June 5th, 2026 | 08:00 CEST

AI and Quantum Wonders Keep Happening: TeamViewer, SAP, and Aspermont Soaring, Palantir Sidelined

Quantum technology is considered one of the most significant waves of innovation of the 21st century and could completely turn entire industries upside down. At the same time, this same technological progress poses significant risks to digital security, as powerful quantum computers could one day overcome established encryption methods. Software and hardware companies are equally challenged. But while the tech titans from Silicon Valley are securing the physical and digital foundation of the AI economy, the valuation fantasies of individual high-flyers like Palantir are coming under increasing pressure from reality following a sharp correction. At least established software companies like SAP and TeamViewer are stabilizing in their new roles as AI integration and automation providers for businesses. Away from the mainstream, Aspermont is taking a radically different approach: there, data is not merely processed but transformed into an actual commodity within a raw materials-driven market environment. In the future, whoever controls access to relevant information will no longer decide merely on competitive advantages—but on market positions themselves.

time to read: 5 minutes

|

Author:

André Will-Laudien

ISIN:

ASPERMONT LTD. | AU000000ASP3 | ASX: ASP , SAP SE O.N. | DE0007164600 , TEAMVIEWER AG INH O.N. | DE000A2YN900 , PALANTIR TECHNOLOGIES INC | US69608A1088

Table of contents:

Author

André Will-Laudien

Born in Munich, he first studied economics and graduated in business administration at the Ludwig-Maximilians-University in 1995. As he was involved with the stock market at a very early stage, he now has more than 30 years of experience in the capital markets.

Tag cloud

Shares cloud

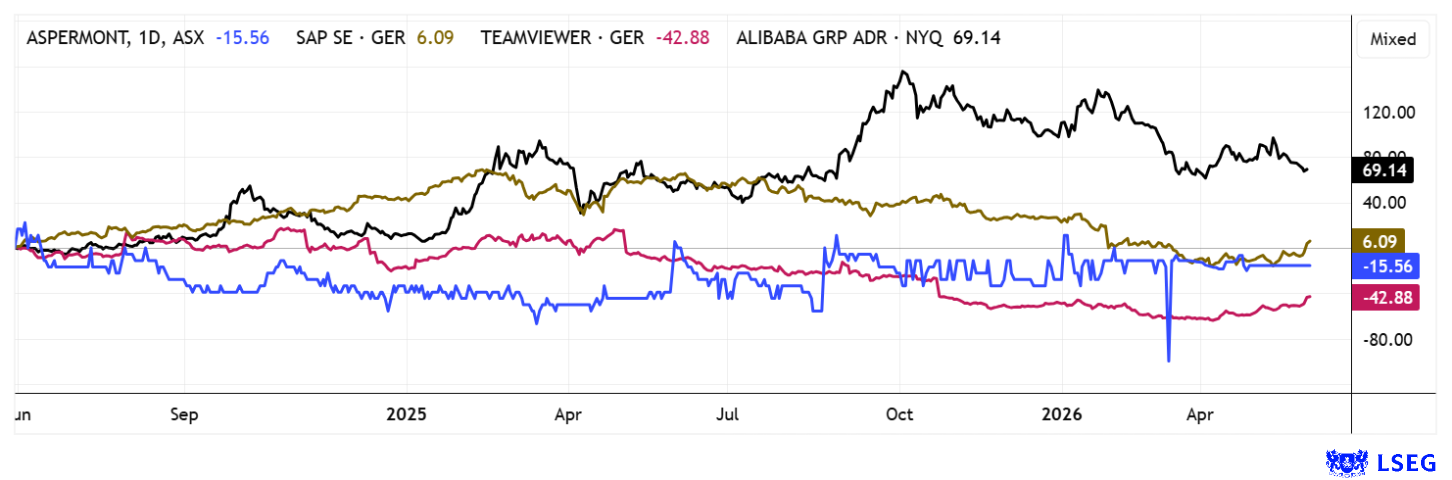

SAP and TeamViewer: Sentiment is Improving

The current realignment in the software and ERP segment is significantly shaped by two overlapping technological drivers: on the one hand, the deep integration of artificial intelligence into business processes, and on the other, the first signs of quantum-based computing architectures. The DAX-listed company SAP is at the center of this structural shift, as the group is increasingly evolving its long-established ERP foundation into an AI-powered process platform. By directly embedding AI functionalities into core business processes, the aim is to realize efficiency gains and optimize decision-making processes in real time. Large-scale cloud transformations support the business model's platform logic and create the necessary transparency and predictability for future revenue streams. Following a pronounced correction phase in May, during which the stock fell back to the EUR 135 range, a significant technical rebound recently set in, pushing the price up to around EUR 173, while the analyst consensus on LSEG Refinitiv implies price targets near EUR 218 over a 12-month horizon—an upside potential of around 40% from current levels.

TeamViewer is also in an upward operational trend. The stock hit its sell-off low of EUR 4.11 in April and rebounded dynamically by nearly 70% to EUR 6.70 by the end of May. Fundamentally, TeamViewer remains a company in transition. The enterprise business continues to grow strongly, while small and medium-sized customers have shown little momentum recently. There is still a lot of work to be done on the 1E acquisition. On the LSEG platform, however, experts are in good spirits, as 11 of 20 reports are optimistic, with an average 12-month price target of EUR 10.87. There is still plenty of potential there. Q2 figures are expected in mid-July. Well then!**

Aspermont: Data Engine for the Global Mining Industry

Anyone talking today about artificial intelligence, critical raw materials, and the industry's supply of copper, lithium, or rare earths cannot ignore one central resource: data.

This is where the Australian big data company Aspermont excels. Starting as a long-established trade publisher with roots dating back to 1835, it has gradually evolved into a specialized provider of digital information, data products, and intelligence solutions for the international commodities and mining industry. The strategic transformation was not spectacular, but rather consistent and characterized by strict capital discipline. Today, the business model is based on recurring revenue, proprietary data sets, and a network of industry contacts that has grown over decades. About two-thirds of revenue now comes from subscription-based business models, which ensures a high degree of revenue predictability. With more than 4,000 corporate clients, a 100% customer retention rate, and annual recurring revenue exceeding AUD 11 million, Aspermont has a stable foundation on which to build the next phase of growth.

The new AI platform, Mining IQ, is increasingly becoming the strategic heart of the company. This is because the combination of historical datasets, digitized archives, and AI-powered analytical tools is expected to create significant added value for mining companies, investors, and commodities experts in the future. At the same time, events, marketing services, and data-driven business solutions open up additional revenue streams across the entire value chain of the commodities sector. What makes this unique is that the business model offers significant economies of scale. The latest half-year figures demonstrate exactly what this entails. Revenue rose by 11.3% to AUD 7.48 million, up from AUD 6.72 million in the same period last year. Business outside of traditional subscriptions performed particularly well, while recurring revenue remained stable. Reported net profit reached AUD 0.60 million, following a loss of AUD 1.28 million in the prior year. While this result was positively influenced by valuation gains on the investment in Taiko Critical Minerals, the operating metrics also show a significant improvement. For instance, the normalized EBITDA deficit narrowed to just around AUD 0.20 million in the second quarter, following a deficit of approximately AUD 0.80 million in the first quarter.

Analysts at the research firm GBC continue to view the investment case as valid. For the current fiscal year, they expect revenue of AUD 16.9 million and EBITDA of AUD 0.15 million. By 2028, revenue is projected to rise to AUD 21.3 million, while EBITDA could increase to approximately AUD 2.93 million. Following a transition phase with adjusted results that are still slightly negative, analysts anticipate a return to sustainable profitability as early as 2027. The current valuation level appears particularly noteworthy in this context. Despite the prospect of significantly rising cash flows, the stock's market valuation remains below that of many comparable data and software companies. Accordingly, GBC reaffirmed its "Buy" recommendation and raised its price target to AUD 5.45, or EUR 3.30, per share. The stock is currently trading at around EUR 1.25. Extremely exciting!

IIF host Lyndsay Malchuk interviewed the company's founder and CEO, Alex Kent, about the future outlook.

Palantir: Is a New Rally on the Horizon, Or Is That It?

Stocks are not always undervalued. For the "US data giant" Palantir, valuation remains a central, ongoing topic of discussion among market participants despite all its operational successes. With an expected 2026 P/E ratio of just under 100 and an enterprise value of around 45 times annual revenue, the Denver-based company remains one of the most expensive software companies in the world. While the recent correction in the tech sector has somewhat normalized this valuation, it is by no means a bargain. Added to this are risks posed by increasing competition from AI specialists such as OpenAI, Anthropic, and Meta, as well as potential delays in government budgets and procurement processes.

Nevertheless, there is much to suggest that Palantir continues to occupy a unique position within the AI sector. Few companies manage to successfully combine 85% revenue growth and 60% operating margins with high customer loyalty. This is likely due to the company's exceptionally prominent position in the public and government-related client sector. The current 40% price correction since the November highs was well anticipated by short-seller Michael Burry and undermines CEO Alex Karp's attempts to reassure investors. While the company is fundamentally strong, a sustained overvaluation is rather unlikely. Palantir will release its Q2 results on August 10. Exciting!

International stock markets are in a celebratory mood. This is particularly true for technology and software stocks in the AI and quantum computing sectors. The scenario could change, as SpaceX is set to go public in a few days - an USD 80 billion IPO and a new MAG7 stock. Experts say a rotation of capital will begin. It will be interesting to see where the shifts will land. Our selected stocks—SAP, TeamViewer, and Aspermont—are currently trading near the lower end of their valuation ranges, presenting good medium-term opportunities.

Conflict of interest

Pursuant to §85 of the German Securities Trading Act (WpHG), we point out that Apaton Finance GmbH as well as partners, authors or employees of Apaton Finance GmbH (hereinafter referred to as "Relevant Persons") currently hold or hold shares or other financial instruments of the aforementioned companies and speculate on their price developments. In this respect, they intend to sell or acquire shares or other financial instruments of the companies (hereinafter each referred to as a "Transaction"). Transactions may thereby influence the respective price of the shares or other financial instruments of the Company.

In this respect, there is a concrete conflict of interest in the reporting on the companies.

In addition, Apaton Finance GmbH is active in the context of the preparation and publication of the reporting in paid contractual relationships.

For this reason, there is also a concrete conflict of interest.

The above information on existing conflicts of interest applies to all types and forms of publication used by Apaton Finance GmbH for publications on companies.

Risk notice

Apaton Finance GmbH offers editors, agencies and companies the opportunity to publish commentaries, interviews, summaries, news and the like on news.financial. These contents are exclusively for the information of the readers and do not represent any call to action or recommendations, neither explicitly nor implicitly they are to be understood as an assurance of possible price developments. The contents do not replace individual expert investment advice and do not constitute an offer to sell the discussed share(s) or other financial instruments, nor an invitation to buy or sell such.

The content is expressly not a financial analysis, but a journalistic or advertising text. Readers or users who make investment decisions or carry out transactions on the basis of the information provided here do so entirely at their own risk. No contractual relationship is established between Apaton Finance GmbH and its readers or the users of its offers, as our information only refers to the company and not to the investment decision of the reader or user.

The acquisition of financial instruments involves high risks, which can lead to the total loss of the invested capital. The information published by Apaton Finance GmbH and its authors is based on careful research. Nevertheless, no liability is assumed for financial losses or a content-related guarantee for the topicality, correctness, appropriateness and completeness of the content provided here. Please also note our Terms of use.