March 6th, 2026 | 08:10 CET

Rockets are blasting into March! Investors are eyeing E.ON, Standard Uranium, and Plug Power

The current military actions in Iran did not come as a complete surprise. However, very few observers had anticipated an escalation across the entire Middle East. Oil and gas are therefore once again testing a breakout, even though global markets should theoretically face a surplus due to the weak economic environment. Regardless, speculators are simply trading fossil fuels higher; let's see if they stay up there. The global expansion of nuclear power programs is being reinforced by such periods of uncertainty. One example is India, which plans to expand its nuclear power capacity to around 100 GW by 2047, while currently less than 10 GW is installed. Such expansion plans reflect the growing demand for reliable base load energy in an increasingly digitalized economy and act as a hedge against commodity-induced crises. The long-term demand outlook for uranium is improving almost daily as a result of such trends, drawing investors' attention to companies with promising projects. Here are a few ideas.

time to read: 6 minutes

|

Author:

André Will-Laudien

ISIN:

E.ON SE NA O.N. | DE000ENAG999 , STANDARD URANIUM LTD | CA85422Q8487 | TSXV: STND , OTCQB: STTDF , PLUG POWER INC. DL-_01 | US72919P2020

Table of contents:

Author

André Will-Laudien

Born in Munich, he first studied economics and graduated in business administration at the Ludwig-Maximilians-University in 1995. As he was involved with the stock market at a very early stage, he now has more than 30 years of experience in the capital markets.

Tag cloud

Shares cloud

Standard Uranium – North America's supply chain on the agenda

The global energy transition, accelerated by the rapidly growing electricity demand of AI data centers, industrial expansion, and population growth, is bringing nuclear energy back into the spotlight of long-term energy planning. Various industry analyses predict that global nuclear capacity will expand significantly by 2050, leading to a structural increase in demand for uranium. At the same time, market observers expect demand to rise by around a third by the end of this decade, as numerous countries are using nuclear power as a stable and low-carbon base load to achieve their climate targets. This growth in demand is meeting with a structurally sluggish supply, as new uranium mines often require many years of development. As a result, the price of uranium has recovered significantly in recent years and is currently at levels that make new projects appear more economically attractive.

This is precisely where Canadian explorer Standard Uranium Ltd. comes in. The company's projects are located in Canada's renowned Athabasca Basin, one of the world's most important uranium regions. Its strategy is based on a project generator model. Exploration programs are developed jointly with partners who cover a large portion of the drilling costs. This allows the company to advance several projects in parallel and limit its own capital requirements. At the same time, it generates revenue from management fees and participation options in the projects. In total, Standard Uranium controls approximately 241,000 acres of mineral rights, with a central focus on the Davidson River Uranium project, the company's flagship project. The area in the southwest is located in a region where over 400 million pounds of high-grade uranium have already been discovered. Geological surveys have identified more than 70 km of promising structural trends that could harbor potential deposits. To define targets, the company uses data-driven analysis and machine learning to compare geophysical patterns of known deposits with new target zones.

Additional exploration programs are running in parallel with partners. A winter drilling campaign with up to 3,000 m of drilling commenced at the Corvo Uranium Project in early 2026. The target is near-surface uranium structures along conductive trends. Of particular interest is the Manhattan deposit, where uranium values of up to 8.10% U₃O₈ were found at surface. Aventis Energy Inc. is providing the financing, while Standard Uranium is acting as the operator. A drilling program is also planned for the first time at the Rocas Uranium project. Several drill holes will test a 7.5-kilometer-long structural corridor where radioactive anomalies have previously been identified. The first exploration phase is being financed by Collective Metals Inc., which can acquire a majority stake under an earn-in agreement. The portfolio also includes other properties such as the Sun Dog Uranium Project in the Uranium City district. Surface samples have already yielded uranium values of up to 3.58% U₃O₈, while many structures have hardly been tested by drilling to date. Overall, Standard Uranium combines a broad project portfolio with technology-based exploration and a partnership-based financing model. This creates several potential price drivers for investors, which will impact the valuation when relevant news is released. For now, the market capitalization is still slumbering at CAD 15.5 million - in this progressive market environment, that likely won't last for long!

Plug Power – Hope dies last

The US market leader in the electrolyser business is going through a long period of adjustment. After a bull market that saw the share price rise to USD 60 in 2021, it fell dramatically by 98.5% to USD 0.75 by 2025. In the USD 0.75 to 2.50 range, there were capital increases in the billions, which loyal followers were still willing to contribute. It is still uncertain whether CEO Andy Marsh will finally be able to deliver. The company has now abandoned its official guidance, as order intake has been too erratic and volatile recently. There is still a lack of public contracts, which arrived sporadically during Joe Biden's administration but are now subject to Trump's "Drill Baby Drill" motto. The new US president is a fan of fossil fuels and plans to promote nuclear power, with statements on hydrogen rarely heard. For the years 2026 to 2028, analysts on the LSEG platform expect revenues to rise from USD 710 million in 2025 to USD 1.2 billion. Compared to previous price-to-sales ratios of over 15, this ratio has now fallen to 3. A positive EBIT is nevertheless forecast for 2030. So all we need is a little "patience"!

E.ON – Robust results, but analysts remain skeptical

European energy supplier E.ON SE is one of the most important infrastructure players in the energy transition. With growing demand for electricity due to electrification, renewable energy, and AI data centers, the importance of modern power grids is increasing significantly. As one of the largest distribution network operators in Europe, E.ON is benefiting directly from this structural trend. Strategically, the group focuses primarily on regulated network infrastructure and customer-oriented energy solutions, thereby deliberately positioning itself more strongly as an infrastructure operator. The figures for the 2025 financial year show solid operational development, with adjusted EBITDA rising to EUR 9.8 billion, at the upper end of the company's own forecast. This resulted in a consolidated net income of around EUR 3 billion. The most important earnings driver was once again the network business, which saw double-digit growth in operating income. At the same time, E.ON invested around EUR 8.5 billion in the expansion and modernization of its network infrastructure. The Group intends to significantly expand its investments in the coming years. A total of around EUR 48 billion is planned for the period from 2026 to 2030 – that is a huge amount!

The management's stated goal is to make the power grids fit for the growing share of renewable energy and for new electricity consumers such as data centers and electromobility. A growing portion of the financing is provided by green bonds, which underscores the strategic focus on sustainable infrastructure. Analyst ratings vary. Goldman Sachs remains optimistic and confirms a "Buy" recommendation with a target price of EUR 19, citing stable growth prospects in the grid business. Bernstein Research rates the stock as "Neutral" and, with a target price of EUR 17, sees no major short-term price drivers. DZ Bank is more skeptical, arguing that many positive expectations may already be reflected in the share price and sees EUR 17.50 over the next 12 months. Overall, the votes are not outstanding, with LSEG standing at an unspectacular EUR 18.52 in the consensus. For fans of the stock, there is at least a 3% dividend payout in mid-April.

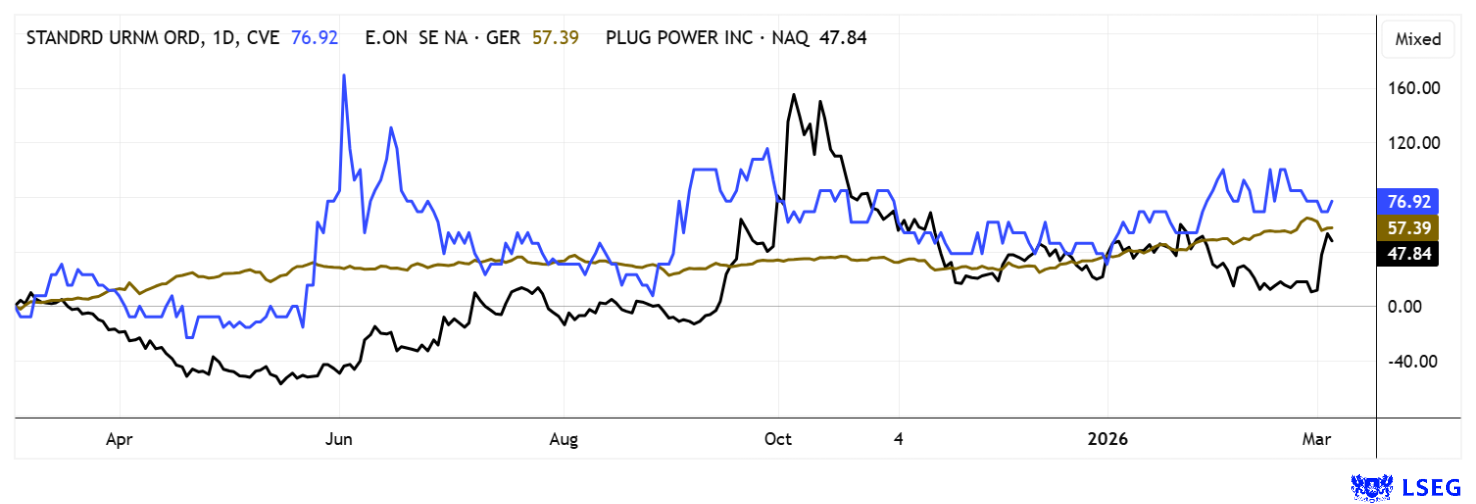

The stock markets currently have a lot to process. On the one hand, there is the absolute shortage of raw materials, which has had negative effects since China shifted its export strategy toward the West. At the same time, energy stocks are receiving increased attention. They must absorb the enormous energy demand generated by the surge in AI usage. No easy task! Investors are mixing blue-chip stocks such as E.ON with higher-risk plays like Standard Uranium or Plug Power - at least over the past 12 months, this has produced something of a "cocktail royale."

Conflict of interest

Pursuant to §85 of the German Securities Trading Act (WpHG), we point out that Apaton Finance GmbH as well as partners, authors or employees of Apaton Finance GmbH (hereinafter referred to as "Relevant Persons") currently hold or hold shares or other financial instruments of the aforementioned companies and speculate on their price developments. In this respect, they intend to sell or acquire shares or other financial instruments of the companies (hereinafter each referred to as a "Transaction"). Transactions may thereby influence the respective price of the shares or other financial instruments of the Company.

In this respect, there is a concrete conflict of interest in the reporting on the companies.

In addition, Apaton Finance GmbH is active in the context of the preparation and publication of the reporting in paid contractual relationships.

For this reason, there is also a concrete conflict of interest.

The above information on existing conflicts of interest applies to all types and forms of publication used by Apaton Finance GmbH for publications on companies.

Risk notice

Apaton Finance GmbH offers editors, agencies and companies the opportunity to publish commentaries, interviews, summaries, news and the like on news.financial. These contents are exclusively for the information of the readers and do not represent any call to action or recommendations, neither explicitly nor implicitly they are to be understood as an assurance of possible price developments. The contents do not replace individual expert investment advice and do not constitute an offer to sell the discussed share(s) or other financial instruments, nor an invitation to buy or sell such.

The content is expressly not a financial analysis, but a journalistic or advertising text. Readers or users who make investment decisions or carry out transactions on the basis of the information provided here do so entirely at their own risk. No contractual relationship is established between Apaton Finance GmbH and its readers or the users of its offers, as our information only refers to the company and not to the investment decision of the reader or user.

The acquisition of financial instruments involves high risks, which can lead to the total loss of the invested capital. The information published by Apaton Finance GmbH and its authors is based on careful research. Nevertheless, no liability is assumed for financial losses or a content-related guarantee for the topicality, correctness, appropriateness and completeness of the content provided here. Please also note our Terms of use.