April 29th, 2026 | 07:30 CEST

Gold Production Starting Soon, PEA Covers Only 10% of the Resource—the Rest Is Currently a Free Bonus at Desert Gold Ventures

Mali provides the cash flow, Côte d'Ivoire the potential—that is the simple equation at Desert Gold. While most junior miners are still struggling to secure their next round of financing, the Canadians are already constructing a gravity plant. Permits are in place, funding has been secured, and construction is underway. Those who wait may end up paying more later. Once the first ounce of gold is produced, the valuation logic typically changes fundamentally. This article explains why the pre-production phase could represent the more attractive entry point.

time to read: 4 minutes

|

Author:

Armin Schulz

ISIN:

DESERT GOLD VENTURES | CA25039N4084 | TSXV: DAU , OTCQB: DAUGF

Table of contents:

Author

Armin Schulz

Born in Mönchengladbach, he studied business administration in the Netherlands. In the course of his studies he came into contact with the stock exchange for the first time. He has more than 25 years of experience in stock market business.

Tag cloud

Shares cloud

Mali: From Drilling to Profit

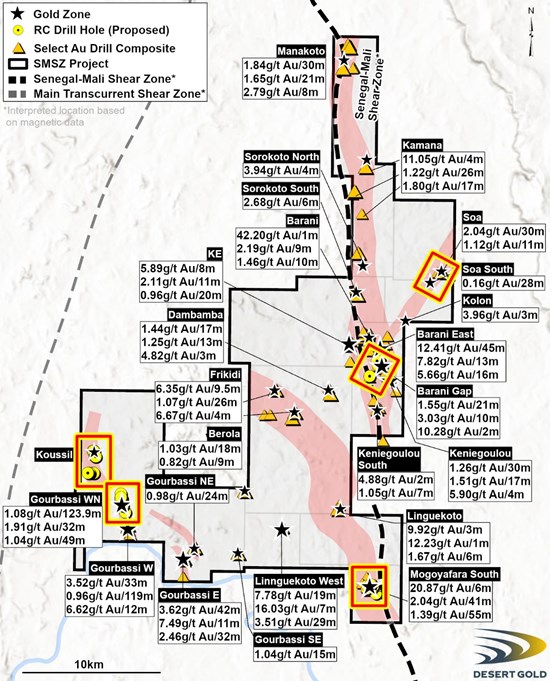

The focus is on the Senegal-Mali Shear Zone (SMSZ) project, a 440 km² area in one of West Africa's most productive gold regions. The neighborhood reads like a directory of gold producers, featuring Barrick, B2Gold, and Allied Gold. Desert Gold has reported a resource of approximately 1.22 million ounces there. But that alone would not be remarkable. What matters is the upcoming gold production.

The company has already begun construction work on the Barani-East oxide gold mine. A modular gravity processing plant has been ordered. The delivery date is early May. The manufacturer will remain on-site for several months to provide training. The approach is deliberately phased. First comes site preparation, then delivery and installation, in order to minimize execution risks.

Financing is secured. In February, Desert Gold completed an oversubscribed LIFE placement of approximately CAD 7.2 million, plus a follow-on subscription. The funds will go toward the first phase of the gravity plant, drilling in Côte d'Ivoire, and resource expansion and exploration drilling at the SMSZ project in Mali. Production at Barani East is targeted to begin in the first half of 2026.

The Barani East Strategy: Start Small, Then Scale Up

The key is phased development. Instead of immediately building an expensive CIL plant, Desert Gold is starting with a gravity stage that achieves a gold recovery rate of about 68%. The processed ore is temporarily stored and can be processed again later via a CIL retrofit, thereby increasing the recovery rate to up to 92%. The Preliminary Economic Assessment (PEA) from November 2025 shows that the model is viable. At a gold price of USD 2,850, the after-tax net present value is USD 61 million, with an internal rate of return of 57%. The payback period is 2.5 years.

And this is calculated using only a fraction of the resource, thereby leaving significant opportunities to improve the project's economics and substantially expand operations over time.

Ongoing drilling supports this outlook. In April 2026, a 4,250-meter RC drill program commenced at 5 priority targets, including Koussili, Gourbassi West North, and the promising Kolon-Soa, an 8 km-long gold-in-soil anomaly featuring artisanal mining and rock samples of up to 77 g/t gold.

What the PEA Does Not Show

The Preliminary Economic Assessment (PEA) considered only the near-surface oxide mineralization, which accounts for about 10% of the total resource. The deeper portion in the fresh rock was completely left out. This is not a shortcoming, but a deliberate decision. First come the quick returns, then the expansion.

The work an explorer has to do is always the same: expand the resource base and build scale in terms of volume and tonnage. That is exactly what is happening right now. Anyone familiar with the major players in West Africa knows that packages like this tend to attract strong interest. Over the past decade and a half, the industry has seen multiple multi-billion-dollar transactions in this belt.

The Second Pillar: Tiegba in Côte d'Ivoire

While Mali is set to become the operational workhorse, Tiegba could deliver the surprise. The 297 km² project is located in Côte d'Ivoire, along the Tehini shear zone, in the same district as Bonikro and Agbaou, where Allied Gold (soon to be part of Zijin) is producing. What makes it special is a 4.5 km-long and 2 km-wide gold anomaly in the ground that Newcrest discovered years ago but never drilled.

The team was on-site, assessed the situation firsthand, and is convinced that the anomaly is present. An aeromagnetic drone survey is planned, followed by aircore drilling across the anomaly. Notably, around 85% of the license area remains completely unexplored. This is classic option value; the project is not currently reflected in the share price, yet it carries the potential to materially increase overall valuation. Should a new discovery in the range of 0.5–1.0 million ounces be made in this belt, it would likely attract significant attention and cause a stir - particularly given the need for replenishment at the more mature mines in the vicinity.

Why the Timing Is Attractive Now

The market capitalization currently stands at around CAD 35 million, with approximately 360 million shares outstanding and a well-funded cash position. A significant portion of this valuation is already covered by the PEA valuation of the Barani East project. This implies that Tiegba, the remaining resources in Mali, and the broader exploration upside are, at present, almost being valued as a free option.

The company has notable shareholders, including Merk Investments and Pan-American Silver Chairman Ross Beaty. Management and the board hold significant stakes, which aligns their interests.

The political situation in Mali has eased, yet the markets are already pricing in the risk generously, according to management's assessment. Many other companies with inferior assets have seen significant valuation jumps. Mali is on a better path today than it was a year ago.

The company is drilling its most promising targets, and the financing for this is already secured. Every hit increases the upside potential. Analysts at GBC share this view, having set a price target of CAD 0.93. The reason for this is the imminent start of production, which is expected to significantly increase the company's valuation.

The stock is currently trading at CAD 0.13.

Desert Gold offers a rare combination of secured financing, ongoing mine construction, and a defined production outlook for 2026, alongside a largely untested option in Côte d'Ivoire. Those who wait until first production often encounter a repriced asset base. The coming months could therefore bring incremental positive catalysts as milestones are reached. The risk-reward profile has now clearly turned positive. That is precisely why it is worth taking an early look before production begins.

Conflict of interest

Pursuant to §85 of the German Securities Trading Act (WpHG), we point out that Apaton Finance GmbH as well as partners, authors or employees of Apaton Finance GmbH (hereinafter referred to as "Relevant Persons") currently hold or hold shares or other financial instruments of the aforementioned companies and speculate on their price developments. In this respect, they intend to sell or acquire shares or other financial instruments of the companies (hereinafter each referred to as a "Transaction"). Transactions may thereby influence the respective price of the shares or other financial instruments of the Company.

In this respect, there is a concrete conflict of interest in the reporting on the companies.

In addition, Apaton Finance GmbH is active in the context of the preparation and publication of the reporting in paid contractual relationships.

For this reason, there is also a concrete conflict of interest.

The above information on existing conflicts of interest applies to all types and forms of publication used by Apaton Finance GmbH for publications on companies.

Risk notice

Apaton Finance GmbH offers editors, agencies and companies the opportunity to publish commentaries, interviews, summaries, news and the like on news.financial. These contents are exclusively for the information of the readers and do not represent any call to action or recommendations, neither explicitly nor implicitly they are to be understood as an assurance of possible price developments. The contents do not replace individual expert investment advice and do not constitute an offer to sell the discussed share(s) or other financial instruments, nor an invitation to buy or sell such.

The content is expressly not a financial analysis, but a journalistic or advertising text. Readers or users who make investment decisions or carry out transactions on the basis of the information provided here do so entirely at their own risk. No contractual relationship is established between Apaton Finance GmbH and its readers or the users of its offers, as our information only refers to the company and not to the investment decision of the reader or user.

The acquisition of financial instruments involves high risks, which can lead to the total loss of the invested capital. The information published by Apaton Finance GmbH and its authors is based on careful research. Nevertheless, no liability is assumed for financial losses or a content-related guarantee for the topicality, correctness, appropriateness and completeness of the content provided here. Please also note our Terms of use.