April 14th, 2026 | 07:35 CEST

Dream Returns with Oil and Gas! Jump on Pure One, but Proceed with Caution on BP, OMV, and Nordex

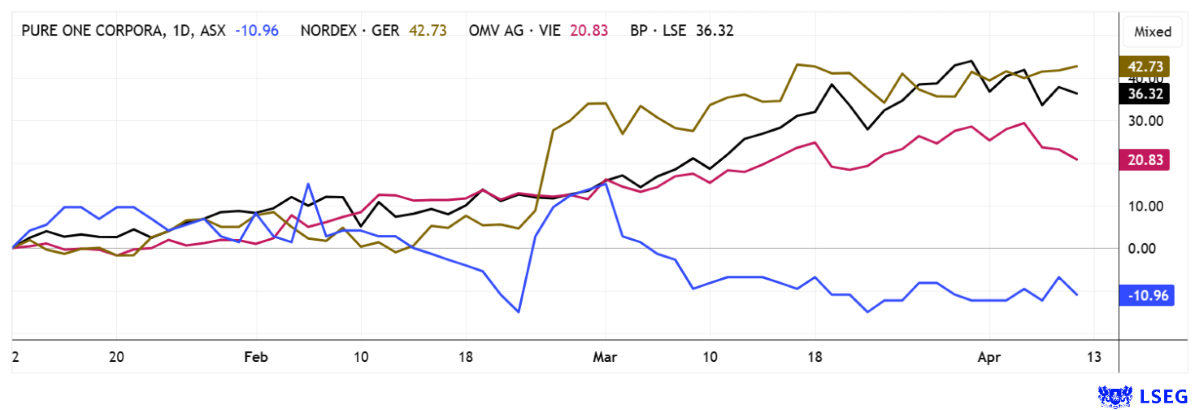

Recent developments are drawing renewed attention! US President Donald Trump has ordered the US Navy to implement a full-scale blockade of the Strait of Hormuz. He aims to halt Iranian shipments, which had previously been tolerated, in favor of countries that are no longer on the list of allies in this Middle East conflict. At the same time, a joint project by individual NATO allies is launching to secure the disputed strait, to enable future transit once again. With this news, energy and commodity prices surged higher again yesterday, even though some of the gains were already pared back by the afternoon. The focus is once again on oil and gas stocks, as well as some alternative energy and utility shares. In this environment, the Australian company Pure One can steer its diverse range of activities in the most profitable direction. Meanwhile, established players such as BP, OMV, and Nordex have already seen significant share price gains, prompting analysts to adopt a more cautious stance. A closer look is therefore warranted.

time to read: 4 minutes

|

Author:

André Will-Laudien

ISIN:

PURE ONE CORPORATION LIMITED | AU0000442865 | ASX: P1E , BP PLC DL-_25 | GB0007980591 , OMV AG ADR 1 | US6708755094 , NORDEX SE O.N. | DE000A0D6554

Table of contents:

Author

André Will-Laudien

Born in Munich, he first studied economics and graduated in business administration at the Ludwig-Maximilians-University in 1995. As he was involved with the stock market at a very early stage, he now has more than 30 years of experience in the capital markets.

Tag cloud

Shares cloud

BP and OMV – When to Take Profits?

In the current market environment, investors are torn between "staying invested" and "selling everything." This decision is particularly difficult when it comes to energy stocks like BP and OMV, as both have gained between 20% and 40% over the past six weeks. When in doubt, a look at the fundamentals often helps. According to analysts, BP is projected to see revenue growth of over 12% and a disproportionately large increase in profits in 2026. The dividend yield is expected to remain above 4%, and share buybacks are also anticipated based on historical cash flows. However, the stock is still a good 40% below its all-time high of approximately EUR 10.50. Experts on the LSEG Refinitiv platform, meanwhile, are once again more cautious. Only 12 out of 26 analysts now expect further appreciation, and the 12-month average price target is actually a full 2% below the current price. Investors should apply the trailing stop-loss method here, which involves automatically adjusting the stop price upward each day by a 5% margin. This helps secure the gains of recent weeks in the event of a potential correction without a gap—that is, without a technical price gap.

The situation is similar at OMV. Here, investors are keeping a close eye on the spin-off and IPO of the Arab chemical subsidiary. Last week, Emma Delaney of BP moved to the CEO's chair at OMV. It will be interesting to see how things develop here. OMV AG has been managed very conservatively in recent years and has offered investors a high special dividend in addition to the regular dividend. However, there have also been downgrades here in recent weeks, lowering the target price to around EUR 55.50. Yesterday, the stock was still trading above EUR 59. Tough call!

From hydrogen pioneer to multi-energy player: Is Pure One poised for a re-rating?

The current situation plays right into the hands of Australia's Pure One Corporation. The energy specialist is in a strategic transformation phase between a traditional energy investment model and a cleantech growth story. Over the past few months, the company has operated in an increasingly strained energy market, where structural gas shortages are expected to start in 2028, particularly in Australia.

Currently, natural gas, the core asset, is regaining importance as a stabilizing factor for industry and the power supply. A key value driver is therefore the stake in Eastern Gas Corporation Ltd, which was recently listed on the ASX but remains approximately 69.4% owned by Pure One. This stake represents a significant portion of the market capitalization and suggests a potential valuation discount for the company as a whole. At the same time, Pure One is pursuing a clear diversification strategy in the area of zero-emission mobility. This includes developments in battery-electric commercial vehicles, hydrogen fuel cells, and hybrid propulsion solutions. This is complemented by innovative concepts such as battery swap and leasing models for fleet customers.

The company is thus aiming to position itself as an integrated provider of sustainable transport and energy solutions. The balance sheet was strengthened by the planned sale of a stake in the Turquoise Group, freeing up capital for the strategic focus. These funds are to be reinvested specifically in the expansion of cleantech activities. On the operational side, initial international partnerships are already in place, including in Europe, the US, and South America. Industrial customers such as Heidelberg Materials are also part of the early commercial development. Due to the diversity of topics, some initiatives are well in line with current trends, while profitability is still lagging due to high investments. Overall, Pure One presents a speculative risk-reward profile with exposure to energy shortages, high equity valuations, and cleantech growth. A market capitalization of just AUD 25.5 million certainly points to significant undervaluation from a sum-of-the-parts perspective.

Nordex – The Target Margin Has Now Been Reached

Hamburg-based wind energy specialist Nordex has gained significantly following its 2025 annual results, but at the current price level of just under EUR 45, the reaction to last year's performance already seems somewhat ambitious and leaves little margin of safety. The wind turbine manufacturer delivered on the operational front, increasing revenue to EUR 7.6 billion and setting a new record with 10.2 GW in order intake, while EBITDA more than doubled to EUR 631 million. The EBITDA margin of 8.4% also marks a leap toward the medium-term target, underscoring the fundamentally strong operational performance. At the same time, the last two reports have shown that while Nordex remains in good business, the fresh impetus for a sustainable revaluation appears limited. Against this backdrop, the rather conservative price targets of EUR 34 at Deutsche Bank and EUR 40 at Bernstein seem plausible, especially since valuation expectations have cooled significantly following the recent strong run. Technically, this fits the picture, as the market is putting the stock to the test following the latest rally. This is evident in the volatile trading range between EUR 42.50 and EUR 46.50 since mid-March. For further upside potential, the company now needs more than just solid figures; it requires new operational surprises and clear evidence that the margin level can not only be achieved but also consistently maintained. Caution at the platform edge!

The energy sector is currently highly volatile. While prices surged at the onset of tensions in the Middle East, they declined again last week as the situation temporarily eased. However, as long as oil and gas prices remain elevated, companies such as BP, OMV, and Nordex continue to be in investors' favor. Investors should closely monitor momentum to protect recent gains from potential reversals. In contrast, Pure One has seen increased market activity in recent days, with the stock gaining noticeable traction.

Conflict of interest

Pursuant to §85 of the German Securities Trading Act (WpHG), we point out that Apaton Finance GmbH as well as partners, authors or employees of Apaton Finance GmbH (hereinafter referred to as "Relevant Persons") currently hold or hold shares or other financial instruments of the aforementioned companies and speculate on their price developments. In this respect, they intend to sell or acquire shares or other financial instruments of the companies (hereinafter each referred to as a "Transaction"). Transactions may thereby influence the respective price of the shares or other financial instruments of the Company.

In this respect, there is a concrete conflict of interest in the reporting on the companies.

In addition, Apaton Finance GmbH is active in the context of the preparation and publication of the reporting in paid contractual relationships.

For this reason, there is also a concrete conflict of interest.

The above information on existing conflicts of interest applies to all types and forms of publication used by Apaton Finance GmbH for publications on companies.

Risk notice

Apaton Finance GmbH offers editors, agencies and companies the opportunity to publish commentaries, interviews, summaries, news and the like on news.financial. These contents are exclusively for the information of the readers and do not represent any call to action or recommendations, neither explicitly nor implicitly they are to be understood as an assurance of possible price developments. The contents do not replace individual expert investment advice and do not constitute an offer to sell the discussed share(s) or other financial instruments, nor an invitation to buy or sell such.

The content is expressly not a financial analysis, but a journalistic or advertising text. Readers or users who make investment decisions or carry out transactions on the basis of the information provided here do so entirely at their own risk. No contractual relationship is established between Apaton Finance GmbH and its readers or the users of its offers, as our information only refers to the company and not to the investment decision of the reader or user.

The acquisition of financial instruments involves high risks, which can lead to the total loss of the invested capital. The information published by Apaton Finance GmbH and its authors is based on careful research. Nevertheless, no liability is assumed for financial losses or a content-related guarantee for the topicality, correctness, appropriateness and completeness of the content provided here. Please also note our Terms of use.