June 10th, 2026 | 07:20 CEST

The SpaceX Frenzy and the Urge to Travel! Caution on Lufthansa, TUI, Zefiro Methane, Shell, and BP

The SpaceX frenzy continues. With an anticipated initial valuation approaching USD 2 trillion, Elon Musk is launching what could become the largest IPO since Saudi Aramco's debut in 2019. Back then, the Saudi oil giant raised nearly USD 30 billion. Musk is now targeting an astonishing USD 75 billion. At the proposed valuation, his 42% stake would make him the world's first trillionaire. The moment of truth will come in the next few days. As the FIFA World Cup kicks off, investors may briefly have to take their eyes off the pitch to avoid missing the first trading quotes. Whether Elon Musk can successfully bring SpaceX—with crown jewels such as Starlink, xAI, and its space operations—to the NASDAQ remains to be seen. One thing is certain: volatility is already elevated, and markets are highly nervous ahead of the listing. But SpaceX is not the only story in town. Following initial signs of de-escalation in the Gulf, investors are once again turning their attention to oil stocks, while travel and tourism shares are also moving back into focus. These are interesting times for flexible investors.

time to read: 7 minutes

|

Author:

André Will-Laudien

ISIN:

ZEFIRO METHANE CORP | CA98926D1069 | NEO: ZEFI , Shell PLC | GB00BP6MXD84 , BP PLC DL-_25 | GB0007980591 , LUFTHANSA AG VNA O.N. | DE0008232125 , TUI AG | DE000TUAG505

Table of contents:

Author

André Will-Laudien

Born in Munich, he first studied economics and graduated in business administration at the Ludwig-Maximilians-University in 1995. As he was involved with the stock market at a very early stage, he now has more than 30 years of experience in the capital markets.

Tag cloud

Shares cloud

Shell and BP: What Do the Giants Think About Climate Protection?

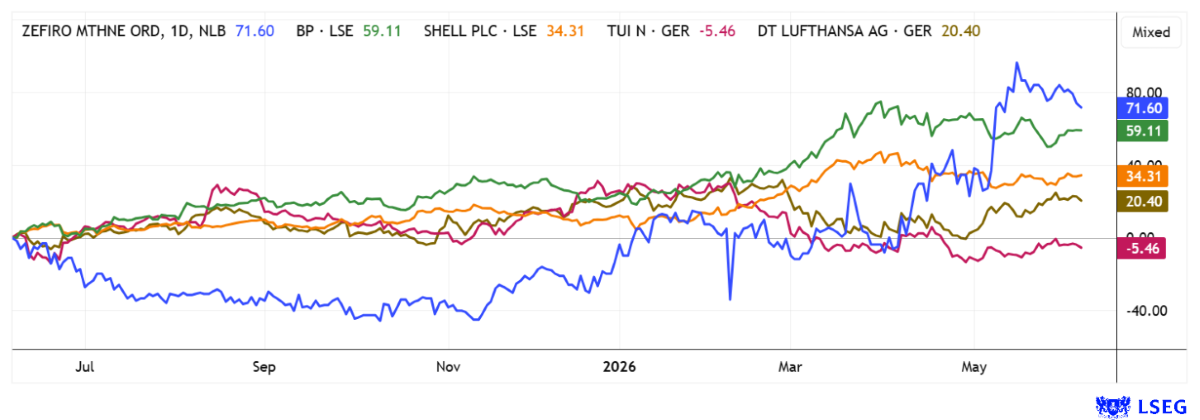

In light of the military incidents in the Gulf region, ESG considerations often take a back seat. But one thing has been a fact for years: oil and gas companies must adopt new criteria when dealing with our precious natural environment. Overall, progress is being made. Energy giants Shell and BP are now positioning themselves as key players in the energy transition without abandoning their roles as global oil and gas producers. Of course, they are attempting to gradually transition their business models toward lower-carbon energy sources, while the high profits from their core fossil fuel business continue to form the financial foundation. Shell aims to become a net-zero emissions company by 2050 and has already reduced its operational emissions by 36% by the end of 2025 compared to 2016. BP also recently reported a 37% reduction in its operational emissions compared to the base year of 2019, as well as a significant reduction in the emissions intensity of its energy products sold.

The question, however, is whether this progress is sufficient. While billions are flowing into charging infrastructure, hydrogen, biofuels, and renewable energy, both companies continue to invest substantial sums in new oil and gas projects. This balancing act is explained by current market realities. Global energy demand continues to grow, while security of supply has once again come into sharper focus amid geopolitical crises. Data from the International Energy Agency (IEA) illustrates that the global energy sector is already undergoing a structural transformation. In 2025, approximately USD 2.2 trillion flowed into clean energy, power grids, storage, and electrification worldwide. That is twice as much as the USD 1.1 trillion invested in oil, gas, and coal. The IEA also provides an important statistic regarding the energy mix: for the first time in decades, oil's share of global energy consumption has fallen below the 30% mark. It remains striking that electricity demand, driven by electric mobility, data centers, and artificial intelligence, shows no signs of slowing. In Asia, households are being encouraged to conserve electricity, while at the same time the AI industry consumes more every day.

This presents an interesting investment thesis for investors: Shell and BP have enormous cash flows, strong dividend programs of 5-6%, and are accelerating share buybacks, while simultaneously benefiting from long-term investments in new energy technologies. Should the energy transition take hold faster than expected, both companies have the financial resources to build market share in future markets. If, on the other hand, the transition proceeds more slowly, oil and gas operations will continue to generate high returns. Shell has posted a 24% gain over the past 12 months and is not far from its all-time high of around EUR 41.30. BP's annual performance stands at 43%, though its all-time high was over EUR 11 in the 2000s. For long-term investors, the oil industry is back on the radar, and when it comes to ESG, the focus here is also on the future.

Zefiro Methane: Tackling Legacy Environmental Liabilities

The energy transition is often associated with wind turbines, solar panels, or hydrogen, but it specifically also encompasses the fossil fuel industry. An innovative solution provider for immediate environmental protection is the Canadian company Zefiro Methane. The company takes a significantly more pragmatic approach, focusing on a massive legacy pollution problem in the North American oil and gas industry. Its main activity is the plugging of abandoned and orphaned oil and gas wells, during which climate-damaging methane emissions are measured and technologies developed to reduce these emissions permanently. In the US alone, according to estimates by the US Environmental Protection Agency (EPA) and various universities, there are between 2 and 3 million abandoned wells. A highly acclaimed study by Princeton University concludes that hundreds of thousands of tons of methane—a greenhouse gas whose global warming potential over a 20-year period is more than 80 times higher than that of CO₂—escape into the atmosphere annually from these so-called "orphan wells." The economic consequences are enormous. Experts estimate the cost of fully remediating these contaminated sites at USD 400-600 billion. And Zefiro is part of this remediation effort! The US government has already allocated approximately USD 4.7 billion through the Infrastructure Investment and Jobs Act for the decommissioning and remediation of abandoned oil and gas wells. Added to this are funding programs from individual states as well as private clients from the energy industry. This creates a market whose growth depends less on commodity prices than on long-term environmental budgets and regulatory requirements. For investors, this significantly increases the predictability of future revenues.

Operationally, the company is now delivering convincing results. In the first nine months of the current fiscal year, Zefiro generated revenue of approximately USD 33.2 million, representing growth of about 36% compared to the previous year. In the third quarter, revenue even rose by more than 58% to just under USD 11 million. At the same time, adjusted EBITDA reached approximately USD 4.25 million, demonstrating the increasing operational leverage of the business model. The latest expansion promises additional momentum. By acquiring Viking Well Service drilling rigs and other specialized equipment, Zefiro is significantly increasing its operational clout. Management expects additional revenue potential of more than USD 10 million per year from the newly acquired capacities alone. At the same time, the project pipeline is steadily filling up. Among the most important contracts is currently a USD 19.6 million project in the state of Ohio, as well as other activities in Pennsylvania, West Virginia, and New York. In some regions, Zefiro now holds an exceptionally strong market position and benefits from a limited competitive environment. In addition to traditional well plugging, methane monitoring is emerging as a high-margin growth segment. A recently completed 849-well program generated approximately USD 850,000 in revenue and is opening up additional follow-on business of about USD 450,000. That is quick cash flow!

This development is particularly noteworthy given the company's market capitalization of just around CAD 65 million. The appointment of renowned energy executive Correne Loeffler as CFO, along with the recent CAD 4.5 million investment from European investors, underscores the company's ambitions for its next phase of growth. Those who think in terms of oil and gas are looking to the future; Zefiro Methane is growing alongside the industry's legacy issues. Buy in!

CEO Catherine Flax commented on current developments at the 19th International Investment Forum.

TUI and Lufthansa: Kerosene Tightens as Travel Becomes a Luxury

In the tourism sector, the profit formula is simple. If tensions ease, there will be double-digit percentage gains, because ultimately, hopes for a turnaround are reigniting for European travel market leader TUI and the largest airline, Lufthansa. In contrast, a permanent closure of the Strait of Hormuz would be a showstopper for kerosene production in Europe. It is not yet clear whether reserves will be sufficient for the vacation months. Looking at the valuations of the two companies, TUI has a P/E ratio of just 6.3 based on 2026 estimates, with approximately 5% revenue growth. Analysts on the LSEG platform also expect continued earnings growth in the coming years, with EPS rising from EUR 0.99 to EUR 1.40 in 2027 and EUR 1.76 in 2028. The 12-month price target is calculated at an average of EUR 10.25, roughly 55% above the current share price of EUR 6.65. Whether this actually happens, of course, depends on a reduction in geopolitical conflicts and an easing of inflationary pressures. Due to various cost increases, private households no longer have the same budgets as they did during the record-breaking travel years of 2017/18. The situation is similar at Lufthansa. A P/E ratio of 5.2 is expected for 2028; investors should also take note of the price-to-book ratio. The book value of equity is 10.32, about 25% above yesterday's closing price of EUR 8.10. Experts on the LSEG platform expect prices around EUR 9.15 in 12 months. The sector is in a holding pattern but could continue to correct due to the crisis.

The capital markets have various trends to digest. For now, there is little relief in the Gulf or Ukraine, meaning Western nations remain under pressure. However, as inflation is rising, the new Fed Chair, Kevin Warsh, will likely recommend an interest rate hike to the US President. And then there are the major IPOs: SpaceX, OpenAI, Anthropic, and Databricks. No wonder some air is being let out ahead of such events.

Conflict of interest

Pursuant to §85 of the German Securities Trading Act (WpHG), we point out that Apaton Finance GmbH as well as partners, authors or employees of Apaton Finance GmbH (hereinafter referred to as "Relevant Persons") currently hold or hold shares or other financial instruments of the aforementioned companies and speculate on their price developments. In this respect, they intend to sell or acquire shares or other financial instruments of the companies (hereinafter each referred to as a "Transaction"). Transactions may thereby influence the respective price of the shares or other financial instruments of the Company.

In this respect, there is a concrete conflict of interest in the reporting on the companies.

In addition, Apaton Finance GmbH is active in the context of the preparation and publication of the reporting in paid contractual relationships.

For this reason, there is also a concrete conflict of interest.

The above information on existing conflicts of interest applies to all types and forms of publication used by Apaton Finance GmbH for publications on companies.

Risk notice

Apaton Finance GmbH offers editors, agencies and companies the opportunity to publish commentaries, interviews, summaries, news and the like on news.financial. These contents are exclusively for the information of the readers and do not represent any call to action or recommendations, neither explicitly nor implicitly they are to be understood as an assurance of possible price developments. The contents do not replace individual expert investment advice and do not constitute an offer to sell the discussed share(s) or other financial instruments, nor an invitation to buy or sell such.

The content is expressly not a financial analysis, but a journalistic or advertising text. Readers or users who make investment decisions or carry out transactions on the basis of the information provided here do so entirely at their own risk. No contractual relationship is established between Apaton Finance GmbH and its readers or the users of its offers, as our information only refers to the company and not to the investment decision of the reader or user.

The acquisition of financial instruments involves high risks, which can lead to the total loss of the invested capital. The information published by Apaton Finance GmbH and its authors is based on careful research. Nevertheless, no liability is assumed for financial losses or a content-related guarantee for the topicality, correctness, appropriateness and completeness of the content provided here. Please also note our Terms of use.