April 13th, 2026 | 09:30 CEST

Double The Gains: 100% Rebound in Defense Stocks and Critical Metals – Rheinmetall, Antimony Resources, CSG, and Mutares in focus

Created and published on behalf of Antimony Resources Corp.

The stock market gives and takes. While investors were able to celebrate a massive 5% gain last week, the tide has already turned in the opposite direction this week. The reason: The hoped-for peace talks in Pakistan between the US, Israel, and Iran have failed. Since this provides no positive momentum for the economy or the already strained energy and metals markets, volatility is likely to return in some sectors. We are looking at opportunities in the critical metals sector and highlighting some stocks that are showing attractive metrics again following recent corrections.

time to read: 5 minutes

|

Author:

André Will-Laudien

ISIN:

ANTIMONY RESOURCES CORP | CA0369271014 | CSE: ATMY , OTCQB: ATMYF , RHEINMETALL AG | DE0007030009 , CSG NV | NL0015073TS8 , MUTARES KGAA NA O.N. | DE000A2NB650

Table of contents:

Author

André Will-Laudien

Born in Munich, he first studied economics and graduated in business administration at the Ludwig-Maximilians-University in 1995. As he was involved with the stock market at a very early stage, he now has more than 30 years of experience in the capital markets.

Tag cloud

Shares cloud

Antimony Resources for Western Supply Security – Billions in Potential in the Ground

The Iran conflict highlights just how vulnerable Western industry is today. Without energy resources and critical metals, nothing works. The global antimony market offers a prime example. It is currently experiencing a structural supply shortage, as China controls around 70% of global production and thus exerts significant influence over prices and availability. In recent years, this market concentration has led to an extraordinary price rally, with spot market prices quadrupling from around USD 15,000 per ton to over USD 60,000 at times. At the same time, industrial demand is growing rapidly, particularly driven by military applications, flame-retardant systems, data center infrastructure, and new battery and solar technologies. Government initiatives to build strategic raw material reserves further reinforce this trend and create a structural demand buffer for the coming years.

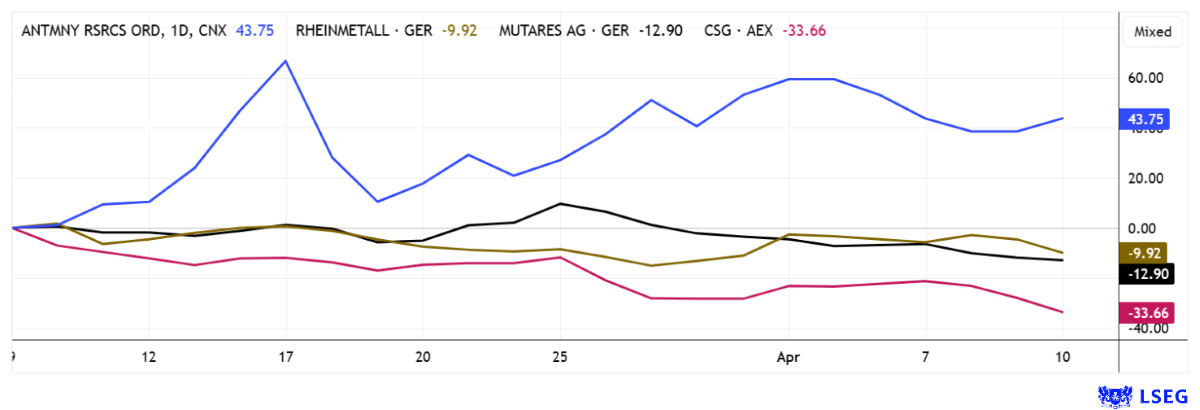

The capital markets are reacting sensitively to this scarcity, as impressively demonstrated by the share price performance of Antimony Resources, whose stock rose from EUR 0.33 to around EUR 1.65 within just five months, recording an increase in value of approximately 500%. Such movements reflect a revaluation of strategic metals in an environment of growing geopolitical tensions, where antimony has become indispensable for both modern defense systems and digital infrastructure. Against this backdrop, the Bald Hill project in New Brunswick is gaining strategic importance, as it is considered one of the largest known antimony deposits in North America and has an exploration target of approximately 2.7 million tons of ore with average grades between 3% and 4%. At an average grade of 3.5%, this results in a potential metal inventory of approximately 94,500 tons of antimony, which, at an assumed price of USD 35,000 per ton, corresponds to a theoretical gross metal value of about USD 3.3 billion.

Drilling programs have confirmed a mineralized structure extending over more than 700 m in length and to a depth of at least 350 m, with individual sections exhibiting peak grades exceeding 30%, signaling the potential for high-margin production zones. Operationally, the project is in the critical phase between exploration and development, with the company proactively mitigating regulatory risks by initiating technical and environmental studies early in the permitting process. A clearly defined permitting roadmap, close coordination with authorities, and the early engagement of local stakeholders enhance planning certainty and are considered key value drivers in the commodities industry. In parallel, the company is working on its first formal NI 43-101 resource estimate, which typically represents one of the most significant valuation jumps in the life cycle of an exploration project.

CEO James R. Atkinson outlines key aspects of his strategy in an interview with IIF host Lyndsay Malchuk.

With a market capitalization in the range of approximately CAD 140 million, the company should seek out the current environment for new capital raising, as there remains a significant valuation discount compared to the potential metal value in the ground. Antimony Resources' stock offers investors above-average strategic and economic leverage. Research firm GBC recently determined a fair value of CAD 3.00 per share, so the rally should continue rapidly following the release of the first resource estimate.

Rheinmetall – Is it Already 2029?

The defense sector is one of the largest consumers of critical metals. In recent years, Rheinmetall has evolved from a traditional automotive supplier into one of Europe's leading defense conglomerates and continues to benefit from high demand for ammunition, vehicles, and air defense systems. The figures for 2025 impressively document this rise. Revenue in 2025 rose by 29% to EUR 9.9 billion, while operating profit climbed to EUR 1.84 billion and the operating margin reached 18.5%. At the same time, the group increased its order backlog by 36%. For 2026, management forecasts revenue growth of 40 to 45% to EUR 14.0 to 14.5 billion and expects the operating margin to remain high at around 19%.

In addition, CEO Armin Papperger recently suggested a potential international order intake of EUR 80 billion by the end of 2026, which should further accelerate revenue if Rheinmetall can scale up its operational capacity to the same extent. The expansion of production capacities is proceeding according to plan so far, including new lines in Switzerland, Germany, and Italy. Demand has surged particularly for the Skyranger and Skynex defense products. In the long term, Rheinmetall is targeting revenue of around EUR 50 billion, which would represent a fivefold increase. Currently, however, investors are somewhat unsettled and not yet fully prepared to pay today for the valuation scheme projected for 2029. As a result, Rheinmetall's share price has fallen by 30% in recent weeks. Analysts at JPMorgan remain positive with an "Overweight" rating and have set a 12-month price target of EUR 2,130. Patient investors could also find opportunities between EUR 1,350 and EUR 1,480.

CSG – Already Down Significantly After 3 Months

Those who participated in the major EuroNext IPO in January 2026 for the new defense hopeful CSG Group are now down 15% on their initial investment of EUR 25. The initiators timed the investors' rush into defense stocks perfectly. Although the Czech defense group has already expanded significantly with a 49% stake in Hirtenberg Defense Systems and recently secured a EUR 2.5 billion order for air defense systems, the stock is plummeting. However, the estimated figures for 2027 show a reasonable P/S ratio of just 2.5 and a low P/E ratio of 15. While this is disappointing for initial subscribers, it presents a good opportunity for new entrants.

Mutares – A major capital increase for US investments

A side note on Mutares. The subscription period for the new shares at EUR 24.50, totaling EUR 105 million or 20% of outstanding shares, runs until April 21. Anyone wishing to actively participate in the management's new US plans should wait until the end of the subscription period, as large investors have already secured shares in a special placement at EUR 24.50. The share price is likely to come under pressure again this week due to the large placement amount. A favorable entry point in the range of EUR 22.50 to 24.50 should therefore be possible even without purchasing subscription rights, as the capital market remains in a state of continued volatility with weak demand.

Investors have had a tough few weeks. High volatility continues to prevail, as announcements by US President Donald Trump continue to drive global events. Like other commodities, antimony is one of the key metals for the high-tech and defense industries. If the Strait of Hormuz cannot be reopened quickly, the Western world faces the threat of a standstill in some sectors. Antimony Resources can attract a great many investors in this environment, as they are among the future solutions to Western supply chain problems. For Rheinmetall, CSG, and Mutares, setting low buy-in limits could well make sense.

Conflict of interest

Pursuant to §85 of the German Securities Trading Act (WpHG), we point out that Apaton Finance GmbH as well as partners, authors or employees of Apaton Finance GmbH (hereinafter referred to as "Relevant Persons") currently hold or hold shares or other financial instruments of the aforementioned companies and speculate on their price developments. In this respect, they intend to sell or acquire shares or other financial instruments of the companies (hereinafter each referred to as a "Transaction"). Transactions may thereby influence the respective price of the shares or other financial instruments of the Company.

In this respect, there is a concrete conflict of interest in the reporting on the companies.

In addition, Apaton Finance GmbH is active in the context of the preparation and publication of the reporting in paid contractual relationships.

For this reason, there is also a concrete conflict of interest.

The above information on existing conflicts of interest applies to all types and forms of publication used by Apaton Finance GmbH for publications on companies.

Risk notice

Apaton Finance GmbH offers editors, agencies and companies the opportunity to publish commentaries, interviews, summaries, news and the like on news.financial. These contents are exclusively for the information of the readers and do not represent any call to action or recommendations, neither explicitly nor implicitly they are to be understood as an assurance of possible price developments. The contents do not replace individual expert investment advice and do not constitute an offer to sell the discussed share(s) or other financial instruments, nor an invitation to buy or sell such.

The content is expressly not a financial analysis, but a journalistic or advertising text. Readers or users who make investment decisions or carry out transactions on the basis of the information provided here do so entirely at their own risk. No contractual relationship is established between Apaton Finance GmbH and its readers or the users of its offers, as our information only refers to the company and not to the investment decision of the reader or user.

The acquisition of financial instruments involves high risks, which can lead to the total loss of the invested capital. The information published by Apaton Finance GmbH and its authors is based on careful research. Nevertheless, no liability is assumed for financial losses or a content-related guarantee for the topicality, correctness, appropriateness and completeness of the content provided here. Please also note our Terms of use.