March 4th, 2026 | 06:55 CET

New EU standards aim to secure the future of e-mobility! BYD, Nio, Group Eleven Resources, and VW

With the Alternative Fuels Infrastructure Regulation (AFIR), the European Union has been creating binding minimum standards for publicly accessible charging points since the beginning of 2026. In addition, new subsidies have been introduced in many EU countries to promote e-mobility, even though the coffers are empty due to high defense spending. Meanwhile, the overall European vehicle market came under noticeable pressure in January. According to the latest data from the industry association ACEA, new vehicle registrations fell by just under 4% compared to the previous year, marking the first decline in months and reflecting the difficult overall market. However, a clear trend is emerging within this development: electrification is continuing to advance and shifting market shares in favor of battery electric vehicles. At the same time, the next Middle East conflict is unfolding, with oil prices rising sharply above USD 82 per barrel of Brent. This is providing a strong tailwind for alternative drive systems that can withstand global hysteria. Risk-conscious investors should now revise their portfolio structures.

time to read: 5 minutes

|

Author:

André Will-Laudien

ISIN:

BYD CO. LTD H YC 1 | CNE100000296 , NIO INC.A S.ADR DL-_00025 | US62914V1061 , GROUP ELEVEN RESOURCES CORP | CA39944P1018 | TSXV: ZNG , OTCQB: GRLVF , VOLKSWAGEN AG VZO O.N. | DE0007664039

Table of contents:

Author

André Will-Laudien

Born in Munich, he first studied economics and graduated in business administration at the Ludwig-Maximilians-University in 1995. As he was involved with the stock market at a very early stage, he now has more than 30 years of experience in the capital markets.

Tag cloud

Shares cloud

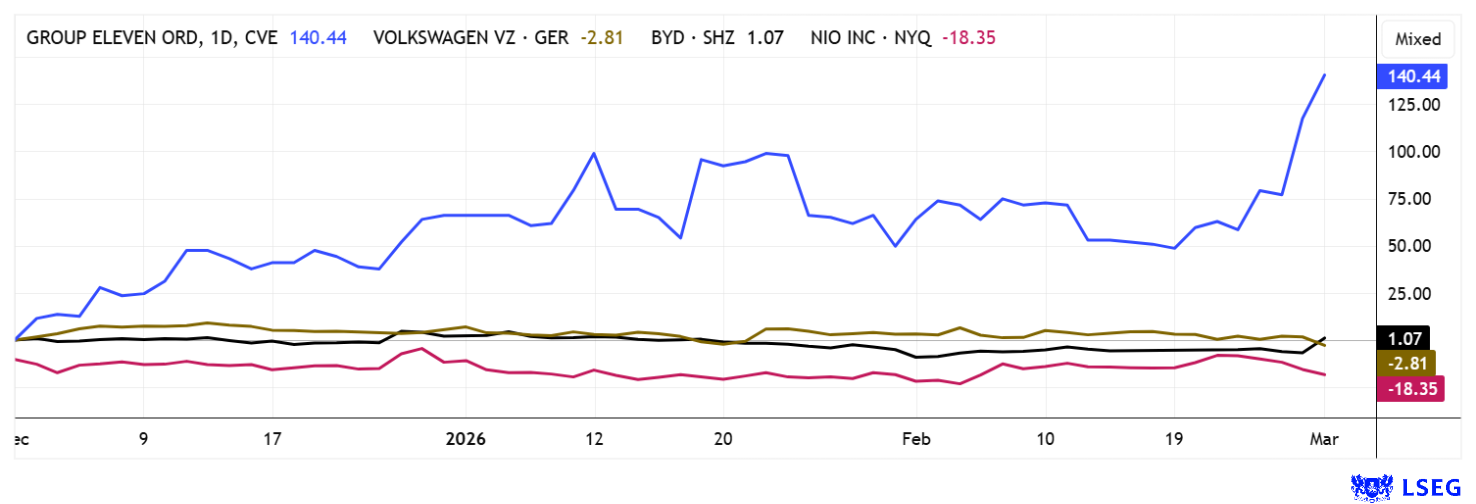

Group Eleven Resources – Critical metals at the forefront

Brussels is waking up! Europe is now stepping up its efforts to secure an independent supply of raw materials in order to reduce strategic dependencies and secure industrial value creation within its own economic area. Group Eleven Resources is very well-positioned in this environment. The company focuses on high-grade base metal deposits in Ireland. Through systematic drilling programs, it is attempting to build up substantial resources of critical size in order to create strategic weight.

The focus of its activities is the PG West project with the Ballywire discovery, which is increasingly evolving from a classic zinc-lead structure into a complex multi-metal system. Since the discovery was announced in 2022, more than 75 drill holes have been completed and evaluated, resulting in a robust geological model of the system. The most significant drill hole to date, No. 25-3552-51, extends a previously reported interval to a total of 52.3 m, averaging 10.3% Zn+Pb, 330 g/t silver, and 0.40% copper. Within this interval, 8.4 m stand out with 18.2% Zn+Pb, 1,776 g/t silver, and 2.21% copper, complemented by detectable antimony content, suggesting a high-grade, polymetallic core zone. In addition, three deeper copper-silver zones were identified in the same drill hole, including 3.7 m grading 225 g/t silver and 1.03% copper, supporting the hypothesis of a structurally controlled Cu-Ag system over at least 350 m of strike length. Additional geochemical analyses also show significant germanium and gallium grades over several tens of meters, further increasing the metallurgical value.

The most ambitious program in the company's history is currently underway, with four drilling rigs operating in parallel. These are expected to complete a total of more than 20,000 m of drilling in 2026, of which approximately 85% will be at Ballywire. In addition, the company holds a 77.64% interest in the neighbouring Stonepark project, which is located in the immediate vicinity of Glencore plc's Pallas Green deposit and has a separate zinc-lead resource. The regional integration is underscored by the current shareholder structure. Glencore Canada will retain its approximately 13.6% interest as part of current capital measures, and the ongoing bought deal private placement of 10 million shares plus a 15% over-allotment option at CAD 0.90 is convincing. Against the backdrop of high-grade, powerful drill sections and increasing evidence of an extensive copper-silver system, Group Eleven is currently presenting itself from its strongest side. The current exploration program offers substantial upside potential, and investors should take advantage of the current volatility and jump in boldly in the CAD 0.95 to 1.15 corridor. With a market capitalization of just under CAD 300 million, the multi-metal story is only just beginning!

BYD versus NIO – Two paths in the dynamic Chinese EV market

Car manufacturers depend on stable supply chains! China's BYD is starting 2026 with a clear European strategy and a strong focus on local production. The new plant in Szeged, Hungary, with a planned capacity of 200,000 vehicles per year, not only allows BYD to circumvent EU additional tariffs but also creates proximity to customers and EU supply chains. This is complemented by battery assembly, R&D in Budapest, and a planned plant in Turkey, which spreads geopolitical risks and increases customs flexibility with EU concessions. With a recently acquired market share of just under 1% in Europe, BYD is positioning itself aggressively against established manufacturers such as Volkswagen and Stellantis. In terms of valuation, the stock appears very attractive with a 2026 P/E ratio of 14. The upcoming annual figures on March 26 could provide possible upside momentum.

Chinese competitor NIO Inc. reported deliveries of 20,797 electric vehicles in February, up 57.6% year-on-year, although the volume is seasonally lower than in the previous month. The Spring Festival shifted production and delivery rhythms, so the decline compared to January is due to calendar effects. The core NIO brand remains the driving force with over 15,000 units, while sub-brands such as Onvo and Firefly are still building economies of scale. Discount campaigns continue to signal intense price competition in the Chinese domestic market. Compared to BYD, NIO is focusing more on its premium positioning, high brand loyalty, and technological differentiation. However, the all-round talent BYD is strategically diversifying strongly and focusing on cost leadership. While BYD impresses with its solidity, NIO appears somewhat more agile but also more susceptible to fluctuations in demand. Overall, both manufacturers are taking different paths to assert themselves in the growing but highly competitive EV market in 2026. While BYD is already making money, NIO shareholders will likely have to wait until 2030.

VW reaches the 2 million electric vehicle mark, but the share price still falls

Good news is coming out of Wolfsburg. While many stock market traders are lamenting the high December prices of well over EUR 110, the latest reports are really good. With the delivery of its two millionth electric vehicle, VW has reached an important milestone in its own electrification strategy, symbolically represented by an ID.3 from Zwickau. This model marks the technological starting point, while the actual bestseller is the ID.4. Together with the ID.5 coupe offshoot and the cool ID Buzz, it is a well-rounded package! Of the two million electric vehicles sold to date, around 628,000 were ID.3s, which laid the foundation for the broad range from the compact to the small car segment. Overall, VW is demonstrating that its model mix of everyday vehicles, bus revival, and SUV power is driving forward its hoped-for electrification agenda. Then there are the well-performing combustion engines. Why the stock, with a 2026 P/E ratio of 4.5 and a dividend yield of over 6%, is failing to gain traction will likely become clear to investors when the annual results are released on March 10. Ultra exciting and once again attractively valued!

The stock markets are in the eye of the storm. While defense stocks are finding new buyers on an almost daily basis, established companies, like those in the automotive sector, are struggling. Future suppliers of critical metals are the focus of attention. This is where Group Eleven can shine!

Conflict of interest

Pursuant to §85 of the German Securities Trading Act (WpHG), we point out that Apaton Finance GmbH as well as partners, authors or employees of Apaton Finance GmbH (hereinafter referred to as "Relevant Persons") currently hold or hold shares or other financial instruments of the aforementioned companies and speculate on their price developments. In this respect, they intend to sell or acquire shares or other financial instruments of the companies (hereinafter each referred to as a "Transaction"). Transactions may thereby influence the respective price of the shares or other financial instruments of the Company.

In this respect, there is a concrete conflict of interest in the reporting on the companies.

In addition, Apaton Finance GmbH is active in the context of the preparation and publication of the reporting in paid contractual relationships.

For this reason, there is also a concrete conflict of interest.

The above information on existing conflicts of interest applies to all types and forms of publication used by Apaton Finance GmbH for publications on companies.

Risk notice

Apaton Finance GmbH offers editors, agencies and companies the opportunity to publish commentaries, interviews, summaries, news and the like on news.financial. These contents are exclusively for the information of the readers and do not represent any call to action or recommendations, neither explicitly nor implicitly they are to be understood as an assurance of possible price developments. The contents do not replace individual expert investment advice and do not constitute an offer to sell the discussed share(s) or other financial instruments, nor an invitation to buy or sell such.

The content is expressly not a financial analysis, but a journalistic or advertising text. Readers or users who make investment decisions or carry out transactions on the basis of the information provided here do so entirely at their own risk. No contractual relationship is established between Apaton Finance GmbH and its readers or the users of its offers, as our information only refers to the company and not to the investment decision of the reader or user.

The acquisition of financial instruments involves high risks, which can lead to the total loss of the invested capital. The information published by Apaton Finance GmbH and its authors is based on careful research. Nevertheless, no liability is assumed for financial losses or a content-related guarantee for the topicality, correctness, appropriateness and completeness of the content provided here. Please also note our Terms of use.