May 8th, 2026 | 07:30 CEST

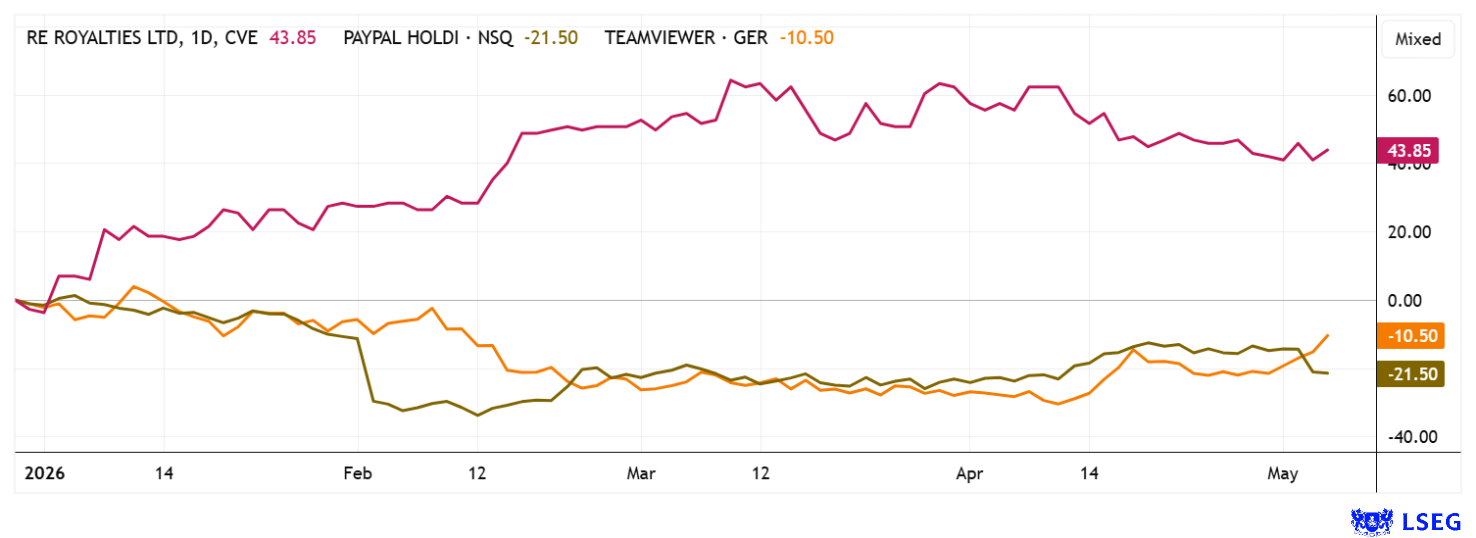

One-Two-Three: High-Momentum Stocks in Focus! TeamViewer, RE Royalties, and PayPal Are Taking Off

The situation in the Middle East is now calming down—or is it? Despite lingering doubts, the indices have already started moving higher. Some stocks have even capitalized on the volatile environment, sending their charts soaring on the back of improved outlooks, while others continue to suffer from the uncertainty. Defence, security, and military stocks, in particular, are losing steam in this environment, having profited from the turmoil for months. The markets breathed a noticeable sigh of relief yesterday, but any new report from the region could turn sentiment on its head within minutes. From an economic perspective, this is likely not the end of the crisis for investors, but rather a temporary interlude full of opportunities and risks. Those who look closely now can profit in areas where no one has really wanted to be for months.

time to read: 5 minutes

|

Author:

André Will-Laudien

ISIN:

TEAMVIEWER AG INH O.N. | DE000A2YN900 , RE ROYALTIES LTD | CA75527Q1081 | TSXV: RE , OTCQX: RROYF , PAYPAL HDGS INC.DL-_0001 | US70450Y1038

Table of contents:

Author

André Will-Laudien

Born in Munich, he first studied economics and graduated in business administration at the Ludwig-Maximilians-University in 1995. As he was involved with the stock market at a very early stage, he now has more than 30 years of experience in the capital markets.

Tag cloud

Shares cloud

Dividends, Diversification, Deal Options: RE Royalties Quietly Builds a Green Finance Platform

If a survey were conducted in Germany asking what people envision when they think of the energy transition, one would likely hear 1,000 different perspectives. The Canadian specialty financier RE Royalties is taking an interesting approach by providing a key building block: innovative financing for green energy projects. The Canadian company is increasingly establishing itself as a kind of renewable energy licensor, combining elements of traditional infrastructure financing with modern ESG principles. Instead of operating wind or solar plants itself, RE Royalties participates in the projects' revenues through revenue-based compensation models, thereby creating an inflation-resistant cash flow profile. This model is reminiscent of streaming approaches from the commodities sector or long-term YieldCo structures, albeit with significantly lower operational complexity.

Particularly exciting is the company's current strategic realignment, as after more than a decade of growth, management is now exploring partnerships, capital measures, or even a full transaction to unlock hidden reserves. Such processes are often viewed in the capital markets as a precursor to a revaluation, especially when stable cash flows and scalable business models converge. At the same time, the company is further expanding its position in the US solar market and recently invested additional funds in a broadly diversified portfolio with projects across multiple states. In total, RE Royalties now controls more than 100 investments in solar, wind, hydropower, and battery storage, giving it a remarkably diversified platform.

The recurring revenues increasingly resemble the coupons of sustainable infrastructure bonds, albeit with additional growth potential driven by rising electricity prices and the massive expansion of AI data centers and electric mobility. The continuity of distributions is also noteworthy, as solid dividends have been paid over many quarters—a rare hallmark of quality in the volatile cleantech sector. Should global capital demand for green infrastructure continue to accelerate as expected, royalty models in the ESG sector could attain the same strategic importance in the future as licensing fees in the software industry or streaming contracts in mining. The stock is up over 40% in 2026. But following the current consolidation, it offers solid entry prices! Electrifying!

COO Peter Leighton will explain his strategy for the current year at the 19th International Investment Forum. Click here to register.

TeamViewer – Between Cost-Cutting and Growth Doubts

The sell-off correction for remote software expert TeamViewer reached as low as EUR 4.11. First-quarter figures were released in recent days. Analysts are divided, but investors are gradually returning. Currently, the Göppingen-based company is navigating a remarkable balancing act between operational discipline and slowing growth momentum. Although revenue shrank slightly again in Q1 to around EUR 183 million, the efficiency program launched in 2024 is now visibly taking effect behind the scenes. Particularly striking is the significant jump in profitability and operating income, even though demand in key regions such as North and South America lost noticeable momentum. The adjusted EBITDA margin climbed to a robust 45%, signalling that the software group has significantly streamlined its cost base. Above all, the massive reduction in marketing expenses acted as a turbocharger for the margin, ensuring that EBIT and net profit could grow by double digits despite weaker revenues.

At the same time, however, a sensitive aspect of the business model is becoming apparent. The number of smaller corporate customers continues to decline; customer loyalty in the enterprise segment appears to be waning, and even existing customers are being more cautious with their budgets. From a regional perspective, Europe remains the group's anchor of stability, while the Americas and Asia are currently acting more like brakes. Nevertheless, management remains steadfast in its annual forecast and is counting on a recovery in the second half of the year. On the stock market, this mix of cost discipline and confidence was initially met with euphoria, and the stock market responded with a double-digit price jump. Behind the short-term relief, however, the central question remains: whether TeamViewer can return to organic growth in the future, or whether the rising profits stem primarily from cost-cutting measures and financial fine-tuning. Analysts on the LSEG Refinitiv platform generally agree on a fair value of around EUR 9, though Deutsche Bank puts it at a low EUR 6.50 and DZ Bank remains rather cautious at EUR 7.00.

PayPal – New Leadership, New Momentum

Finally! At payment service provider PayPal, a phase of radical restructuring is beginning under new CEO Enrique Lores, after the company lost much of its market lustre. A cost-cutting program worth billions is intended to squeeze out high costs from the system and eliminate inefficient, duplicative structures in the coming years. At the same time, management is attempting to strategically realign the company for the modern era. The aim is to focus more strongly on high-margin core businesses. Operationally, PayPal has recently proven more resilient than many market participants had expected. Despite all market doubts, payment volume grew by double digits, and the company also delivered a positive surprise on the earnings front. Nevertheless, investors reacted skeptically to the announced major restructuring, and the stock lost significant ground again following the Q1 results. Apparently, concerns are growing in the market that the company can no longer keep pace technologically with modern fintech platforms and digital wallet providers. This is precisely where CEO Lores is now stepping in, aiming to both modernize the technical infrastructure and integrate artificial intelligence more deeply into internal processes. The coming quarters are therefore likely to be a decisive test. Meanwhile, the estimated 2026 P/E ratio has even fallen to a low of 8.7, despite an annual free cash flow of over USD 6 billion. The stock is a bargain!

In the current environment, investors should focus more on long-term expectations for stocks rather than betting on short-term price fluctuations. This is because, first, daily volatility causes extreme swings that are completely irrelevant, and second, a surprising resolution to one of the numerous geopolitical conflicts could quickly trigger a rally, which, in the age of algorithmic and AI trading, can unfold within minutes.

Conflict of interest

Pursuant to §85 of the German Securities Trading Act (WpHG), we point out that Apaton Finance GmbH as well as partners, authors or employees of Apaton Finance GmbH (hereinafter referred to as "Relevant Persons") may hold shares or other financial instruments of the aforementioned companies in the future or may bet on rising or falling prices and thus a conflict of interest may arise in the future. The Relevant Persons reserve the right to buy or sell shares or other financial instruments of the Company at any time (hereinafter each a "Transaction"). Transactions may, under certain circumstances, influence the respective price of the shares or other financial instruments of the Company.

In addition, Apaton Finance GmbH is active in the context of the preparation and publication of the reporting in paid contractual relationships.

For this reason, there is a concrete conflict of interest.

The above information on existing conflicts of interest applies to all types and forms of publication used by Apaton Finance GmbH for publications on companies.

Risk notice

Apaton Finance GmbH offers editors, agencies and companies the opportunity to publish commentaries, interviews, summaries, news and the like on news.financial. These contents are exclusively for the information of the readers and do not represent any call to action or recommendations, neither explicitly nor implicitly they are to be understood as an assurance of possible price developments. The contents do not replace individual expert investment advice and do not constitute an offer to sell the discussed share(s) or other financial instruments, nor an invitation to buy or sell such.

The content is expressly not a financial analysis, but a journalistic or advertising text. Readers or users who make investment decisions or carry out transactions on the basis of the information provided here do so entirely at their own risk. No contractual relationship is established between Apaton Finance GmbH and its readers or the users of its offers, as our information only refers to the company and not to the investment decision of the reader or user.

The acquisition of financial instruments involves high risks, which can lead to the total loss of the invested capital. The information published by Apaton Finance GmbH and its authors is based on careful research. Nevertheless, no liability is assumed for financial losses or a content-related guarantee for the topicality, correctness, appropriateness and completeness of the content provided here. Please also note our Terms of use.