April 7th, 2026 | 07:35 CEST

Fertilizer Crisis: Supply Chain Collapse Threatens Bayer, Nestlé, MustGrow, and K+S! Where are the Opportunities for Investors?

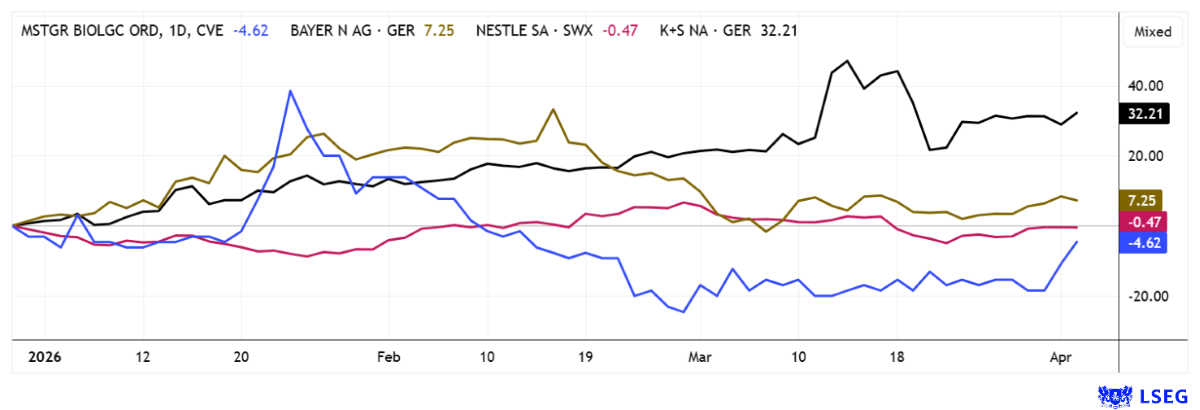

The escalation involving Iran has thrown global supply chains and the fertilizer and food sectors into a state of emergency, as sanctions and security risks are crippling exports of key raw materials. Iran, a key producer of phosphate-based fertilizers and potash products, is temporarily out of the picture, leading to price spikes of up to 40% in the agricultural sector. Bayer is struggling with rising production costs for its agrochemicals division, which is putting extreme pressure on margins. Even Nestlé is increasingly facing raw material shortages for animal feed and packaging materials. The situation regarding supply security in Europe is at risk in the medium term, as inflationary pressure on food prices is noticeably increasing. MustGrow is positioning itself as a game-changer with organic fertilizer alternatives that are scalable regardless of geopolitical hotspots and promise rapid revenue growth. Kali + Salz is benefiting massively from the demand for potash fertilizer, as European inventories shrink and demand from agriculture explodes.

time to read: 6 minutes

|

Author:

André Will-Laudien

ISIN:

BAYER AG NA O.N. | DE000BAY0017 , NESTLE NAM. SF-_10 | CH0038863350 , MUSTGROW BIOLOGICS CORP | CA62822A1030 | TSXV: MGRO , OTCQB: MGROF , K+S AG NA O.N. | DE000KSAG888

Table of contents:

Author

André Will-Laudien

Born in Munich, he first studied economics and graduated in business administration at the Ludwig-Maximilians-University in 1995. As he was involved with the stock market at a very early stage, he now has more than 30 years of experience in the capital markets.

Tag cloud

Shares cloud

Bayer and Nestlé – Facing the Impact of Global Shortages

The global trade distortions caused by the Middle East crisis have not yet reached supermarket shelves. However, upstream production stages in the food sector are currently grappling with significant cost increases, including fossil fuels up 40%, organic raw materials up 25%, and critical metals for production processes up 20%. It is only a matter of time before consumers have to bear these noticeable price hikes.

The diversified conglomerates Bayer and Nestlé are primarily feeling the impact of higher energy, raw material, and transportation costs, which are affecting their operating cost base. This is particularly relevant for Bayer, as energy-intensive processes in agricultural chemicals are sensitive to price fluctuations in gas and feedstocks. In the agricultural sector, a prolonged rise in energy and raw material costs can put margins under significant pressure, especially since energy often accounts for 30 to 40% of production costs. Strategically, the risk therefore lies less in immediate supply disruptions than in rising manufacturing costs and higher working capital. At Nestlé, the impact is most evident in logistics: rerouting of freight routes can extend transit times between Europe and Asia by 10 to 15 days, thereby dramatically increasing freight rates and storage costs. Supply disruptions would likely occur if disruptions persist for months!

For investors, the current situation thus primarily means increased earnings and price volatility, but not a structural supply weakness. Both companies have multi-sourcing and scalable supply chains, which enable pricing power, thereby strengthening their resilience to regional disruptions. The decisive factors remain how long the geopolitical uncertainty persists and to what extent cost increases can be passed on to customers. Analysts on the LSEG Refinitiv platform have not yet priced in the current external factors. Accordingly, the weighted 12-month price target for Bayer stands at EUR 44.84 (+14%), while Nestlé's is at EUR 85.67 (+9.5%). As a precaution in light of potential further global bottlenecks, both stocks currently appear more like sell positions.

MustGrow – A Game-Changer in the Field of Biological Fertilizer Alternatives

In the right place at the right time. At a time when potash fertilizer is trading like gold, some farmers are having to switch to cheaper alternatives. The Canadian agricultural biotech firm MustGrow Biologics Corp. is positioning itself precisely in this market, which is structurally shifting toward sustainable and organic solutions. This is driven by a global trend: increasing regulatory requirements, a growing need for healthy soils, and an agricultural sector that must simultaneously deliver higher yields and meet environmental standards. At the same time, major agricultural corporations are increasingly investing in biological technologies, as these are achieving growth rates of around 10 to 20% per year and are thus expanding significantly faster than traditional chemical pesticides. Experts estimate that the global market for biological crop protection solutions could reach a volume of around USD 15 to USD 16 billion by the end of the decade, providing fertile ground for MustGrow's rapid growth.

The innovative Canadian company has launched a technology platform based on natural plant compounds that can be used both to combat soil pests and to improve soil quality. The underlying concept leverages the natural defense mechanisms of certain plants and translates them into agricultural applications with repeatable use. This has resulted in several products, including solutions to promote root growth and strengthen crops' resilience to stress factors. Of particular interest is the potential for recurring revenue in specialty crops such as fruits, vegetables, or seed production, where high margins and stable demand are typical. Organic agricultural producers today rely on a range of ESG certifications; MustGrow provides corresponding solutions.

Operationally, the company is in a phase of transition from research and development toward broader commercialization of its products. Initial sales have already been achieved in North America, with demand at times exceeding available production capacity, indicating early market access and growing interest. At the same time, management is pursuing a dual business model consisting of direct sales and licensing partnerships with established agricultural corporations, which allows for the partial outsourcing of development and regulatory approval costs. An international collaboration with a major industry player enables the company to tap into new markets and streamline regulatory processes. Technologically, MustGrow possesses an extensive patent portfolio of more than 110 intellectual property rights, which serve as a barrier to entry for competitors and can support the long-term monetization of the platform.

Particularly revealing are recent field trials involving a major North American crop, in which soil pathogens were reduced by up to 95%. Such results increase the likelihood that biological solutions will be used in the future not only as a supplement but increasingly as an integral part of modern farming systems. Financially, the company remains relatively lean, which is typical for growth-oriented small-cap companies. Following a capital raise of approximately CAD 2 million and a share count of about 63 million shares, the market valuation stands at approximately CAD 40 million. In the current environment, the company is likely to continue its recent surge unabated, as investors recognize its relevance in both the short and long term.

COO Colin Bletsky explained how the technology works at the 18th International Investment Forum.

K+S – Not Yet on the Buy List Despite Higher Earnings Estimates

The German fertilizer giant K+S is the absolute beneficiary of the current supply crunch. Some may view this as unethical; others say that is just how business works. K+S, a company over 130 years old (founded in 1889), is one of the world's leading suppliers of potash and magnesium-containing products. Now is harvest time, as the company has every reason to raise its prices. The stock market seems to agree. The onset of the Iran crisis technically fits into a strong upward trend that began back in January at around EUR 12. The price briefly surpassed EUR 18, but the subsequent technical consolidation following a 50% rise has brought it back down to around EUR 15.20 over the past two weeks.

The latest analyst ratings from UBS and Deutsche Bank were disappointing. Although the experts have slightly raised their EBITDA forecasts, global risks for the fertilizer business are likely to remain dominant through 2026. As a result, both firms maintain a "Sell" rating with price targets of EUR 11.50 and EUR 10.20, respectively. At least 8 out of 23 analysts on the LSEG Refinitiv platform have managed to issue a "Buy" recommendation. This results in a weighted 12-month consensus of EUR 14.58. Some firms will likely revisit their calculations and, due to potential price increases, also expect better profits for K+S. In our view, the temporary high of EUR 18 should therefore be quickly surpassed on the second attempt.

The global state of the markets is cause for concern. While large technology companies are most affected by supply chain disruptions, it is also becoming clear that food supply is by no means immune to such pressures. If there is a global shortage of potash fertilizer, crop yields could plummet in 2026. This should give the shares of K+S and MustGrow a new boost, as suitable solutions are already available.

Conflict of interest

Pursuant to §85 of the German Securities Trading Act (WpHG), we point out that Apaton Finance GmbH as well as partners, authors or employees of Apaton Finance GmbH (hereinafter referred to as "Relevant Persons") currently hold or hold shares or other financial instruments of the aforementioned companies and speculate on their price developments. In this respect, they intend to sell or acquire shares or other financial instruments of the companies (hereinafter each referred to as a "Transaction"). Transactions may thereby influence the respective price of the shares or other financial instruments of the Company.

In this respect, there is a concrete conflict of interest in the reporting on the companies.

In addition, Apaton Finance GmbH is active in the context of the preparation and publication of the reporting in paid contractual relationships.

For this reason, there is also a concrete conflict of interest.

The above information on existing conflicts of interest applies to all types and forms of publication used by Apaton Finance GmbH for publications on companies.

Risk notice

Apaton Finance GmbH offers editors, agencies and companies the opportunity to publish commentaries, interviews, summaries, news and the like on news.financial. These contents are exclusively for the information of the readers and do not represent any call to action or recommendations, neither explicitly nor implicitly they are to be understood as an assurance of possible price developments. The contents do not replace individual expert investment advice and do not constitute an offer to sell the discussed share(s) or other financial instruments, nor an invitation to buy or sell such.

The content is expressly not a financial analysis, but a journalistic or advertising text. Readers or users who make investment decisions or carry out transactions on the basis of the information provided here do so entirely at their own risk. No contractual relationship is established between Apaton Finance GmbH and its readers or the users of its offers, as our information only refers to the company and not to the investment decision of the reader or user.

The acquisition of financial instruments involves high risks, which can lead to the total loss of the invested capital. The information published by Apaton Finance GmbH and its authors is based on careful research. Nevertheless, no liability is assumed for financial losses or a content-related guarantee for the topicality, correctness, appropriateness and completeness of the content provided here. Please also note our Terms of use.