April 16th, 2026 | 07:30 CEST

Almonty Industries: Strategic Reassessment Opens Up Further Upside Potential

It is a good thing when a company has what many others want. This is particularly true for Almonty Industries. The US-based company produces the critical raw material tungsten, which is in high demand and irreplaceable across many industries due to its unique properties, such as extreme heat resistance and the ability to withstand enormous pressure. Demand is rising enormously, particularly in the defense industry. Almonty is set to become the largest tungsten producer outside of China in the foreseeable future. Its main production site in Sangdong, South Korea, was designed to generate high margins even in a low-price environment of USD 350 per metric ton unit (MTU). The price currently stands at USD 3,000 per MTU. Analysts are factoring in only a fraction of that. Given the fundamentally changed market conditions, a revaluation of the stock will begin, taking into account the new reality and the company's geopolitical significance.

time to read: 3 minutes

|

Author:

Carsten Mainitz

ISIN:

ALMONTY INDUSTRIES INC. | CA0203987072 | TSX: AII , NASDAQ: ALM , ASX: AII

Table of contents:

Author

Carsten Mainitz

The native Rhineland-Palatinate has been a passionate market participant for more than 25 years. After studying business administration in Mannheim, he worked as a journalist, in equity sales and many years in equity research.

Tag cloud

Shares cloud

Countless Price Drivers

Hardly any other stock has as many potential price drivers as Almonty Industries. The scarcity and rapidly rising demand for tungsten is undeniably playing into the company's hands. USD 3,000 per MTU is a milestone, but not the end of the line. Tungsten is indispensable to the defense industry and plays a critical role in modern industrial applications. China dominates the market with an 80% share. Given the agenda of Western industrialized nations to prioritize non-Chinese deposits and build secure supply chains, Almonty provides the perfect solution that no one can ignore.

But it is not only the defense industry that has an enormous demand for tungsten; the chip industry does as well. Massive supply bottlenecks are looming this year for tungsten hexafluoride, an essential process gas in chip manufacturing. China has also been restricting its exports for some time. The gap between supply and demand continues to widen.

Strategic Leverage: The US

At the beginning of the year, the US government announced the creation of a strategic reserve for rare earths and other critical raw materials to support the national technology industry. This reflects the new reality in the raw materials sector. Governments and states are establishing themselves as a key investor group. They are willing to pay high, strategically motivated prices to ensure supply security.

Against this backdrop, the acquisition of an advanced tungsten project in the US last year was a brilliant move. Production is scheduled to begin in the second half of 2026. In addition, the company's headquarters is currently being relocated from Toronto, Canada, to the US state of Montana. This news has already given the stock a significant boost in recent days.

With planned US production, the company is positioning itself as a preferred supplier to meet the enormous demand from the United States. Notably, the US government has banned the import of critical raw materials from China starting in 2027. As a US-based company, Almonty becomes accessible to a broader pool of institutional investors. In addition, its positioning within the US market could facilitate access to financing and potential government support. With a cash balance of nearly CAD 270 million at the turn of the year, the company is well funded to execute its growth strategy.

Price Targets Should Continue To Rise

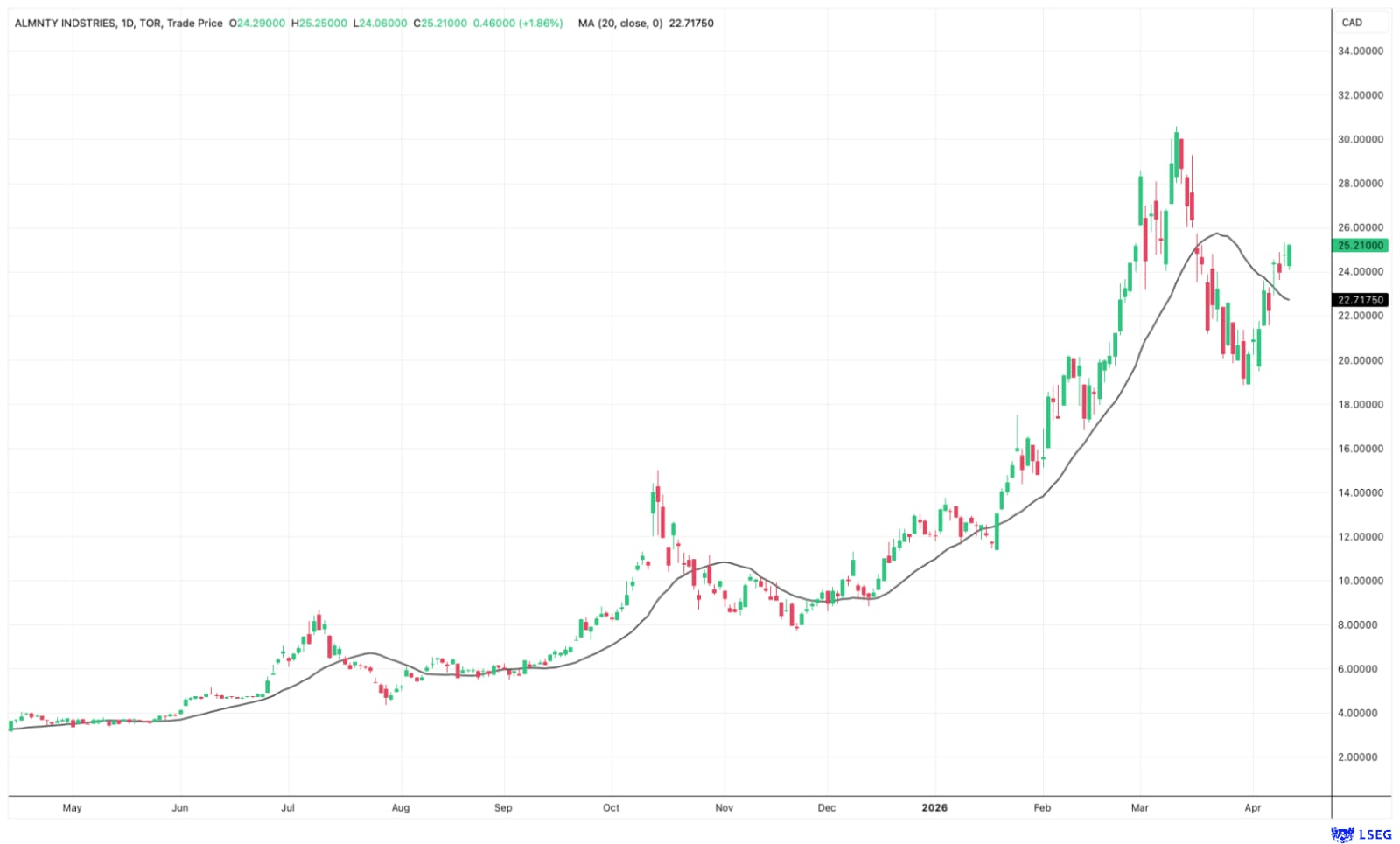

But what does all this say about the stock's valuation? The shares have recently corrected by USD 22 from their all-time highs, but are now already establishing a dynamic upward trend that should lead to new highs, primarily for two reasons. Analysts base their price targets largely on a price level of around USD 1,000 to USD 1,500 per MTU, which is a fraction of the current price.

Even at the assumed lower price, experts believe Almonty will achieve net margins of 60% at full production—a fantastic level. Given the discrepancy between the assumed prices and those actually paid in the market, a gradual increase in price targets and a revaluation of the stock can be expected. Furthermore, a strategic premium, driven by market conditions and geopolitical significance, is barely priced in. That, too, should change soon.

Sangdong as a Beacon

Almonty recently reached full production capacity during Phase 1 of its flagship Sangdong mine in South Korea. This is an important milestone, as 640,000 tons of tungsten ore are now processed here annually, enabling the production of approximately 2,300 tons of tungsten concentrate. With the second expansion phase, expected by the end of 2027, output will increase significantly once again. The goal is to cover 40% of global demand outside of China.

South Korea plays a significant role as a location and platform. The plan is to establish a fully integrated value chain for critical raw materials locally, which would make the Asian country a global hub for the production, refining, and processing of tungsten.

Several factors point to an imminent revaluation of the stock. The persistently high level of tungsten prices and their stability resulting from a supply shortage are the obvious drivers. The pricing in of a strategic premium is currently being completely overlooked. The relocation of the company's headquarters to the US also plays a role here. Investment in the stock, as well as access to loans and subsidies, will be facilitated. Furthermore, with US production set to begin in the second half of the year, the company is positioning itself as the obvious source of supply for the United States. The sheer scale of serving 40% of the world's non-Chinese demand in the future, combined with the strategic importance of this critical raw material, gives the company significant geopolitical weight. All these factors should lead to a revaluation of the stock, which is already moving back toward its previous highs.

Conflict of interest

Pursuant to §85 of the German Securities Trading Act (WpHG), we point out that Apaton Finance GmbH as well as partners, authors or employees of Apaton Finance GmbH (hereinafter referred to as "Relevant Persons") may hold shares or other financial instruments of the aforementioned companies in the future or may bet on rising or falling prices and thus a conflict of interest may arise in the future. The Relevant Persons reserve the right to buy or sell shares or other financial instruments of the Company at any time (hereinafter each a "Transaction"). Transactions may, under certain circumstances, influence the respective price of the shares or other financial instruments of the Company.

In addition, Apaton Finance GmbH is active in the context of the preparation and publication of the reporting in paid contractual relationships.

For this reason, there is a concrete conflict of interest.

The above information on existing conflicts of interest applies to all types and forms of publication used by Apaton Finance GmbH for publications on companies.

Risk notice

Apaton Finance GmbH offers editors, agencies and companies the opportunity to publish commentaries, interviews, summaries, news and the like on news.financial. These contents are exclusively for the information of the readers and do not represent any call to action or recommendations, neither explicitly nor implicitly they are to be understood as an assurance of possible price developments. The contents do not replace individual expert investment advice and do not constitute an offer to sell the discussed share(s) or other financial instruments, nor an invitation to buy or sell such.

The content is expressly not a financial analysis, but a journalistic or advertising text. Readers or users who make investment decisions or carry out transactions on the basis of the information provided here do so entirely at their own risk. No contractual relationship is established between Apaton Finance GmbH and its readers or the users of its offers, as our information only refers to the company and not to the investment decision of the reader or user.

The acquisition of financial instruments involves high risks, which can lead to the total loss of the invested capital. The information published by Apaton Finance GmbH and its authors is based on careful research. Nevertheless, no liability is assumed for financial losses or a content-related guarantee for the topicality, correctness, appropriateness and completeness of the content provided here. Please also note our Terms of use.