March 25th, 2026 | 07:15 CET

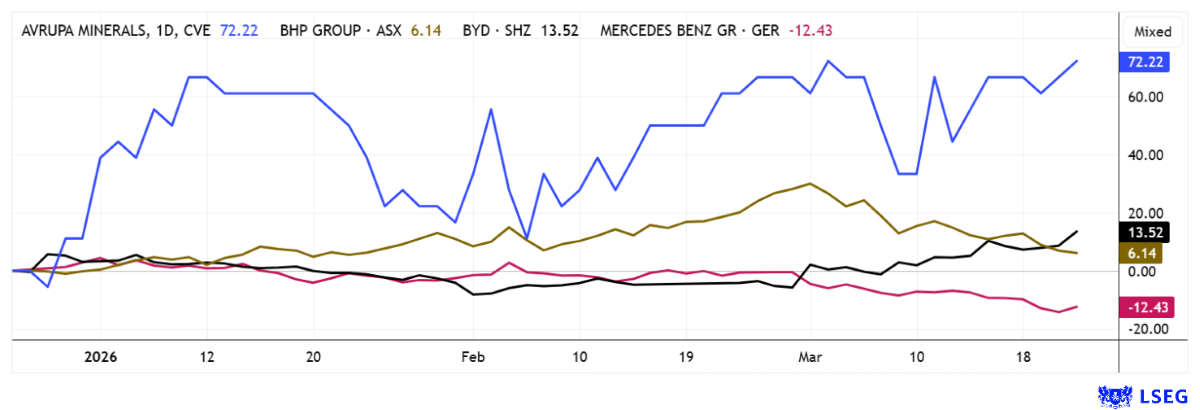

Trump and the EU Need Critical Metals and Oil Alternatives! BHP, Avrupa Minerals, Mercedes, and BYD

As oil prices surge to new levels above USD 100, investors are facing heightened supply chain concerns. Just as during the COVID-19 pandemic, global trade relations in the commodities sector are at risk of grinding to a halt due to the closure of the Strait of Hormuz. Following significant price declines across all industrial sectors, it is essential to identify potential winners. The commodities giant BHP can look forward to rising revenues and cash flows, while a new surge in e-mobility is expected in the alternative energy sector. Avrupa Minerals is searching for critical materials in Finland and Portugal and has already made discoveries. An exciting investment opportunity is currently emerging.

time to read: 5 minutes

|

Author:

André Will-Laudien

ISIN:

BHP GROUP LTD. DL -_50 | AU000000BHP4 , AVRUPA MINERALS LTD | CA05453A2074 | TSXV: AVU , MERCEDES-BENZ GROUP AG | DE0007100000 , BYD CO. LTD H YC 1 | CNE100000296

Table of contents:

Author

André Will-Laudien

Born in Munich, he first studied economics and graduated in business administration at the Ludwig-Maximilians-University in 1995. As he was involved with the stock market at a very early stage, he now has more than 30 years of experience in the capital markets.

Tag cloud

Shares cloud

BHP Ltd. – The Commodity Giant with Billions in Cash Flow

At the center of the commodities storm is currently the mining giant BHP. The Australian group is currently benefiting greatly from the structural shortage of critical metals, particularly copper, whose prices have risen by about 32% compared to the previous year, thereby significantly increasing producers' margins. Due to demand from increasing electrification, the expansion of data centers, and progress in the energy transition, supply currently cannot keep up. New mines take about 10 years before the first concentrate is delivered, making this a home run for large, established producers. For BHP, copper now accounts for 51% of consolidated EBITDA; in the latest figures for the half-year ending December 2025, adjusted EBITDA rose by 25% to USD 15.5 billion, while the EBITDA margin reached a very high 58%. Operating cash flow also remained strong at approximately USD 9.4 billion, enabling continued high levels of investment as well as a dividend of USD 0.73 per share, an increase of about 46% compared to 2024.

At the same time, the company has raised its copper production forecast for fiscal year 2026 to approximately 1.9 to 2.0 million tons to meet expected demand. Strategically, the group is currently investing billions in new projects and is deliberately positioning itself as a long-term beneficiary of a potential global supply shortage of critical metals. Now begins a phase of stable, annual profit growth for BHP and its shareholders. With a 4.5% dividend yield and a 2026 P/E ratio of 13.4, the stock is historically undervalued despite a 50% increase since 2025. Snap it up!

Avrupa Minerals – On Track with Europe's Raw Materials Strategy

The situation in Europe is a major cause for concern! This is because the region has few developed raw material deposits and is therefore ill-prepared for current international disruptions. Europe, and the EU in particular, could one day even be completely cut off from supplies. As part of Europe's efforts to achieve greater resource sovereignty, the exploration company Avrupa Minerals Ltd. is coming into sharper focus, as it specifically develops projects in politically stable regions.

The company uses a project generator model, in which deposits are identified early on and then further developed with partners, thereby limiting capital requirements and dilution for shareholders. With a market capitalization of approximately CAD 5 million, Avrupa ranks among the smaller explorers but possesses significant operational leverage from exploration successes. The focus is on strategically important metals such as copper and zinc, which are experiencing structurally rising demand as part of the energy transition. In 2025, the company significantly expanded its presence in Finland's Pyhäsalmi district and secured new exploration areas. Of particular importance was the acquisition of the Lippikylä permit, which is located less than 2 km from the former Pyhäsalmi mine and is considered a potential extension of the known ore system.

Together with the Lehto area, at least 5 drill-ready targets have been identified that can be incorporated into new programs in the near term. In addition, the KKS area was acquired, featuring three additional VMS targets where previous drilling has already identified sulfide lenses at depths of approximately 100 to 150 m. In total, the Finnish partnership now controls 8 permits with 7 copper-zinc targets within a radius of approximately 40 km of an existing processing plant, which creates infrastructure advantages. In parallel, the company is advancing the Alvalade project in Portugal, for which a mining license has already been applied for the Sesmarias deposit. Management has also acquired a 49% stake in the Slivova Gold project in Kosovo, whose development is set to resume following an expected re-licensing. For 2026, management plans new exploration programs in Finland as soon as a financing partner is found. An extremely exciting, EU-focused story! Enter in stages given the current market environment!

CEO Paul Kuhn describes current project highlights and his plans for 2026 in a recent interview with Stockhouse.

BYD versus Mercedes – Mobility from Two Perspectives

Success in e-mobility is directly linked to the availability of critical metals, as a total of 22 critical metals are used in the latest-generation batteries and electric drives. In the European e-mobility market, BYD and Mercedes-Benz have so far demonstrated distinctly different success strategies, reflecting differences in production capacity, price positioning, and technology deployment. BYD delivered approximately 75,000 vehicles in Europe in 2025, representing growth of nearly 120% compared to 2024. Mercedes delivered about 50,000 electric vehicles during the same period, which is still an increase of approximately 35% over the previous year, but lags behind BYD.

Analysts highlight that BYD stands out particularly due to its vertically integrated battery cell production and low manufacturing costs. This has enabled the company to achieve an average unit price of EUR 28,500 in the lower and mid-range segments, while Mercedes, with its premium approach, is positioned in the market at an average price of EUR 67,000. Typically, these buyer groups do not compete with one another; nevertheless, BYD benefits from a rapidly scalable pricing strategy that primarily targets fleet customers and urban logistics companies. Mercedes, on the other hand, excels in margins: The EBIT margin of the electric vehicle division stood at around 15% in 2025, while BYD, despite strong sales volume, only reached around 8%.

In their market forecast for 2026, analysts expect BYD to double its European deliveries to 150,000 vehicles, supported by partnerships in Germany, France, and the Netherlands. Mercedes is projected to deliver 65,000 to 70,000 vehicles, albeit with stable profitability. Most recently, Mercedes was weighed down by weak business in Asia, but this is now expected to be offset by a new EU strategy. From an analytical perspective, BYD and Mercedes offer 2026 P/E ratios of 14.4 and 8.9. Mercedes-Benz holds its annual general meeting on April 16, at which time a dividend of EUR 3.26 will be paid, representing an excellent yield of 6% at current prices. Both stocks appeal for their solidity and robust financials. Current entry prices are EUR 11.65 and EUR 51.50, respectively—making them highly attractive for the long term.

The shortage of critical metals is weighing on many industries and could become a major obstacle in a worst-case scenario. Companies like BYD and Mercedes-Benz are under intense scrutiny in this regard. On the supply side, Avrupa Minerals' properties could well attract the attention of a major player like BHP. A well-diversified portfolio protects against major fluctuations!

Conflict of interest

Pursuant to §85 of the German Securities Trading Act (WpHG), we point out that Apaton Finance GmbH as well as partners, authors or employees of Apaton Finance GmbH (hereinafter referred to as "Relevant Persons") currently hold or hold shares or other financial instruments of the aforementioned companies and speculate on their price developments. In this respect, they intend to sell or acquire shares or other financial instruments of the companies (hereinafter each referred to as a "Transaction"). Transactions may thereby influence the respective price of the shares or other financial instruments of the Company.

In this respect, there is a concrete conflict of interest in the reporting on the companies.

In addition, Apaton Finance GmbH is active in the context of the preparation and publication of the reporting in paid contractual relationships.

For this reason, there is also a concrete conflict of interest.

The above information on existing conflicts of interest applies to all types and forms of publication used by Apaton Finance GmbH for publications on companies.

Risk notice

Apaton Finance GmbH offers editors, agencies and companies the opportunity to publish commentaries, interviews, summaries, news and the like on news.financial. These contents are exclusively for the information of the readers and do not represent any call to action or recommendations, neither explicitly nor implicitly they are to be understood as an assurance of possible price developments. The contents do not replace individual expert investment advice and do not constitute an offer to sell the discussed share(s) or other financial instruments, nor an invitation to buy or sell such.

The content is expressly not a financial analysis, but a journalistic or advertising text. Readers or users who make investment decisions or carry out transactions on the basis of the information provided here do so entirely at their own risk. No contractual relationship is established between Apaton Finance GmbH and its readers or the users of its offers, as our information only refers to the company and not to the investment decision of the reader or user.

The acquisition of financial instruments involves high risks, which can lead to the total loss of the invested capital. The information published by Apaton Finance GmbH and its authors is based on careful research. Nevertheless, no liability is assumed for financial losses or a content-related guarantee for the topicality, correctness, appropriateness and completeness of the content provided here. Please also note our Terms of use.