March 16th, 2026 | 09:10 CET

Oil Crisis 5.0 is Pure Fiction: Shell, American Atomics, and E.ON Call the Shots

The same old refrain every day: We are running out of oil! The Strait of Hormuz is about to be closed! This is scaremongering by the oil lobby, which has been suffering from relatively low oil prices of USD 60 to USD 80 for the past two years. So a bit of stress is injected into the system, a few images of burning oil facilities appear in the news, and prices quickly start soaring again. Oil prices have already surged well above USD 100 twice on strong momentum - but that is not what scarcity looks like! The "Peak Oil" myth has already been debunked several times. In reality, with all the renewable alternatives to fossil fuels, oil demand has reached a peak, which, according to experts, is almost exactly 100 million barrels per day. And as recent studies show, there is still enough oil on Earth to last well over 200 years. So: take advantage of short-selling opportunities in the oil market as the conflict draws to a close, ride Shell's current oil wave as long as possible, and keep an eye on upcoming energy favorites such as American Atomics, RWE, or E.ON. Then your portfolio will be smiling - without falling into sheer panic.

time to read: 5 minutes

|

Author:

André Will-Laudien

ISIN:

Shell PLC | GB00BP6MXD84 , AMERICAN ATOMICS INC | CA0240301089 | CSE: NUKE , E.ON SE NA O.N. | DE000ENAG999

Table of contents:

Author

André Will-Laudien

Born in Munich, he first studied economics and graduated in business administration at the Ludwig-Maximilians-University in 1995. As he was involved with the stock market at a very early stage, he now has more than 30 years of experience in the capital markets.

Tag cloud

Shares cloud

From Ore to Reactor: American Atomics is Building an Integrated Uranium Strategy

Amid rising geopolitical tensions and wildly fluctuating energy prices, nuclear energy is once again taking center stage in global energy policy. Rising costs for fossil fuels highlight the vulnerability of many industries to supply risks and intensify the pressure to expand stable, long-term, and predictable energy sources. At the same time, new structural trends, such as the rapidly rising electricity demand from AI data centers, are further driving the demand for baseload energy. Amazon, Microsoft, and Meta are among the tech giants that have already acquired stakes in power generators and are pushing new technologies.

In this environment, the nuclear industry is undergoing a strategic reassessment internationally, with small modular reactors (SMRs) in particular being viewed as a key component of future energy systems. With this development, securing Western uranium supply chains is increasingly becoming a central focus of political and economic strategies. This is precisely where American Atomics Inc. positions itself, with the goal of establishing an integrated value chain in the North American uranium sector. The business model encompasses traditional exploration activities but also includes, in the long term, the subsequent stages of the fuel cycle through to preparation for modern reactor technologies. This approach directly addresses a key US energy policy issue - reducing dependence on foreign uranium suppliers and strengthening national production capacities.

Operationally, the company focuses on the historically significant uranium district in the Lisbon Valley in the US state of Utah. There, American Atomics has entered into an option agreement that grants the company the opportunity to gradually acquire up to 80% of an extensive claim package. The project comprises over two hundred claims and covers a large portion of the eastern flank of the geological structure, while previous mining activities took place primarily on the western side. Historical production of approximately 78 million pounds of uranium oxide in the region underscores the area's geological potential.

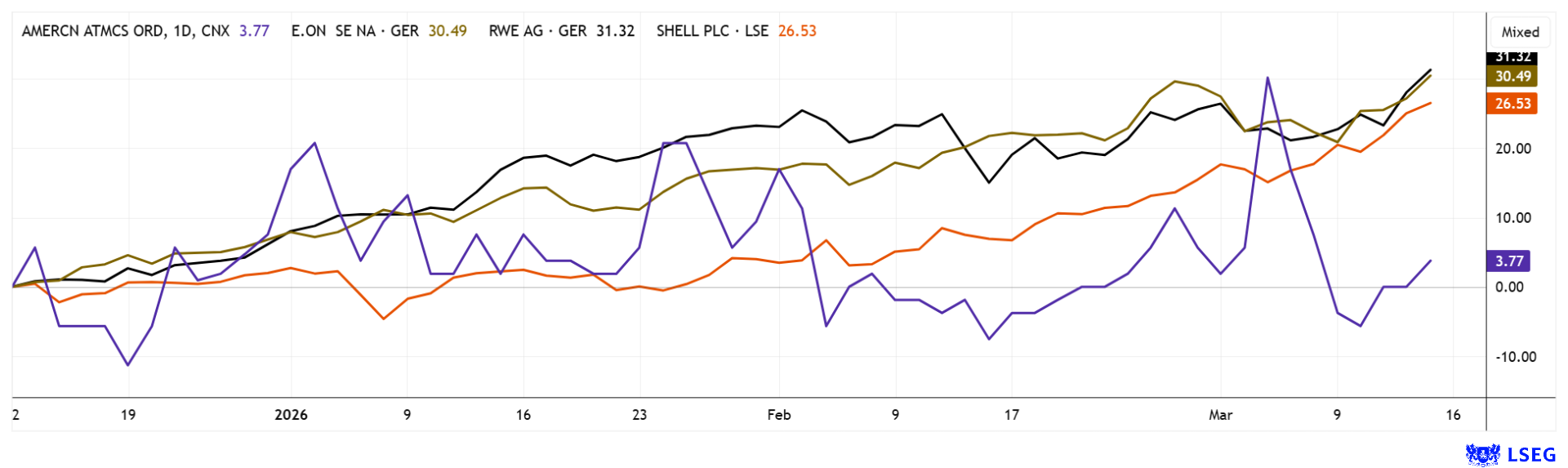

Following the conclusion of the agreement, the company is now working on permits for an initial drilling program, which is scheduled to begin in the coming months. In parallel, management is pursuing a technological approach that goes beyond mere raw material extraction. In collaboration with industry partners, the development of modular processing plants is being explored that could efficiently convert uranium ore into high-purity compounds. A particular focus is on the potential production of HALEU fuel, which is required for the next generation of small modular reactors. A strategy that is attracting growing investor attention. The shares are traded under the ticker symbol NUKE in Germany and Canada, but are also listed on the OTCQB Venture Market under the ticker symbol GNEMF. In early March, nearly CAD 2 million was raised via a private placement. For those seeking leverage in the sector, American Atomics is currently valued at just CAD 14 million and is actively traded. The prospects for a significant appreciation are exceptionally good.

Co-founder Connor Lynch presented American Atomics' strategic direction at the 18th International Investment Forum.

E.ON and RWE: Quietly Emerging as DAX Outperformers

There is significant pressure in the EU to build the necessary grids and a secure supply infrastructure. In Germany, companies and households must do without affordable nuclear power, while in other European countries, this very "NetZero" energy form is now making a remarkable comeback. Once new capacity is in place, Germany’s energy-intensive industries could again benefit from reliable baseload power. Largely unnoticed, E.ON and RWE have crept into the ranks of DAX outperformers over the past 12 months, with gains of 52% and 77%, respectively. In this environment, E.ON benefits in particular from its stable, regulated grid business, which delivers inflation-proof returns and benefits from the massive expansion of power grids in the wake of the energy transition. The focus is on electrification, grid digitalization, and smart consumption solutions for both households and industry. RWE, in turn, has positioned itself as one of Europe's leading producers of green energy and is consistently expanding its wind, solar, and storage facilities. RWE's profitability depends heavily on revenue from renewable generation capacities as well as prevailing electricity price levels. While E.ON impresses as an infrastructure stock with stable cash flows, RWE scores points with growth potential driven by the massive expansion of renewable alternatives. In terms of valuation, these models are reflected in different multiples - E.ON, with a 2026 P/E ratio of 18, is classically valued based on stable earnings, while RWE, as a growth story, receives a small premium with a P/E ratio of 23. However, both benefit structurally from the European energy transition and remain key players in the shift toward a carbon-neutral electricity system. Given the supply concerns surrounding the Middle East conflict, these stocks are a true asset to any portfolio.

Shell: Profits Keep Pouring In

Driven by robust cash flow, the shares of Shell have recently rallied significantly following a weaker 2024 and reached a new all-time high of EUR 39.19 last week. Short-term catalysts remain the 50% increase in oil and gas prices, the substantial margins in the LNG business, and potential further share buyback programs, following Shell's achievement of over USD 40 billion in operating cash flow again in 2025. Added to this are several strategic shifts, as Shell is now refocusing more strongly on fossil fuel projects and LNG as a transition fuel, while scaling back certain renewable energy commitments. What slows down ESG investors supports profitability. For the coming months, the opportunities for investors lie primarily in continued high dividends, buybacks, and a potential revaluation relative to US majors. In the medium term, regulatory pressure in the wake of the energy transition, as well as potential requirements for higher decarbonization investments, could increase or reduce the return on equity. Currently, the dividend yield is just under 3%, and analysts on the LSEG platform expect a 2026 P/E ratio of 13. A decline in oil prices could trigger a period of consolidation.

The energy markets are currently divided. While fossil fuel companies like Shell are riding the crest of the inflation wave, E.ON and RWE can benefit from Europe's infrastructure dilemma regarding electricity and gas supply. The EU faces a monumental challenge if it wants to avoid relying on its own fossil reserves. American Atomics is keeping an eye on the North American trend toward nuclear energy and could offer a complete supply chain in just a few years.

Conflict of interest

Pursuant to §85 of the German Securities Trading Act (WpHG), we point out that Apaton Finance GmbH as well as partners, authors or employees of Apaton Finance GmbH (hereinafter referred to as "Relevant Persons") currently hold or hold shares or other financial instruments of the aforementioned companies and speculate on their price developments. In this respect, they intend to sell or acquire shares or other financial instruments of the companies (hereinafter each referred to as a "Transaction"). Transactions may thereby influence the respective price of the shares or other financial instruments of the Company.

In this respect, there is a concrete conflict of interest in the reporting on the companies.

In addition, Apaton Finance GmbH is active in the context of the preparation and publication of the reporting in paid contractual relationships.

For this reason, there is also a concrete conflict of interest.

The above information on existing conflicts of interest applies to all types and forms of publication used by Apaton Finance GmbH for publications on companies.

Risk notice

Apaton Finance GmbH offers editors, agencies and companies the opportunity to publish commentaries, interviews, summaries, news and the like on news.financial. These contents are exclusively for the information of the readers and do not represent any call to action or recommendations, neither explicitly nor implicitly they are to be understood as an assurance of possible price developments. The contents do not replace individual expert investment advice and do not constitute an offer to sell the discussed share(s) or other financial instruments, nor an invitation to buy or sell such.

The content is expressly not a financial analysis, but a journalistic or advertising text. Readers or users who make investment decisions or carry out transactions on the basis of the information provided here do so entirely at their own risk. No contractual relationship is established between Apaton Finance GmbH and its readers or the users of its offers, as our information only refers to the company and not to the investment decision of the reader or user.

The acquisition of financial instruments involves high risks, which can lead to the total loss of the invested capital. The information published by Apaton Finance GmbH and its authors is based on careful research. Nevertheless, no liability is assumed for financial losses or a content-related guarantee for the topicality, correctness, appropriateness and completeness of the content provided here. Please also note our Terms of use.