April 8th, 2026 | 08:15 CEST

Rising Rates, ESG & Private Equity: Financing in Extreme Times – Vonovia, RE Royalties, and Mutares

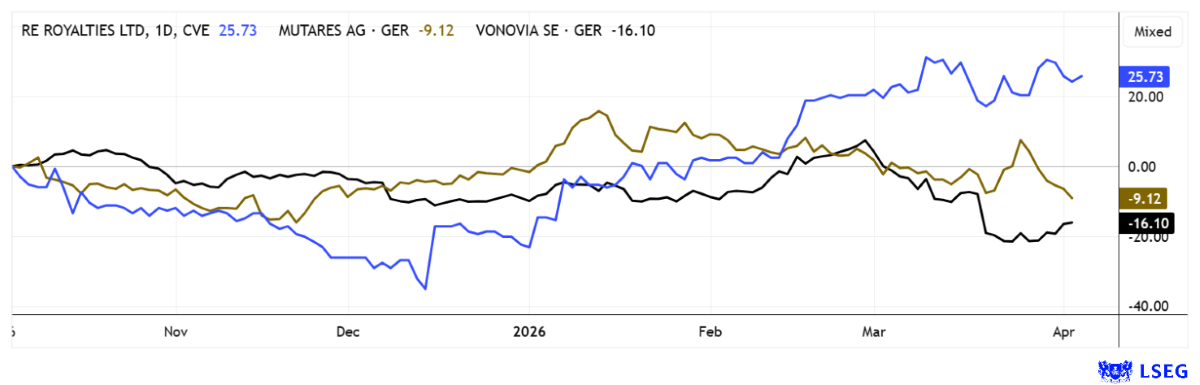

War, destruction, reconstruction. These are all issues closely tied to financing. Clearly, no one is currently thinking about how to rebuild the destroyed buildings, bridges, and power plants in Ukraine, the Gaza Strip, or Iran. First, peace must return before new investments in conflict zones can even be considered. The US likely already has dedicated plans for Ukraine, as well as for the Gaza Strip. For the companies RE Royalties, Vonovia, and Mutares, financing questions arise on a different level. Here, return requirements are linked to each individual investment. Often, however, it is not the interest rate of the financing instrument that matters, but rather the attractiveness of the specific project. This is highly interesting for investors who view a sufficient return as the primary criterion for their investment. The charts of these key players are swinging wildly back and forth, creating opportunities for agile investors!

time to read: 5 minutes

|

Author:

André Will-Laudien

ISIN:

VONOVIA SE NA O.N. | DE000A1ML7J1 , RE ROYALTIES LTD | CA75527Q1081 | TSXV: RE , OTCQX: RROYF , MUTARES KGAA NA O.N. | DE000A2NB650

Table of contents:

Author

André Will-Laudien

Born in Munich, he first studied economics and graduated in business administration at the Ludwig-Maximilians-University in 1995. As he was involved with the stock market at a very early stage, he now has more than 30 years of experience in the capital markets.

Tag cloud

Shares cloud

RE Royalties – Innovative Financing Models Are in Tune with the Times

These days, it takes courage to rethink established practices! The Canadian financier RE Royalties is breaking new ground and relying on an unusual but clever business model. Instead of operating projects itself, the company acquires royalty interests in solar, wind, hydro, and storage projects. This principle, previously more common in the commodities industry, ensures that project developers receive capital without giving up equity, while RE Royalties receives reliable long-term revenue from sales. Since payments are tied to revenue rather than profit, the business model remains stable even as operating costs rise. And the model works!

The project portfolio now comprises over 100 investments in North and South America as well as Asia, making it broadly diversified. The US market is particularly exciting, where rising electricity demand driven by digitalization, electric mobility, and AI data centers is ensuring sustained structural growth. At the same time, RE Royalties has optimized its capital structure, phased out old financing instruments, and thereby created more financial flexibility. With ongoing project plans totaling approximately CAD 20 million and a pipeline of up to CAD 200 million, the company is poised for a significant growth phase.

Management recently announced a strategic review to examine options such as partnerships, new financing avenues, or even a sale, with the aim of specifically increasing the company's value. A closer look reveals that, for investors, the bottom line is an attractive combination of stable cash flow, a high dividend yield of around 10%, and structural tailwinds in the renewable energy market. Active portfolio management, including the expansion of existing royalty components, ensures that the earnings base continues to grow. Should the strategic review result in concrete steps to increase value, the stock could quickly be revalued. Anyone looking for a mix of ESG, security, and returns should jump on this bandwagon!

In an interview with IIF host Lyndsay Malchuk, CEO Bernard Tan describes his medium-term business strategy.

https://www.youtube.com/watch?v=sKWA0kb1A_s

Vonovia – Stable figures meet a nervous interest rate environment

The residential real estate group Vonovia finds itself in rather difficult territory. Although the company recently reported solid figures, the capital market reacted nervously, sending the stock down at times to around EUR 20—a level that many investors associate more with crisis periods like 2023 than with a company reporting rising results again. In fact, adjusted EBITDA recently stood at around EUR 2.8 billion, an increase of about 6%, while the occupancy rate remained very high at just under 98% and rental income also rose by over 4%. For many investors, this discrepancy between stable fundamentals and weak share price performance now feels almost contradictory.

The core of the uncertainty stems from another source: rising financing costs, real-value losses, and limited opportunities to pass on rising facility costs to residents. Analysts also view the portfolio as illiquid, which necessitates both asset sales and debt repayments. Strategically, management is therefore consistently working on the balance sheet and plans to reduce the debt ratio to around 40% by 2028, in part through portfolio sales totaling approximately EUR 5 billion. This may sound unspectacular, but it is crucial for investors because stable finances are a prerequisite for long-term dividends and refinancing.

Analysts on the LSEG Refinitiv platform have a consensus fair value of around EUR 32, signaling upside potential of about 50%. In other words, the market currently has fewer doubts about the company itself than about the external conditions.

Mutares SE – Equity for opportunistic acquisitions and US expansion

The recent capital increase of no less than EUR 105 million brought short sellers into the picture. As a result, the Munich-based investment company's share price fell by nearly 25% last week. The decline bottomed out at temporary lows below EUR 25, and yesterday the share price rebounded to around EUR 28. Mutares is strategizing about the next phase of its expansion in the US and further acquisition opportunities in Europe. For many observers, this shift sends a clear signal: any operationally driven turnaround investor seeking to successfully acquire troubled assets must be able to secure financing quickly. The US markets offer larger companies, more attractive exit opportunities, and broader carve-out pipelines. These are ideal conditions for an agile Mutares, which can only be realized with sufficient equity capital.

Approximately 80% of the proceeds from the capital increase will go toward new acquisitions, with the remainder used to strengthen the balance sheet. This not only finances expansion but also stabilizes the company's own platform, which is important in light of potential covenant breaches starting in 2025. For investors, this means the measure makes economic sense, it creates room for maneuver, and it protects against unexpected risks in the acquisition process. Mutares generates its revenue primarily from consulting services, management fees, dividends, and exit proceeds. More portfolio and add-on investments expand this base, while divestitures temporarily impact the holding company's net income. The capital increase is therefore not just a financing instrument but a direct input for the future business model. The current transaction pipeline in the US includes attractive acquisition opportunities with a total revenue volume of approximately EUR 4.8 billion. CIO Johannes Laumann explains: "An exceptionally attractive setup currently exists in the US!"

With a slightly negative overall bias, analysts view the financing measures as necessary to secure the US focus and growth opportunities. The fact that existing shareholders are largely waiving their subscription rights is already a well-known procedure. The volatile sideways trend of the stock between EUR 25 and 45 is likely to continue in the medium term. Investors who take this range into account have also been able to collect a dividend of over 8%, which remains attractive in the current environment.

In today's financial sector, resilient structures and robust business models matter more than ever. Return potential and risk management must be in balance. The recent challenges at Vonovia demonstrate that this balance is not achievable in every market environment. RE Royalties, on the other hand, represents a model that combines structured royalty financing in the renewable energy sector with predictable cash flows and a clear focus on sustainability. As an investment company, Mutares pursues a hybrid revenue approach that is now set to be scaled up further in the US. Why not also tap into transatlantic opportunities?

Conflict of interest

Pursuant to §85 of the German Securities Trading Act (WpHG), we point out that Apaton Finance GmbH as well as partners, authors or employees of Apaton Finance GmbH (hereinafter referred to as "Relevant Persons") currently hold or hold shares or other financial instruments of the aforementioned companies and speculate on their price developments. In this respect, they intend to sell or acquire shares or other financial instruments of the companies (hereinafter each referred to as a "Transaction"). Transactions may thereby influence the respective price of the shares or other financial instruments of the Company.

In this respect, there is a concrete conflict of interest in the reporting on the companies.

In addition, Apaton Finance GmbH is active in the context of the preparation and publication of the reporting in paid contractual relationships.

For this reason, there is also a concrete conflict of interest.

The above information on existing conflicts of interest applies to all types and forms of publication used by Apaton Finance GmbH for publications on companies.

Risk notice

Apaton Finance GmbH offers editors, agencies and companies the opportunity to publish commentaries, interviews, summaries, news and the like on news.financial. These contents are exclusively for the information of the readers and do not represent any call to action or recommendations, neither explicitly nor implicitly they are to be understood as an assurance of possible price developments. The contents do not replace individual expert investment advice and do not constitute an offer to sell the discussed share(s) or other financial instruments, nor an invitation to buy or sell such.

The content is expressly not a financial analysis, but a journalistic or advertising text. Readers or users who make investment decisions or carry out transactions on the basis of the information provided here do so entirely at their own risk. No contractual relationship is established between Apaton Finance GmbH and its readers or the users of its offers, as our information only refers to the company and not to the investment decision of the reader or user.

The acquisition of financial instruments involves high risks, which can lead to the total loss of the invested capital. The information published by Apaton Finance GmbH and its authors is based on careful research. Nevertheless, no liability is assumed for financial losses or a content-related guarantee for the topicality, correctness, appropriateness and completeness of the content provided here. Please also note our Terms of use.