March 5th, 2026 | 07:25 CET

Gold in the ground, cash on the way: Why Desert Gold is well positioned for the gold boom fueled by the Iran war

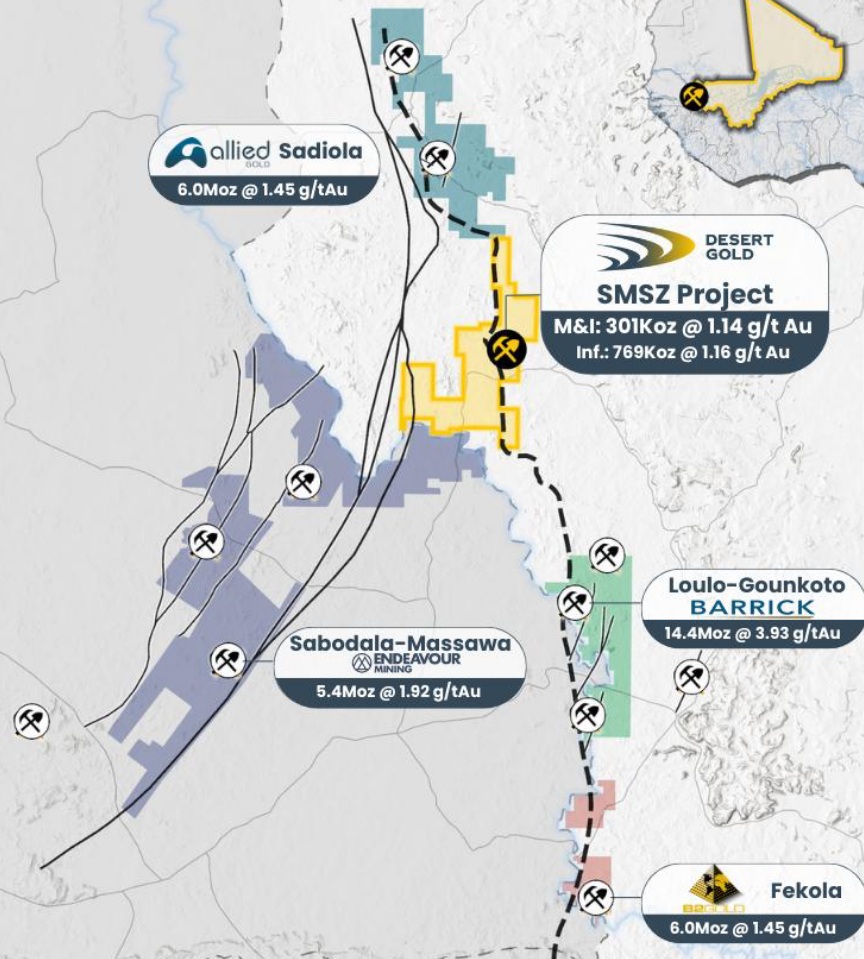

When major industry players start writing billion-dollar checks to buy their way into a region, investors should take a closer look. The acquisition of Canadian producer Allied Gold by Chinese giant Zijin Mining for CAD 5.5 billion caused a stir in West Africa at the beginning of the year. But above all, it is a wake-up call for anyone still searching for the gems that the market has overlooked. In the immediate vicinity of the acquired Allied Gold concessions, in the same highly productive Senegal-Mali Shear Zone (SMSZ), lies Desert Gold with a market capitalization of around CAD 35 million. The company owns an impressive 440 sq km of exploration ground within the same highly productive structural corridor that hosts operations owned by Barrick, B2Gold, and Endeavour. Geologically, this is the Champions League. From a valuation standpoint, however, Desert Gold plays in a completely different league. This discrepancy between geological setting and market capitalization forms the core of the investment thesis.

time to read: 4 minutes

|

Author:

Armin Schulz

ISIN:

DESERT GOLD VENTURES INC | CA25039N4084 | TSXV: DAU , OTCQB: DAUGF

Table of contents:

Author

Armin Schulz

Born in Mönchengladbach, he studied business administration in the Netherlands. In the course of his studies he came into contact with the stock exchange for the first time. He has more than 25 years of experience in stock market business.

Tag cloud

Shares cloud

An asset that can do more than the share price shows

The heart of Desert Gold is the SMSZ project in western Mali. Since 2012, the company has built up an impressive portfolio of properties here. Since then, over 1.2 million ounces of gold have been found in the "indicated" and "inferred" categories. But the sheer number of ounces is not the decisive factor. The context is much more important.

The company controls a whopping 38 km strike length along the Senegal-Mali Shear Zone. Anyone familiar with the region knows that this structure is home to the very largest mines. Barrick Mining's Loulo-Gounkoto has 15 million ounces. B2Gold's Fekola has over 6 million ounces. They are all direct neighbors of Desert Gold. This is no coincidence; it is geology. The structure does not stop at the claim boundary.

What now sets the company apart from the mass of pure exploration companies is its move toward production. In January, a final, approved Preliminary Economic Assessment (PEA) for the Barani East project was released, and the figures are compelling even at current gold prices above USD 4,000. At a gold price of USD 4,070 per ounce, the study outlines an after-tax net present value (NPV) of USD 124 million and an internal rate of return (IRR) of an exceptional 101%. The payback period is just over 2 years. Currently, the gold price is over USD 1,000 higher.

This is not a coincidence. The strategy is deliberate and structured around a modular development approach. The initial phase, a small, cost-effective gravity plant, is used to generate cash flow quickly. Construction work is expected to be so far advanced in the first half of 2025 that the first gold production will become a reality this year. CEO Jared Scharf has outlined a six-month timeline for the completion of the facilities. Cash flow from production is intended to fund further exploration activities internally, thereby reducing or potentially eliminating the need for dilutive capital increases.

The second lever: Where no one has drilled yet

While Mali is expected to provide short-term cash flow, the real price driver is waiting in the wings in Côte d'Ivoire: the Tiegba Gold project. What is so special about it? A huge ground anomaly identified by Newmont's predecessor Newcrest, but never drilled. It extends over 4 km in length and 2 km in width. Initial field surveys confirm that the gold is in situ, meaning in the bedrock.

The first core drilling is scheduled to take place here in the first half of the year. This is the moment speculative investors have been waiting for. If a contiguous gold system can be proven to exist beneath this anomaly, it would be a classic "company maker." A new discovery in this terrain would immediately attract attention due to the constant demand for new feed from the surrounding mines.

The valuation gap: USD 29 vs USD 73

Let's get to the heart of the argument. The market currently values Desert Gold at less than USD 29 per ounce of gold in the ground. That is extremely cheap. A look at acquisitions in the same geological environment since 2012 paints a completely different picture. The cheapest deals were at USD 36 per ounce, the most expensive at USD 132. The average price paid by buyers such as Barrick or Endeavour for ounces in this region is around USD 73.

To reach this average, Desert Gold's share price would have to rise significantly. Of course, this is a simplified calculation, but it illustrates the extent of the discrepancy. The acquisition of Allied Gold by Zijin, a direct neighbor, is further evidence that strategic buyers recognize the value of this region and are willing to pay for it.

In addition, the current PEA for the SMSZ project is based on less than 10% of the total gold resource. Over 1 million ounces are outside the current mine plan. Every successful drill hole that brings these ounces into the economically mineable zone increases the value of the company without the costs increasing to the same extent. This is the leverage that many overlook.

Management with substance

One aspect that is often underestimated in exploration companies is management. At Desert Gold, the board of directors and supervisory board themselves hold a stake of around 10%. If you add in the inner circle, the figure is as high as 45%. That is a strong signal. In addition, there are high-profile anchor investors such as the Merk Investments fund from California (approximately 7%) and mining legend Ross Beaty (approximately 3%). The team's operational experience in West Africa, including at Barrick and Centamin, cannot be overestimated in a region where community work and approval procedures can determine success or failure.

Analyst opinion

GBC AG recommends buying Desert Gold shares and sees an ambitious price target of CAD 0.81 by the end of 2026. GBC highlights the strong economics with an internal rate of return of 101%, the fast payback period, and the exploration potential. The stock is currently available at a significant discount for risk-tolerant investors in the gold supercycle. The company is currently trading at CAD 0.13.

Desert Gold currently offers investors a rare combination. On the one hand, it has a clear, structured path to small but capital-efficient production in Mali, which is expected to catapult the company into producer status this year. This creates a solid foundation and reduces risk. On the other hand, Tiegba in Côte d'Ivoire is a genuine "blue sky" option in the portfolio. A large, undrilled anomaly that, if successful, has the potential to be a real price driver. Surrounded by the industry's big players, with a management team that is heavily invested itself and a valuation that is well below what strategic buyers in the region are willing to pay, the risk-reward ratio here is exceptional. The market has not yet fully understood the potential of this double lever, and that is precisely the opportunity.

Conflict of interest

Pursuant to §85 of the German Securities Trading Act (WpHG), we point out that Apaton Finance GmbH as well as partners, authors or employees of Apaton Finance GmbH (hereinafter referred to as "Relevant Persons") currently hold or hold shares or other financial instruments of the aforementioned companies and speculate on their price developments. In this respect, they intend to sell or acquire shares or other financial instruments of the companies (hereinafter each referred to as a "Transaction"). Transactions may thereby influence the respective price of the shares or other financial instruments of the Company.

In this respect, there is a concrete conflict of interest in the reporting on the companies.

In addition, Apaton Finance GmbH is active in the context of the preparation and publication of the reporting in paid contractual relationships.

For this reason, there is also a concrete conflict of interest.

The above information on existing conflicts of interest applies to all types and forms of publication used by Apaton Finance GmbH for publications on companies.

Risk notice

Apaton Finance GmbH offers editors, agencies and companies the opportunity to publish commentaries, interviews, summaries, news and the like on news.financial. These contents are exclusively for the information of the readers and do not represent any call to action or recommendations, neither explicitly nor implicitly they are to be understood as an assurance of possible price developments. The contents do not replace individual expert investment advice and do not constitute an offer to sell the discussed share(s) or other financial instruments, nor an invitation to buy or sell such.

The content is expressly not a financial analysis, but a journalistic or advertising text. Readers or users who make investment decisions or carry out transactions on the basis of the information provided here do so entirely at their own risk. No contractual relationship is established between Apaton Finance GmbH and its readers or the users of its offers, as our information only refers to the company and not to the investment decision of the reader or user.

The acquisition of financial instruments involves high risks, which can lead to the total loss of the invested capital. The information published by Apaton Finance GmbH and its authors is based on careful research. Nevertheless, no liability is assumed for financial losses or a content-related guarantee for the topicality, correctness, appropriateness and completeness of the content provided here. Please also note our Terms of use.