April 23rd, 2026 | 07:15 CEST

Middle East Escalates Shortages: Supply Chains at Risk - Nordex, Antimony Resources, and Siemens Energy

Prepared and published on behalf of Antimony Resources Corp.

The ongoing conflict in the Middle East once again highlights how vulnerable global supply chains for critical metals are when a strategic chokepoint like the Strait of Hormuz comes under pressure. What matters here is not so much the direct transport of metals through the strait, but rather its importance to global energy trade; a disruption there would rapidly drive up the costs of energy-intensive metals such as aluminum, copper, or nickel. Higher freight rates, more expensive insurance, and longer routes would further increase logistics costs and significantly slow down just-in-time structures in many industries. Raw materials that are indispensable for the energy transition, digitalization, and defense would be particularly affected. A recent study concludes that a prolonged blockade of the Strait of Hormuz could disrupt global trade flows worth up to USD 1.2 trillion annually. Which stocks are now in the spotlight?

time to read: 5 minutes

|

Author:

André Will-Laudien

ISIN:

ANTIMONY RESOURCES CORP | CA0369271014 | CSE: ATMY , OTCQB: ATMYF , NORDEX SE O.N. | DE000A0D6554 , SIEMENS ENERGY AG NA O.N. | DE000ENER6Y0

Table of contents:

Author

André Will-Laudien

Born in Munich, he first studied economics and graduated in business administration at the Ludwig-Maximilians-University in 1995. As he was involved with the stock market at a very early stage, he now has more than 30 years of experience in the capital markets.

Tag cloud

Shares cloud

Antimony Resources: Iran Crisis Boosts Antimony Demand - Bald Hill Can Deliver

The EU is finally waking up! The Iran conflict underscores the precarious situation of Western industries without stable energy and metal sources. The antimony market used to cater to a niche demand, but with global rearmament, it is now taking center stage—a disaster for industry, a source of medium-term returns for investors. The world is experiencing a classic supply crisis, as China, with a 70% share of production, dictates prices, driving them from USD 15,000 to over USD 60,000 per ton at times. Demand is exploding due to applications in flame retardants, batteries, solar cells, and military technology, while governments currently have no idea how to replenish their reserves.

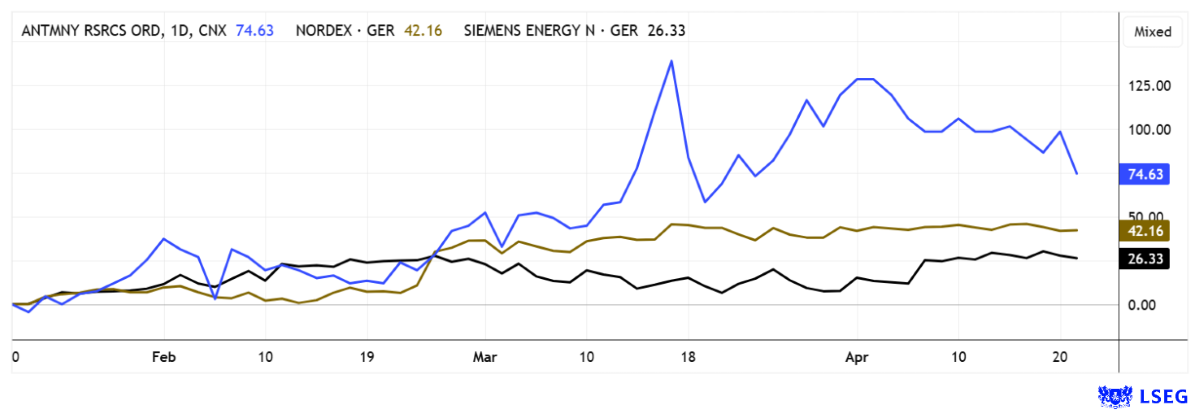

Antimony Resources' stock surged 500% in five months, from CAD 0.33 to CAD 1.65, reflecting the strategic revaluation of the sector. The Bald Hill project in New Brunswick, which is currently the focus of attention, stands out in North America with 2.7 million tons of ore at a 3-4% grade, as it has the potential to produce 94,500 tons of antimony. Recent drilling confirmed mineralization over a 700-meter strike length and 350-meter depth, with peaks exceeding 30%. Antimony Resources has now initiated environmental studies with GEMTEC and is engaging with New Brunswick authorities and First Nations. A clear approval plan, including baseline studies and an EIA roadmap, minimizes risks early on. The timeline is tight, as the company aims to make progress.

Important for investors: The first NI 43-101 resource estimate is approaching; for many junior miners, this is the moment for a valuation jump. With a market capitalization of CAD 115 million, there remains massive upside relative to the metal value from today's perspective. Of course, mine development must still follow its usual course, but an acquisition by a major player is not unlikely. Research firm GBC sees a 12-month price target of CAD 3.00 per share, which means the rally is gaining further momentum. The current correction makes it easy to get in!

CEO James R. Atkinson outlines key parts of his strategy in an interview with IIF host Lyndsay Malchuk.

Nordex: Can the quarterly figures deliver a margin jump?

A classic consumer of critical metals is wind turbine specialist Nordex. After a long dry spell, the Hamburg-based company finally got its operating business back on track in 2025; in fact, it even slightly exceeded its EBITDA margin target of over 8% last year. Given the overall strong performance and good visibility driven by the order backlog and service portfolio, the company is now raising its medium-term EBITDA margin target to 10.0–12.0%.

Investors are hoping that management has calculated this correctly. After all, the stock price has already anticipated this development with a 12-month gain of 185%, hence the current peak in the EUR 44 to EUR 47 range. The company will publish its Q1 figures on April 27. Earnings per share are expected to be approximately EUR 0.183, with full-year earnings projected at EUR 1.80, up from EUR 1.16 in the previous year—a 55% increase. The upcoming press conference promises to be highly anticipated, as at these price levels, management must provide clear indications that the targets will be met; otherwise, a sharp drop in the share price looms. Given strained supply chains and global uncertainty, there is a high probability that CEO José Diéguez will strike a somewhat more cautious tone. 9 out of 18 experts on the LSEG platform remain positive, but the consensus price target has already dropped to EUR 42.80. Therefore, exercise caution!

Siemens Energy: Can the Munich-based company maintain its robust growth?

With a market capitalization of EUR 144 billion, the energy spin-off from Siemens AG is now a fixture in the DAX 40 index. One of the reasons for the outstanding performance of the former subsidiary Siemens Energy is the perfect positioning of its product portfolio and strategic focus on power generation and grids. In the global race for thousands of gigawatts to secure the AI and cloud capabilities of tech giants, a massive demand for power capacity has built up, which now needs to be gradually expanded. The left-green debates about sustainability and energy conservation from the COVID era have completely faded from political discourse, as the planet Earth is now set to steadily increase its energy demand for years to come. Political currents can shift 180 degrees that quickly.

Siemens Energy plays a key role in the AI economy because the massive expansion of data centers is driving demand for energy infrastructure. As a result, the Munich-based company is evolving from a traditional plant manufacturer into a central infrastructure player of the AI era, because sustainable growth in artificial intelligence is impossible without scalable power generation and grid stability. This also explains the company's immense valuation, which resembles that of a NASDAQ company more than a DAX stock. For analysts, revenue multiples of 5 and P/E ratios above 40 are uncharted territory. Consequently, the consensus price target of currently EUR 166 is mostly below the current trading price. It will be interesting to see when the experts finally change their minds and dramatically raise their price targets. By then, the Munich-based company's cyclical growth may have reached a point where the high multiples no longer make sense. With a double top in the range of EUR 168 to 174, investors should already be on high alert today. The next quarterly results are due on May 12. Exciting!

Investors have faced challenging times. Global markets remain marked by significant volatility, as the decisions and statements of US President Donald Trump continue to exert a major influence on global events. Like many other raw materials, antimony is also considered a key metal for the high-tech and defense industries. If the Strait of Hormuz is not restored to unrestricted passage in the near future, serious production disruptions could arise in parts of the Western economy. In such an environment, Antimony Resources is likely to attract increased investor interest, as the company is viewed as a future building block for stabilizing Western supply chains. For Nordex and Siemens Energy, the next quarterly results will have to show whether the strong price gains are justified in the medium term.

Conflict of interest

Pursuant to §85 of the German Securities Trading Act (WpHG), we point out that Apaton Finance GmbH as well as partners, authors or employees of Apaton Finance GmbH (hereinafter referred to as "Relevant Persons") currently hold or hold shares or other financial instruments of the aforementioned companies and speculate on their price developments. In this respect, they intend to sell or acquire shares or other financial instruments of the companies (hereinafter each referred to as a "Transaction"). Transactions may thereby influence the respective price of the shares or other financial instruments of the Company.

In this respect, there is a concrete conflict of interest in the reporting on the companies.

In addition, Apaton Finance GmbH is active in the context of the preparation and publication of the reporting in paid contractual relationships.

For this reason, there is also a concrete conflict of interest.

The above information on existing conflicts of interest applies to all types and forms of publication used by Apaton Finance GmbH for publications on companies.

Risk notice

Apaton Finance GmbH offers editors, agencies and companies the opportunity to publish commentaries, interviews, summaries, news and the like on news.financial. These contents are exclusively for the information of the readers and do not represent any call to action or recommendations, neither explicitly nor implicitly they are to be understood as an assurance of possible price developments. The contents do not replace individual expert investment advice and do not constitute an offer to sell the discussed share(s) or other financial instruments, nor an invitation to buy or sell such.

The content is expressly not a financial analysis, but a journalistic or advertising text. Readers or users who make investment decisions or carry out transactions on the basis of the information provided here do so entirely at their own risk. No contractual relationship is established between Apaton Finance GmbH and its readers or the users of its offers, as our information only refers to the company and not to the investment decision of the reader or user.

The acquisition of financial instruments involves high risks, which can lead to the total loss of the invested capital. The information published by Apaton Finance GmbH and its authors is based on careful research. Nevertheless, no liability is assumed for financial losses or a content-related guarantee for the topicality, correctness, appropriateness and completeness of the content provided here. Please also note our Terms of use.