April 27th, 2026 | 07:40 CEST

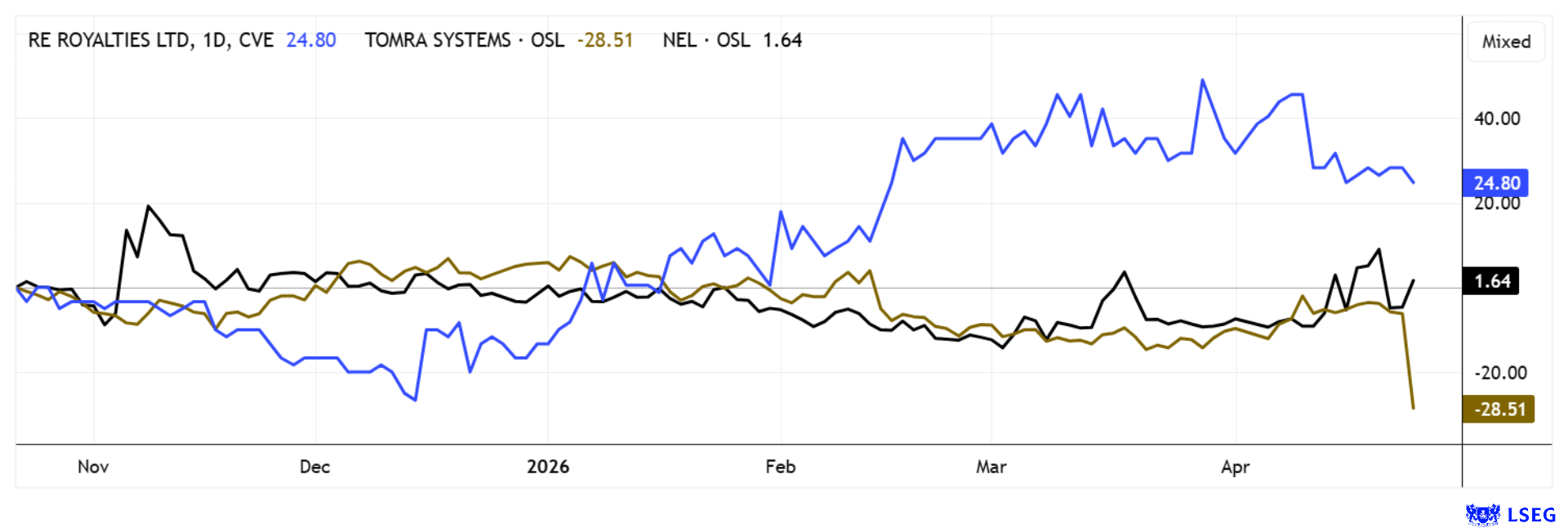

Rockets, Returns, Recycling: Investors Sense Geopolitical Tailwinds for Nel ASA, RE Royalties, and Tomra Systems

In an environment of political instability and growing uncertainty, one thing is clear: investments in sustainability are no longer merely an ESG issue, but a geopolitical and economic imperative. This is because dependence on fossil fuels is increasingly perceived as a strategic risk. Accordingly, pressure is mounting to prioritize alternative energy sources and sustainable infrastructure. This opens up a structural growth market for investors that extends far beyond short-term crisis responses. Companies across the value chain are in the spotlight, benefiting to varying degrees from this transformation. While RE Royalties, as a financier of sustainable projects, relies on stable cash flows from renewable energy plants, Tomra Systems addresses key resource issues of the future with recycling and circular economy solutions. Nel ASA, in turn, embodies the hope for a hydrogen economy, though it is still grappling with the typical challenges of a nascent industry. We do the math.

time to read: 5 minutes

|

Author:

André Will-Laudien

ISIN:

RE ROYALTIES LTD | CA75527Q1081 | TSXV: RE , OTCQX: RROYF , NEL ASA NK-_20 | NO0010081235 , TOMRA SYSTEMS ASA NK 1 | NO0005668905

Table of contents:

Author

André Will-Laudien

Born in Munich, he first studied economics and graduated in business administration at the Ludwig-Maximilians-University in 1995. As he was involved with the stock market at a very early stage, he now has more than 30 years of experience in the capital markets.

Tag cloud

Shares cloud

RE Royalties - A billion-dollar market for decentralized energy as a strategic lever

It is no coincidence that things are going particularly well for the ESG-compliant financier RE Royalties at the moment. Amid growing investments in renewable energy, the Canadian company is increasingly positioning itself as a specialized investor with a business model whose structure is more reminiscent of commodity financing than that of traditional energy companies. Instead of operating plants itself, the company takes a stake in the revenues of solar, wind, or storage projects, thereby creating a revenue base that is more closely tied to production volume than to profit margins. This innovative structure is unique in the financial sector and reduces sensitivity to rising operating costs. At the same time, the visibility of long-term cash flows increases, a factor that is increasingly valued in the capital markets environment amid growing interest rates and inflation volatility. Over the years, a broadly diversified portfolio has emerged that now comprises more than 120 individual investments in North and South America as well as in selected Asian markets, thereby offering solid regional and technological diversification.

The North American energy market is currently developing particularly dynamically, where digitalization, electromobility, and the rising electricity demand from data centers are driving structural demand. In this environment, the company is continuously expanding its investments and specifically targeting projects in the commercial and industrial segments that require a long-term, predictable energy supply. This is an interesting and smart niche that also provides investors with a sustainable structure. Strategic adjustments are currently underway aimed at increasing financial flexibility while simultaneously streamlining the balance sheet structure. Previous financing instruments have been gradually phased out, while new projects with a selective risk profile are being evaluated in parallel. Projects with a volume of approximately CAD 20 million are currently in concrete negotiations, while a broader pipeline of about CAD 200 million signals the potential for significant scaling of the business model.

Crucially, the operational platform is already designed to handle a multiple of the current investment volume without incurring proportionally rising administrative costs.

The company's dividend policy, which has proven remarkably stable in recent years, remains particularly attractive to investors. On an annual basis, the dividend currently amounts to approximately CAD 0.04 per share, which, at the current valuation, approaches a double-digit percentage yield and thus represents a rare combination of growth prospects and recurring income in the small-cap segment. Nevertheless, the market capitalization of approximately CAD 16 million indicates that the market has so far only partially priced in the long-term earnings potential. This is precisely where the recently initiated strategic review comes in, examining not only partnerships and co-investments but also structural options for value enhancement. The involvement of external financial advisors underscores management's commitment to shaping the next phase of development not by chance but deliberately, and to systematically increasing the company's value. The stock is currently extremely cheap.

In an interview with IIF host Lyndsay Malchuk, CEO Bernard Tan describes his medium-term business strategy.

Tomra Systems – Is the Correction a Buying Opportunity?

Tomra Systems shares have taken a serious hit. The Norwegian company has recently experienced a significant downward trend, attributable less to a single trigger than to an accumulation of fundamental and earnings-related disappointments. The recycling segment remains at the heart of the weakness; it has suffered noticeably from investment reluctance in Europe and North America in recent quarters and at times recorded revenue declines of over 30%. At the same time, order intake in this segment has weakened significantly, which has unsettled the market regarding the visibility of future growth rates. The negative trend continued in the first quarter. Sales of recycling machines fell by 19% in a challenging market environment, though revenue from reverse vending machines and food sorting systems rose by 12% and 13%, respectively.

At the operational level, margins remain solid, but the market is currently clearly focused on the cyclical weakness in order intake and uncertainty regarding customers' willingness to invest. Institutional investors in particular have viewed this shift in the segment with increasing skepticism, as the stock's high valuation has historically been based heavily on the assumption of sustainable recycling growth. After several years of high multiples, a normalization of growth expectations is now being priced in. With the sharp downward move to EUR 8.25 last week, the valuation has fallen significantly. A 2027 P/E ratio of 12.3 is now in play, and the dividend yield has climbed to 4.5%. On the LSEG Refinitiv platform, 11 out of 13 analysts are bullish. On average, they expect a 12-month target price of NOK 144 or EUR 13.16—a potential upside of over 60%. If a bottom of around EUR 8.50 can form in the coming days, the top tech stock from Norway would be a long-term value pick.

Nel ASA – The comeback is a long time coming

Things are quite volatile for our second Norwegian stock, Nel ASA. Last week, the stock went on a real rollercoaster ride. The Q1 figures were in line with lowered expectations. With revenue down 5% to NOK 148 million, EBITDA also came in at minus NOK 100 million, and the net loss decreased only marginally to NOK 144 million. The job cuts are slowly making themselves felt, though order intake also plummeted again by 73% to just NOK 85 million. The cash position stood at NOK 1.44 billion at the end of the quarter, and there is now hope for Q2. This is because Oslo expects EU funding of EUR 11 million as well as the commercial launch of a new alkaline platform. Insider and Board Chairman Arvid Moss apparently also sees good opportunities at the moment and bought 100,000 shares of the company last Friday. It was enough for a daily gain of 7%. After several breakout attempts, technical analysts are taking notice, as momentum is currently clearly on the buyers' side. Speculators should start positioning themselves, as the next move above the EUR 0.22 mark could be highly dynamic.

For investors, an exciting dynamic is currently emerging between defensive cash flow models, turnaround potential, and cyclical valuation adjustments. While RE Royalties, with stable revenue streams and double-digit return profiles, bears the hallmarks of an undervalued infrastructure stock, Nel ASA remains a classic growth stock whose valuation depends heavily on the pace of the hydrogen economy and political stimulus measures. The weak performance of Tomra Systems ASA, on the other hand, appears less like a structural breakdown and more like a long-overdue revaluation following years of high expectations.

Conflict of interest

Pursuant to §85 of the German Securities Trading Act (WpHG), we point out that Apaton Finance GmbH as well as partners, authors or employees of Apaton Finance GmbH (hereinafter referred to as "Relevant Persons") currently hold or hold shares or other financial instruments of the aforementioned companies and speculate on their price developments. In this respect, they intend to sell or acquire shares or other financial instruments of the companies (hereinafter each referred to as a "Transaction"). Transactions may thereby influence the respective price of the shares or other financial instruments of the Company.

In this respect, there is a concrete conflict of interest in the reporting on the companies.

In addition, Apaton Finance GmbH is active in the context of the preparation and publication of the reporting in paid contractual relationships.

For this reason, there is also a concrete conflict of interest.

The above information on existing conflicts of interest applies to all types and forms of publication used by Apaton Finance GmbH for publications on companies.

Risk notice

Apaton Finance GmbH offers editors, agencies and companies the opportunity to publish commentaries, interviews, summaries, news and the like on news.financial. These contents are exclusively for the information of the readers and do not represent any call to action or recommendations, neither explicitly nor implicitly they are to be understood as an assurance of possible price developments. The contents do not replace individual expert investment advice and do not constitute an offer to sell the discussed share(s) or other financial instruments, nor an invitation to buy or sell such.

The content is expressly not a financial analysis, but a journalistic or advertising text. Readers or users who make investment decisions or carry out transactions on the basis of the information provided here do so entirely at their own risk. No contractual relationship is established between Apaton Finance GmbH and its readers or the users of its offers, as our information only refers to the company and not to the investment decision of the reader or user.

The acquisition of financial instruments involves high risks, which can lead to the total loss of the invested capital. The information published by Apaton Finance GmbH and its authors is based on careful research. Nevertheless, no liability is assumed for financial losses or a content-related guarantee for the topicality, correctness, appropriateness and completeness of the content provided here. Please also note our Terms of use.