May 21st, 2026 | 07:45 CEST

150% Opportunity and Risk at the Same Time! Kobo Resources on the Verge of Gold, TUI, easyJet, and Lufthansa Attractively Valued

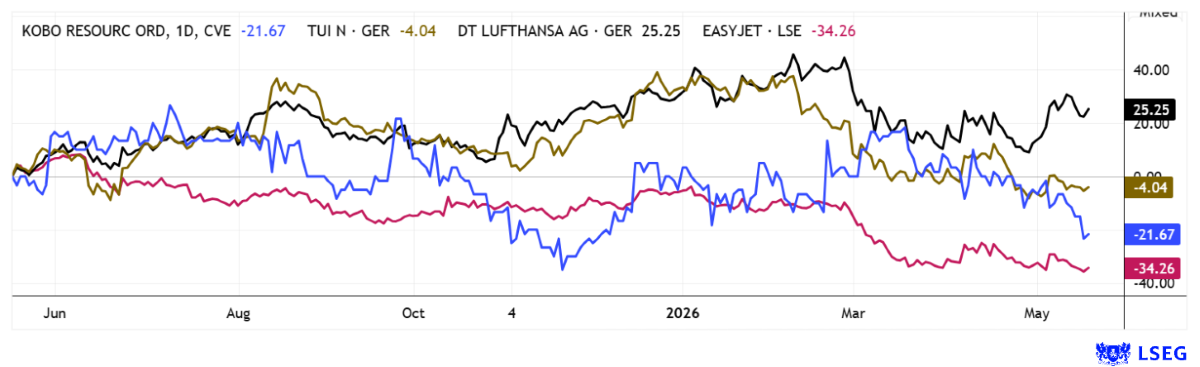

With extreme volatility expected in 2026, one thing remains clear: gold serves as a portfolio stabilizer. In an environment of rising inflation, increasing interest rates, and soaring commodity prices, precious metals have performed strongly so far. Due to the Iran conflict, travel and tourism stocks in particular have come under pressure, as they are affected by weaker travel demand, tighter household budgets, and ultimately higher fuel costs. But those who look beyond the immediate horizon recognize that crises are temporary, and fear-driven valuation discounts can create medium-term buying opportunities. For risk-conscious investors, these scenarios present investment opportunities that would not be expected under normal circumstances. For instance, Deutsche Lufthansa is currently trading at around 30% below its book value, while TUI is trading at a P/E ratio of about 5. Is this irrational? In the short term, perhaps not. In the long term, however, it may well be. As the saying goes: buy when the cannons thunder.

time to read: 5 minutes

|

Author:

André Will-Laudien

ISIN:

KOBO RESOURCES INC | CA49990B1040 | TSXV: KRI , TUI AG NA O.N. | DE000TUAG505 , EASYJET PLC LS-_27285714 | GB00B7KR2P84 , LUFTHANSA AG VNA O.N. | DE0008232125

Table of contents:

Author

André Will-Laudien

Born in Munich, he first studied economics and graduated in business administration at the Ludwig-Maximilians-University in 1995. As he was involved with the stock market at a very early stage, he now has more than 30 years of experience in the capital markets.

Tag cloud

Shares cloud

TUI – As Cheap as During the Pandemic

Anyone looking at the German stock market will be a bit puzzled by TUI. After all, Europe's largest tourism group was already severely battered between 2021 and 2022. To secure its survival, the German government provided state aid totalling over EUR 750 million. This aid was fully repaid by 2023. Following an interim recovery, the stock price reached levels above EUR 9.50 again in early 2026. However, since the US attacks on Iran, the stock has come under pressure once again. The macroeconomic environment is particularly burdensome, having hindered the operational recovery process. Following significant periods of losses, the stock is currently trading only marginally above its 52-week low at around EUR 6.10. While the Q1 figures satisfied analysts, the loss per share still stood at EUR 0.56. Surprisingly, the annual estimates for 2026/27 are clearly in positive territory at EUR 1.12 and EUR 1.43, respectively. This brings the P/E ratio to around 5, while a 2027 dividend yield of 3.5% is expected at this valuation level. The neutral observer is pleased with these conditions because, once geopolitical pressure is over, the share price is likely to soar again. The LSEG Refinitiv 12-month consensus stands at a generous EUR 10.50—a potential gain of over 60%.

Lufthansa and easyJet – Painful Adjustment Processes, but Low Valuation

Equally disheartening is the situation at the two airlines, Lufthansa and easyJet. With revenue well over EUR 40 billion in Europe, Deutsche Lufthansa is the clear market leader. As a multi-brand provider, the airline operates in both the business and low-cost carrier segments. The Lufthansa Group now includes the brands Lufthansa, SWISS, Austrian Airlines, Brussels Airlines, Eurowings, Discover Airlines, and ITA Airways. The latter is to be integrated into the group as soon as possible, thereby completing the European portfolio. With the recent closure of Cityline, the most attractive routes were transferred to Discover and Eurowings. This surprising move allows management to retire older aircraft early and remove inefficient routes from the schedule. Ultimately, personnel costs were likely also a factor in the swift shutdown following the final flight in April. The group effectively offset rising kerosene prices through international deliveries and considers itself well-prepared for the summer season. Analysts on the LSEG Refinitiv platform currently do not expect any significant price increases, with target prices around EUR 8.48. Consequently, the book value of equity is nearly 50% higher!

The mood is likely not quite as positive as that of low-cost competitor easyJet. Here, provisions and high kerosene prices are weighing on the company. As a result, analysts have reduced the number of "Buy" recommendations, though the average price target remains 30% above the last quoted price. With additional routes in Europe, the group expects revenue growth of about 10% per annum through 2030, even under the current scenario. The P/E ratio of 19.5 in 2026—which has risen due to the crisis—is expected to fall to about 5 by 2028. Perhaps the current adjustment processes are a good trigger for a medium-term entry, as the share price has fallen back to 2023 lows over the past week. In 2025, the price had already reached over EUR 7—a respectable target in good times. Currently, the price is just under EUR 4, attracting traders and investors alike!

Kobo Resources – A Very Affordable Entry Point in West Africa

Anyone feeling the urge to travel right now should also consider a trip to West Africa. Because in the stable region of Côte d'Ivoire, there is not only a good climate and an already well-developed infrastructure, but also a thriving tourism industry. And, the country has a lot of gold! Over the past 10 years, West Africa has quietly but consistently developed into one of the world's most dynamic gold corridors. The Côte d'Ivoire is considered one of the more prominent locations. Economically, the country is growing at about 6% annually, driven by infrastructure investments and commodity exports, while GDP now stands at just under USD 95 billion. At the same time, according to current industry estimates, the country produces around 50-60 tons of gold per year, establishing itself among the second tier of globally relevant gold-producing nations.

In this competitive landscape, Kobo Resources positions itself as a classic early-stage explorer with a compelling opportunity profile. The company operates in a geologically established gold belt where several deposits in the range of tens of millions of ounces have already been proven. The strategic approach is clearly focused on value creation through exploration. Projects are to be systematically developed from the anomaly stage to a defined resource, ideally along existing infrastructure, to limit Capex risks and shorten development times.

IIF host Lyndsay Malchuk in conversation with CEO Edward Gosselin about the prospects for Kobo Resources in Côte d'Ivoire.

The focus is on the Kossou project, which is increasingly emerging as the geological anchor of the portfolio. Since 2023, over 40,000 m of drilling have been completed there, supplemented by extensive trenching programs along a mineralized structure more than 9 km long. The latest results show consistent gold mineralization, including 13 m at 1.77 g/t, as well as high-grade zones up to 2 m averaging over 26 g/t gold. At the same time, Kotobi is emerging as a second pillar, where several large-scale gold anomalies have already been identified and which is now moving into the first drilling phase. This multi-asset strategy reduces dependence on a single project while simultaneously increasing capital requirements at a stage when exploration success has not yet translated into cash flows.

Financially, Kobo remains in the classic "discovery phase." Approximately 119 million outstanding shares and a market capitalization of about CAD 28.5 million are offset by growing exploration expenses, which are to be supported by approximately CAD 5.5 million in financing. The key catalyst remains the first resource estimate expected in 2026. **Until then, the share price is likely to remain relatively unspectacular; after all, prices as low as CAD 0.36 were seen already in 2026, and yesterday shares were trading around CAD 0.24. Well done to those who are positioned early!

Anyone looking to generate returns right now must be flexible and able to switch between asset classes effectively. While easyJet is heading toward a multi-year low in its share price, TUI and Lufthansa are available at very favourable fundamental valuations. The up-and-coming gold stock Kobo Resources has also seen significantly higher prices in the past. Those who act now on this selection are seizing the moment for a chance to double their investment in the medium term. Broad diversification reduces portfolio volatility.

Conflict of interest

Pursuant to §85 of the German Securities Trading Act (WpHG), we point out that Apaton Finance GmbH as well as partners, authors or employees of Apaton Finance GmbH (hereinafter referred to as "Relevant Persons") currently hold or hold shares or other financial instruments of the aforementioned companies and speculate on their price developments. In this respect, they intend to sell or acquire shares or other financial instruments of the companies (hereinafter each referred to as a "Transaction"). Transactions may thereby influence the respective price of the shares or other financial instruments of the Company.

In this respect, there is a concrete conflict of interest in the reporting on the companies.

In addition, Apaton Finance GmbH is active in the context of the preparation and publication of the reporting in paid contractual relationships.

For this reason, there is also a concrete conflict of interest.

The above information on existing conflicts of interest applies to all types and forms of publication used by Apaton Finance GmbH for publications on companies.

Risk notice

Apaton Finance GmbH offers editors, agencies and companies the opportunity to publish commentaries, interviews, summaries, news and the like on news.financial. These contents are exclusively for the information of the readers and do not represent any call to action or recommendations, neither explicitly nor implicitly they are to be understood as an assurance of possible price developments. The contents do not replace individual expert investment advice and do not constitute an offer to sell the discussed share(s) or other financial instruments, nor an invitation to buy or sell such.

The content is expressly not a financial analysis, but a journalistic or advertising text. Readers or users who make investment decisions or carry out transactions on the basis of the information provided here do so entirely at their own risk. No contractual relationship is established between Apaton Finance GmbH and its readers or the users of its offers, as our information only refers to the company and not to the investment decision of the reader or user.

The acquisition of financial instruments involves high risks, which can lead to the total loss of the invested capital. The information published by Apaton Finance GmbH and its authors is based on careful research. Nevertheless, no liability is assumed for financial losses or a content-related guarantee for the topicality, correctness, appropriateness and completeness of the content provided here. Please also note our Terms of use.