May 5th, 2026 | 07:45 CEST

Things are heating up in the Middle East! Antimony Resources, Rheinmetall, RENK, and LPKF Laser in high demand

Created and published on behalf of Antimony Resources Corp.

The escalating conflict in the Middle East is acting as a catalyst for the already fragile global supply chains and is abruptly pushing critical raw materials into the spotlight of the capital markets. The focus is less on the physical flow of metals through the Strait of Hormuz and more on its role as a bottleneck for approximately 20% of global oil trade, where disruptions immediately drive up energy prices and, consequently, the cost base of industrial production. Even moderate disruptions lead to rising freight rates, higher insurance premiums, and extended delivery times: a toxic mix for industries optimized for just-in-time production. Studies estimate that the risk of a sustained disruption could destabilize trade volumes of up to USD 1.2 trillion annually. In this complex situation, companies that address strategic bottlenecks or are part of the security-relevant value chain stand to benefit the most. Antimony Resources Corp. is emerging as a potential Western supplier of a critical metal, while Rheinmetall and RENK Group are benefiting from rising defence budgets. LPKF Laser & Electronics is addressing the chip market with new ideas. Investors should trust their instincts about what belongs in their portfolio right now.

time to read: 5 minutes

|

Author:

André Will-Laudien

ISIN:

ANTIMONY RESOURCES CORP | CA0369271014 | CSE: ATMY , OTCQB: ATMYF , RHEINMETALL AG | DE0007030009 , RENK AG O.N. | DE000RENK730 , LPKF LASER+ELECTRON. | DE0006450000

Table of contents:

Author

André Will-Laudien

Born in Munich, he first studied economics and graduated in business administration at the Ludwig-Maximilians-University in 1995. As he was involved with the stock market at a very early stage, he now has more than 30 years of experience in the capital markets.

Tag cloud

Shares cloud

Critical Raw Material, Critical Moment: Antimony Between Geopolitics and Valuation Speculation

The strategic relevance of the specialty metal antimony has intensified dramatically in a short period of time, driven by geopolitical tensions and a structural supply shortage. China controls around 70% of global production, while prices have risen from about USD 15,000 to over USD 60,000 per ton—a classic setup for Western supply risks. In this environment, Antimony Resources Corp. is increasingly coming into focus, as the company's Canadian portfolio represents a rare and, at the same time, North American option. The Bald Hill project forms the foundation with a target size of approximately 2.7 million tonnes at 3 to 4% antimony content, which implies a substantial metal inventory. New soil samples have now been analyzed, more than 550 in total, and they provide additional momentum. Values exceeding 450 ppm were detected in various zones, more than 40 times the normal background level. Such anomalies are not limited to specific points but remain open and extend across multiple target areas, increasing the likelihood of a significantly larger system.

The clear signature is striking: antimony occurs largely without correlation to classic associated metals, suggesting independent mineralized structures. Geophysical interpretations link these zones to fault structures, which often act as conduits for mineralizing fluids. Furthermore, existing zones already exhibit considerable dimensions: over 600 m in strike length and up to 350 m in depth, with average thicknesses of 4 to 5 m. That is impressive!

Crucial to Antimony Resources' investment case is the military demand component, which accounts for about one-third of the thesis: Antimony is used in armour-piercing ammunition, hardened alloys, and flame-retardant systems for military platforms. Added to this are applications in batteries and electronics for drones, communication systems, and modern combat operations. With rising defence budgets in Europe and North America, demand is shifting structurally upward, while supply remains severely limited.

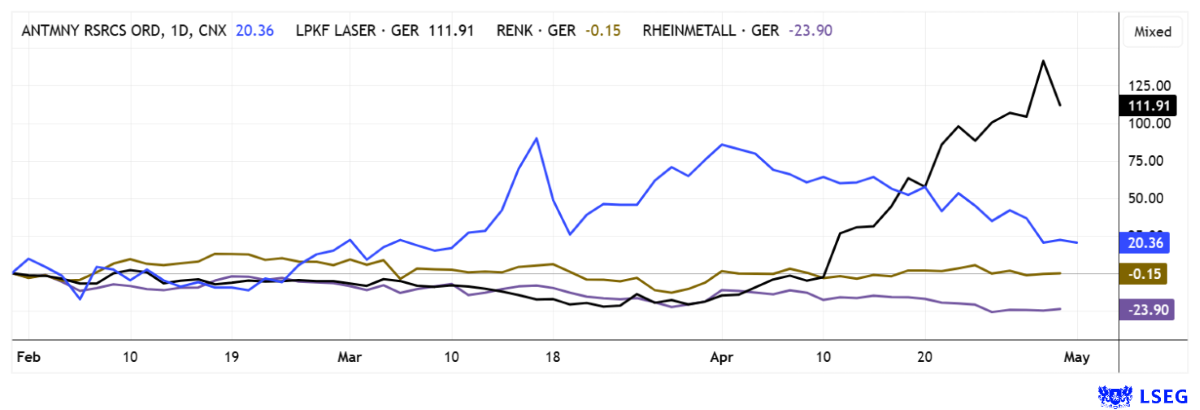

The capital markets have so far only cautiously priced in this situation. Although the stock has risen significantly in just a few months, the valuation remains moderate at around CAD 95 million compared to the potential metal value. In the short term, an initial NI 43-101 resource estimate is likely to act as a catalyst, while additional drilling programs and an expanded exploration area could provide further upside. GBC Research expects CAD 3.00 in 12 months; currently, one can still get in at CAD 1.00.

CEO James R. Atkinson in an interview with IIF host Lyndsay Malchuk on current developments.

RENK and Rheinmetall – Analysts Positive Again After the Correction

In addition to the traditional supply chain companies in the metals sector, their customers—the defence industry—have naturally shone over the past three years. Stocks like RENK managed to more than quadruple during this period, while the blockbuster Rheinmetall rose from around EUR 100 to a peak of EUR 2,005—a 20-fold increase. That was likely too big a bite to take, as the stock then fell by 35% to around EUR 1,300. RENK also saw a nearly 50% drop from EUR 90 to 47. At the Munich Capital Markets Conference in mid-April, attendees learned that RENK now generates over 75% of its consolidated revenue in the defence sector. With an order backlog of EUR 6.7 billion, the 2025 revenue of EUR 1.366 billion is likely to be comfortably surpassed. Analysts on the LSEG platform estimate revenue increases for 2026/27 to EUR 1.559 billion and EUR 1.814 billion, respectively—a 20% annual increase in each case.

Things also continue to look good at Rheinmetall. CEO Armin Papperger expects revenue to reach around EUR 50 billion by 2030; here, experts are still somewhat more cautious, with a consensus estimate of EUR 42.8 billion. The price targets are particularly interesting. **For RENK, 15 out of 17 research firms are positive and expect an average 12-month price target of EUR 69.50, about 30% above yesterday's level. However, analysts are almost euphoric about Rheinmetall. 19 out of 24 "Buy" recommendations set a target price of EUR 2,056—47% above yesterday's closing price of EUR 1,395. Wow—let's see if that holds up!

LPKF Laser – Investors see great potential for the chip industry

How insiders move stock prices. A few weeks ago, no one had much good to say about LPKF Laser. Then a board member bought at EUR 5.95, triggering a buying spree that lifted the price to over EUR 20 by yesterday. As a result, LPKF Laser's stock has evolved from a small-cap stock to a momentum star within weeks. However, the rally stands in stark contrast to the company's operational performance. In 2025, revenue fell by 6%, EBIT stood at just EUR 0.8 million, and the net loss widened to EUR 14.3 million, while order intake dropped to EUR 27 million.

The current driver of the share price, however, is LIDE technology. It addresses a central problem in the semiconductor industry: excessive heat generation. Traditional substrates reach thermal limits when used in AI chips, while glass is considered an alternative but has been difficult to process until now. This is precisely where LPKF comes in: enabling high-precision microstructures in glass that could be crucial for the next generation of chips. Collaborations with industry partners on a pilot line through Q3 2026 underscore the potential, though they have yet to contribute to revenue. So far, so good!

However, warning signs are mounting regarding the stock price: analyst targets around EUR 9.50 are roughly half the current price, and technical indicators also point to a clearly overbought situation. Strategically, however, the case remains compelling, as precision lasers play a key role in high-tech and defence applications. Should LIDE gain traction starting in 2027, a significant scaling effect in revenue and margins is on the horizon. Until then, LPKF remains a speculative tech stock with plenty of ups and downs—a trader's dream!

Not an easy time for investors. Even though we read mostly bad news about global economies every day, stock prices are still soaring. According to expert studies, the so-called Shiller P/E ratio for the S&P 500 currently stands at 41, whereas the long-term average is closer to 16-18. Of course, bulls argue that technology stocks in particular deserve a high P/E ratio. Whether this is truly sustainable in the face of external global shocks remains questionable. Investors are therefore well advised to conduct thorough research before making long-term commitments.

Conflict of interest

Pursuant to §85 of the German Securities Trading Act (WpHG), we point out that Apaton Finance GmbH as well as partners, authors or employees of Apaton Finance GmbH (hereinafter referred to as "Relevant Persons") currently hold or hold shares or other financial instruments of the aforementioned companies and speculate on their price developments. In this respect, they intend to sell or acquire shares or other financial instruments of the companies (hereinafter each referred to as a "Transaction"). Transactions may thereby influence the respective price of the shares or other financial instruments of the Company.

In this respect, there is a concrete conflict of interest in the reporting on the companies.

In addition, Apaton Finance GmbH is active in the context of the preparation and publication of the reporting in paid contractual relationships.

For this reason, there is also a concrete conflict of interest.

The above information on existing conflicts of interest applies to all types and forms of publication used by Apaton Finance GmbH for publications on companies.

Risk notice

Apaton Finance GmbH offers editors, agencies and companies the opportunity to publish commentaries, interviews, summaries, news and the like on news.financial. These contents are exclusively for the information of the readers and do not represent any call to action or recommendations, neither explicitly nor implicitly they are to be understood as an assurance of possible price developments. The contents do not replace individual expert investment advice and do not constitute an offer to sell the discussed share(s) or other financial instruments, nor an invitation to buy or sell such.

The content is expressly not a financial analysis, but a journalistic or advertising text. Readers or users who make investment decisions or carry out transactions on the basis of the information provided here do so entirely at their own risk. No contractual relationship is established between Apaton Finance GmbH and its readers or the users of its offers, as our information only refers to the company and not to the investment decision of the reader or user.

The acquisition of financial instruments involves high risks, which can lead to the total loss of the invested capital. The information published by Apaton Finance GmbH and its authors is based on careful research. Nevertheless, no liability is assumed for financial losses or a content-related guarantee for the topicality, correctness, appropriateness and completeness of the content provided here. Please also note our Terms of use.