April 18th, 2024 | 07:15 CEST

Attention Nvidia! The turnaround check for Nel ASA, Saturn Oil + Gas, Lufthansa and TUI

It looks like a peak is forming in Artificial Intelligence. The most prominent share here is Nvidia. With a spectacular rally, the value has surged by over 100% in just 6 months. However, the share price is now stuttering, and there have been no new highs for days. The charts for TUI and Lufthansa also show an upward reversal. The latest wage negotiations have tightened the cost structure considerably. Also, a significant amount of revenue has been lost due to the numerous strikes. And now the Middle East crisis is flaring up, making the entire region a risk for holidaymakers. However, the rise in oil prices is giving oil companies a new lease of life. Here is a list of interesting investments.

time to read: 4 minutes

|

Author:

André Will-Laudien

ISIN:

NVIDIA CORP. DL-_001 | US67066G1040 , NEL ASA NK-_20 | NO0010081235 , Saturn Oil + Gas Inc. | CA80412L8832 , LUFTHANSA AG VNA O.N. | DE0008232125 , TUI AG NA O.N. | DE000TUAG505

Table of contents:

Author

André Will-Laudien

Born in Munich, he first studied economics and graduated in business administration at the Ludwig-Maximilians-University in 1995. As he was involved with the stock market at a very early stage, he now has more than 30 years of experience in the capital markets.

Tag cloud

Shares cloud

Nel ASA - The planned turnaround is a long time coming

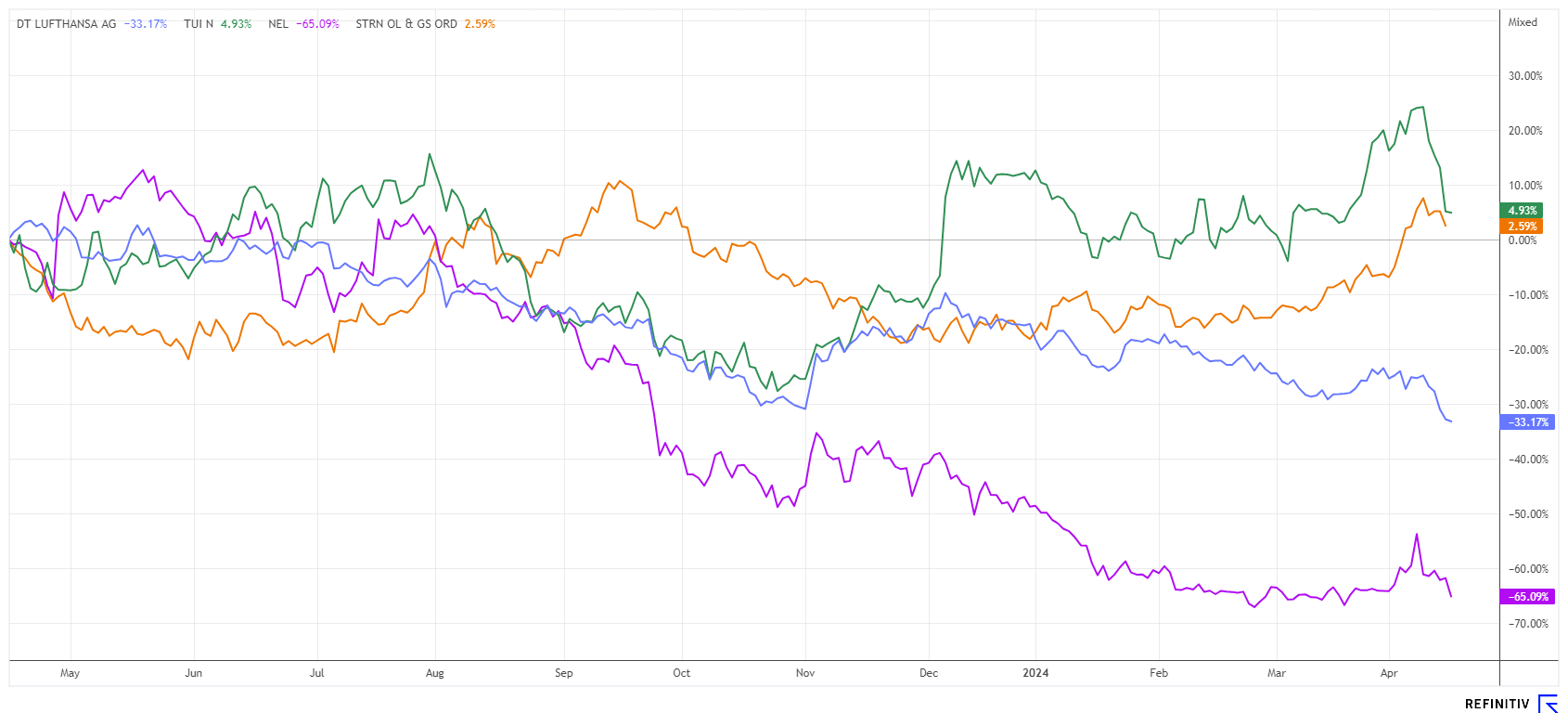

The Norwegian pioneer in electrolysers has shrunk to a market capitalization of EUR 730 million in recent weeks. This puts Nel ASA at a price-to-sales ratio of 4.4 for 2024. After numerous cancellations of major orders, the operating breakeven point is now expected to be reached in 2027. Although revenue for the first quarter of 2024 increased from NOK 409 million to NOK 532 million, a loss of NOK 74 million remained. Management announced that it will continue to invest in expanding organizational and production capacity while working on larger, more complex projects. This strategy, although it could promote growth in the long term, is a burden on the Company's profitability in the short term.

After a share price fall of over 80% in the last 3 years, the chartist can currently recognize some turnaround attempts. From a technical chart perspective, however, the situation now looks much better than at the beginning of the year. Nel ASA has already recovered 10% from its low, but yesterday's loss is again weighing on the picture. Those who buy cautiously now should only do so with a long-term horizon in mind. Over a three-year period, however, triple-digit returns beckon.

Saturn Oil & Gas - Higher oil prices provide cash flow

In addition to the political efforts to shape the energy transition through alternative energies, the undersupply in Germany as an industrial location has shown just how important traditional coal, oil, and gas facilities still are today. Without any need, energy prices in Central Europe have risen dramatically due to the misguided subsidy policy. Unfortunately, the sun does not always shine, and the wind can fail to blow. Regardless of the economic outlook one may project, the long-term geopolitical landscape will likely keep energy prices elevated for a while longer.

Canadian oil producer Saturn Oil & Gas has increased its production capacity in Saskatchewan and Alberta to over 26,500 barrels of oil equivalent by the end of 2023. It expects EBITDA of CAD 355 million over the course of the year at estimated WTI oil prices of USD 80. With over 800 developed drilling locations, the Company is able to generate nearly CAD 100 million in operating earnings (EBITDA) before interest, taxes, depreciation and amortization per quarter. If the expected cash flows are added at a discount rate of 10%, the safest resource indication yields a net cash value of CAD 6.11 per share, and even CAD 14.7 if the estimated reserves are included. It is no wonder that analysts rate the share with average price targets of CAD 5.15 and a "Buy" rating. The aim is to reduce the existing debt of around CAD 413 million by 2026. With spot prices above USD 83 and ongoing geopolitical conflicts, cash flow is likely to be higher than expected. This will generate ongoing surpluses of unimagined proportions and simultaneously release funds that can be used to further develop the properties.

With around 161.5 million shares, the current market capitalization is just under CAD 450 million. Therefore, Saturn Oil is only valued at around 1.5 times free cash flow for 2024. Information on the first quarter of 2024 will be available at the beginning of May. As earnings outside the hedge book will be higher than expected, the share price will likely continue to rise further. It is important to overcome the chart resistance at around CAD 2.85; then, follow-up purchases should follow quickly.

Lufthansa and TUI - Travel is becoming more complicated again

While there was hope for a good tourism year at the beginning of the year, things are turning out differently than expected, with numerous strikes and flight cancellations. With the travel backlog from the Corona years now cleared, TUI and Lufthansa have also been able to repay government aid. However, the average price increase of 40% has, in turn, led consumers to rethink, and today, not all prices quoted are paid so easily. Household budgets are under considerable pressure due to the general increase in the cost of living, especially from government fees and taxes. An improvement in the short term is hardly to be expected with declining economic growth.**

German households are paying several hundred per cent more than the rest of the world in energy prices, which is self-inflicted. Tighter household budgets are having a particularly negative impact on the consumption of luxury goods and are significantly reducing travel budgets. After the disappointing earnings in the first quarter, analysts are now hoping for a recovery by mid-year. On the Refinitiv Eikon platform, only 6 of 22 analysts still recommend the Lufthansa share as a "Buy", but the price expectation is still quite high at EUR 8.65. From a technical perspective, a trend reversal in the share is not expected for the time being. Yesterday's support break at EUR 6.50 is significant and likely to trigger further stop-loss selling. Things look a little better for TUI. The share is currently trading at a 2025 P/E ratio of 5.6, with slight revenue increases of 5% still being consensus. There are also 7 "Buy" recommendations out of 11 estimates with a 12-month price target of EUR 9.90 - a 50% premium to the traded price. Nevertheless, the price should not fall below the support level of EUR 6. The sector is currently only for the most resilient investors.

The energy markets remain tense due to geopolitical uncertainty, as demand for fossil fuels remains high. Hydrogen expert Nel ASA still has a long road to profitability, while Saturn Oil & Gas from Canada can boast a P/E ratio of 1.5 based on 2024 estimates. TUI and Lufthansa should come back into the focus of investors with the summer business, but there is still a risk of price corrections before then.

Conflict of interest

Pursuant to §85 of the German Securities Trading Act (WpHG), we point out that Apaton Finance GmbH as well as partners, authors or employees of Apaton Finance GmbH (hereinafter referred to as "Relevant Persons") currently hold or hold shares or other financial instruments of the aforementioned companies and speculate on their price developments. In this respect, they intend to sell or acquire shares or other financial instruments of the companies (hereinafter each referred to as a "Transaction"). Transactions may thereby influence the respective price of the shares or other financial instruments of the Company.

In this respect, there is a concrete conflict of interest in the reporting on the companies.

In addition, Apaton Finance GmbH is active in the context of the preparation and publication of the reporting in paid contractual relationships.

For this reason, there is also a concrete conflict of interest.

The above information on existing conflicts of interest applies to all types and forms of publication used by Apaton Finance GmbH for publications on companies.

Risk notice

Apaton Finance GmbH offers editors, agencies and companies the opportunity to publish commentaries, interviews, summaries, news and the like on news.financial. These contents are exclusively for the information of the readers and do not represent any call to action or recommendations, neither explicitly nor implicitly they are to be understood as an assurance of possible price developments. The contents do not replace individual expert investment advice and do not constitute an offer to sell the discussed share(s) or other financial instruments, nor an invitation to buy or sell such.

The content is expressly not a financial analysis, but a journalistic or advertising text. Readers or users who make investment decisions or carry out transactions on the basis of the information provided here do so entirely at their own risk. No contractual relationship is established between Apaton Finance GmbH and its readers or the users of its offers, as our information only refers to the company and not to the investment decision of the reader or user.

The acquisition of financial instruments involves high risks, which can lead to the total loss of the invested capital. The information published by Apaton Finance GmbH and its authors is based on careful research. Nevertheless, no liability is assumed for financial losses or a content-related guarantee for the topicality, correctness, appropriateness and completeness of the content provided here. Please also note our Terms of use.