May 1st, 2026 | 07:25 CEST

Is a Western Tungsten Ecosystem Emerging? Almonty Industries vs China Tungsten – Does Rheinmetall Stand to Gain?

The supply of tungsten has become one of the most critical bottlenecks for Western security and high technology. The metal, which has the highest melting point of any element at 3,422°C, is simply irreplaceable in modern weapon systems, semiconductors, and technologies ranging from the energy transition to fusion energy. While the Chinese market leader, China Tungsten and Hightech Materials, continues to post impressive record figures, a turning point is unfolding behind the scenes: China is transforming from a dominant exporter to a strategic importer of tungsten concentrates. This development is forcing Western consumers like Rheinmetall to radically reevaluate their supply chains to avoid dependence on Beijing's export decisions. Almonty is stepping into this strategic vacuum; with the commissioning of the Sangdong mine in South Korea, it is becoming the new linchpin of a Western-oriented raw materials alliance. The current market situation makes it clear that the era of cheap and always-available tungsten from the Far East is over. This makes establishing self-sufficient supply chains in secure jurisdictions a top priority for Western governments. Almonty is likely to benefit. We compare this ambitious tungsten player with the Chinese market leader.

time to read: 4 minutes

|

Author:

Nico Popp

ISIN:

ALMONTY INDUSTRIES INC. | CA0203987072 | TSX: AII , NASDAQ: ALM , ASX: AII , RHEINMETALL AG | DE0007030009

Table of contents:

Author

Nico Popp

At home in Southern Germany, the passionate stock exchange expert has been accompanying the capital markets for about twenty years. With a soft spot for smaller companies, he is constantly on the lookout for exciting investment stories.

Tag cloud

Shares cloud

China Tungsten: A Giant at the Zenith of Its Power

China Tungsten and Hightech Materials embodies the ideal image of a vertically integrated commodities group. The company covers the entire value chain—from mining in large-scale deposits to the production of high-precision cutting tools and micro-drills for the AI circuit board industry. The group's latest financial data attests to this dominance. In the first quarter of 2026, net profit surged by 264.4% to RMB 921 million. Despite this impressive performance, China Tungsten's data also highlights the limitations of the Chinese model, as declining ore grades in domestic mines are increasingly forcing the group to source raw materials globally. In January and February, China recorded a significant net import of tungsten metal for the first time, while exports of key precursors such as ammonium paratungstate (APT) effectively fell to zero. For Western buyers, this is a clear signal: Chinese resources are primarily reserved for its own high-tech industry.

Rheinmetall and the Defence of Supply Chains in Times of Rearmament

For the Düsseldorf-based defense group Rheinmetall, this development has existential implications. At a time when Europe is rearming on a massive scale, tungsten is the indispensable "enabler" for nearly all modern weapon systems, particularly for kinetic energy munitions. Rheinmetall increased its revenue by 29% to EUR 9.9 billion in fiscal year 2025, while its order backlog climbed to a record EUR 63.8 billion.

To realize this enormous growth potential, Rheinmetall must reassess its raw material risks and is dependent on new, politically stable sources. The strategic importance of tungsten is also evident in the aviation, energy production, and high-tech industries of the United States. For many world-class companies, the emergence of a high-performing Western producer is therefore not a luxury but a hard operational necessity. Rheinmetall is just one of many companies that need tungsten for growth. Other examples include Boeing, SpaceX, and chip giants like Intel.

Almonty Industries: A New Champion Emerges

This is why Almonty Industries' time has come. With the official commissioning of the Sangdong mine in South Korea in March, the company, which has been mining tungsten in Portugal for years and is regarded as a master of efficiency in the extraction and processing of this critical metal, has entered a new phase. Sangdong is considered one of the world's largest and highest-grade tungsten deposits and is estimated to supply 40% of global supply outside China's sphere of influence. Almonty is pursuing an integrated approach known as the "Korean Trinity." In addition to concentrate production, the company is establishing its own oxide plant to directly produce ammonium paratungstate (APT) and oxides for the semiconductor and battery industries.

A decisive strategic move was the recent relocation of the company's headquarters to the US, accompanied by the US Congress's official recognition of Almonty as "strategic infrastructure." This positions Almonty as the partner of choice for the Pentagon and Western governments to end strategic dependence on China for tungsten. Financial support from Germany's Kreditanstalt für Wiederaufbau (KfW), which has already provided over USD 90 million for Sangdong, underscores the strong government backing for the company. Almonty also plans to become the sole integrated US producer by 2026 through the commissioning of the Montana project acquired last fall. This, too, could elevate the company's valuation to a new level.

Conclusion: Enormous Potential for Almonty Shareholders

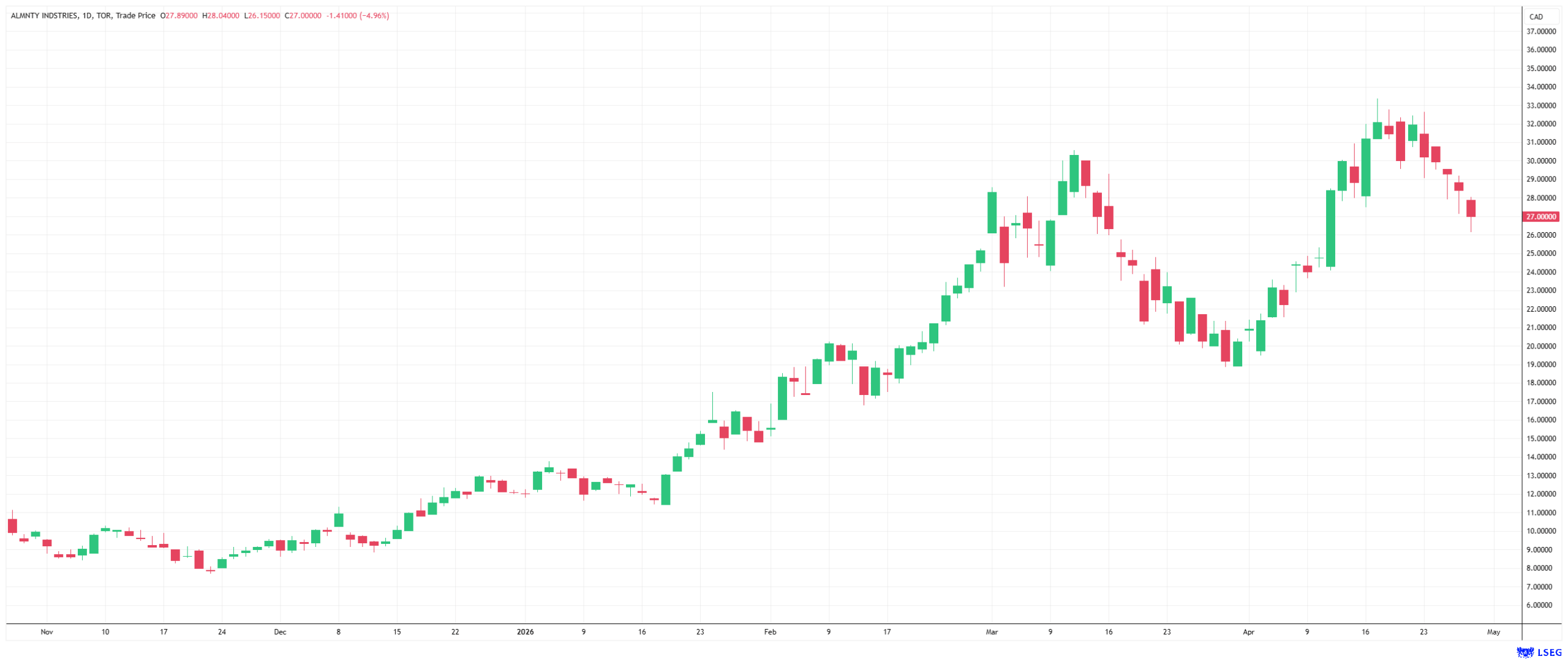

A cross-comparison highlights the potential: While China Tungsten is valued at around USD 18 billion on the stock market, Almonty's market capitalization, despite the enormous price gains of the past twelve months, remains around USD 5.9 billion, a fraction of that. The only things currently missing for Almonty to catch up with the Chinese giant are full operational scaling and the completion of the oxide plant. Once this vertical integration is in place, Almonty is likely to be valued not merely as a mining stock but as a specialized materials company. Analysts at Cantor Fitzgerald and Texas Capital emphasize that Almonty is well on its way to becoming the world's most profitable tungsten producer. While China Tungsten is valued at a forward P/E ratio of around 23, earnings estimates for Almonty for 2027 imply a P/E ratio of just 10.

For investors, the government-backed expansion of the Sangdong mine and the expansion into the US offer a rare opportunity to gain early exposure to a new Western commodities champion whose products are systemically important to customers such as Rheinmetall and many other companies worldwide. This unique risk-reward ratio is supported by surging tungsten prices, which stood at around USD 340 in early 2025 and have since surpassed USD 3,000. No alternative tungsten projects in the West, aside from the aforementioned Almonty mines, are expected to enter production in the foreseeable future.

Conflict of interest

Pursuant to §85 of the German Securities Trading Act (WpHG), we point out that Apaton Finance GmbH as well as partners, authors or employees of Apaton Finance GmbH (hereinafter referred to as "Relevant Persons") currently hold or hold shares or other financial instruments of the aforementioned companies and speculate on their price developments. In this respect, they intend to sell or acquire shares or other financial instruments of the companies (hereinafter each referred to as a "Transaction"). Transactions may thereby influence the respective price of the shares or other financial instruments of the Company.

In this respect, there is a concrete conflict of interest in the reporting on the companies.

In addition, Apaton Finance GmbH is active in the context of the preparation and publication of the reporting in paid contractual relationships.

For this reason, there is also a concrete conflict of interest.

The above information on existing conflicts of interest applies to all types and forms of publication used by Apaton Finance GmbH for publications on companies.

Risk notice

Apaton Finance GmbH offers editors, agencies and companies the opportunity to publish commentaries, interviews, summaries, news and the like on news.financial. These contents are exclusively for the information of the readers and do not represent any call to action or recommendations, neither explicitly nor implicitly they are to be understood as an assurance of possible price developments. The contents do not replace individual expert investment advice and do not constitute an offer to sell the discussed share(s) or other financial instruments, nor an invitation to buy or sell such.

The content is expressly not a financial analysis, but a journalistic or advertising text. Readers or users who make investment decisions or carry out transactions on the basis of the information provided here do so entirely at their own risk. No contractual relationship is established between Apaton Finance GmbH and its readers or the users of its offers, as our information only refers to the company and not to the investment decision of the reader or user.

The acquisition of financial instruments involves high risks, which can lead to the total loss of the invested capital. The information published by Apaton Finance GmbH and its authors is based on careful research. Nevertheless, no liability is assumed for financial losses or a content-related guarantee for the topicality, correctness, appropriateness and completeness of the content provided here. Please also note our Terms of use.